Analysis of turnover is one of the leading areas of analytical study of the financial activities of the organization. Based on the results of the analysis, estimates of business activity and the effectiveness of asset and / or capital management are made.

Today, the analysis of working capital turnover raises many disputes between practical economists and theoretical economists. This is the most vulnerable point in the whole methodology of financial analysis of the organization.

What characterizes the analysis of turnover

The main purpose with which it is conducted is to assess whether the enterprise is able to make a profit by completing the “money-commodity-money” turnover. After the necessary calculations, the conditions of material supply, settlements with suppliers and customers, sales of manufactured products, etc. become clear.

So what is turnover?

This is an economic value that characterizes a specific time period for which the full circulation of cash and goods, or the number of these calls for the allotted time period.

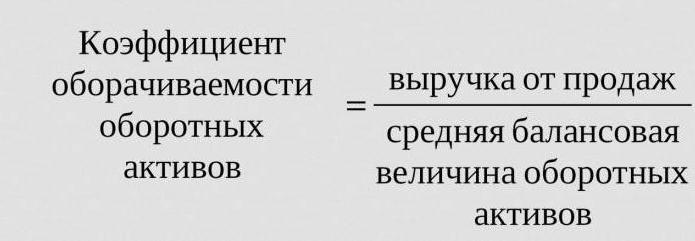

So, the turnover ratio, the formula of which is given below, is three (the analyzed period is year). This means that the company for the year of work helps out the second money more than the value of its assets (i.e., they turn around three times in a year).

The calculations are simple:

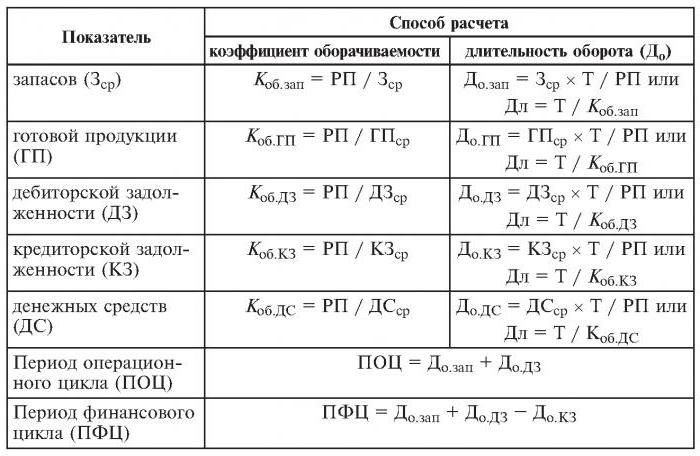

TOabout = sales revenue / average assets.

It is often required to find out the number of days for which one revolution takes place. For this, the number of days (365) is divided by the turnover ratio for the analyzed year.

Frequently Used Turnover Ratios

They are needed to analyze the business activity of the organization. The turnover indicators of funds show the intensity of use of liabilities or certain assets (the so-called turnover rate).

So, conducting the analysis of turnover, use the following turnover ratios:

- equity capital of the enterprise,

- assets of current assets,

- full assets

- stocks

- debts to creditors,

- accounts receivable.

The higher the estimated turnover ratio of full assets, the more intensively they work and the higher the indicator of business activity of the enterprise. Turnover is not always positively influenced by industry specifics. So, in trade organizations through which large amounts of money pass, the turnover will be high, while at capital-intensive enterprises it will be much lower.

When comparing the turnover ratios of two similar enterprises belonging to the same industry, one can see the difference, sometimes significant, in the efficiency of managing active assets.

If the analysis shows a large turnover ratio of receivables, then there is reason to talk about a significant collection efficiency.

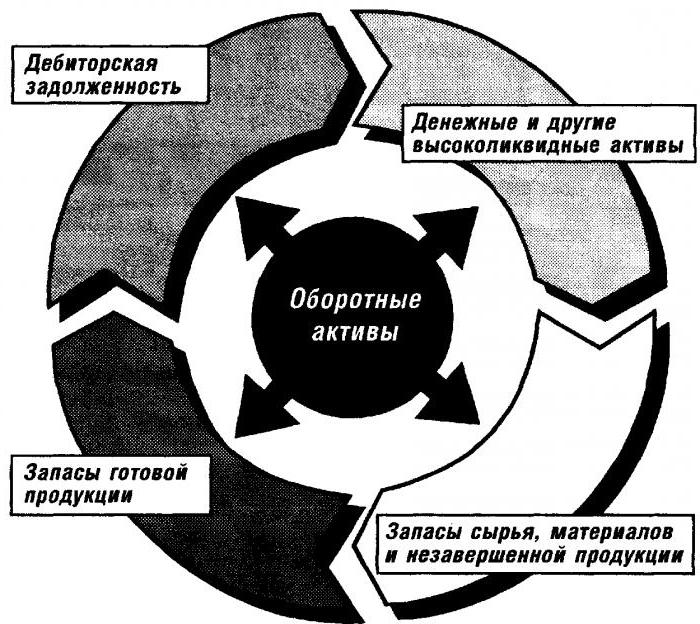

Analysis of working capital turnover

This coefficient gives a characteristic of the speed of movement of working capital from the moment of receipt of payment for tangible assets and ending with the return of money for sold goods (services) to bank accounts. The amount of working capital is the difference between the total amount of working capital and the cash balance in the bank on the accounts of the enterprise.

In the case of an increase in the speed of turnover with the same volume of goods (services) sold, the organization uses lower amounts of working capital. From this we can conclude that material and monetary resources will be used more efficiently. Thus, the turnover ratio of working capital indicates the totality of the processes of economic activity, such as: a decrease in capital intensity, an increase in productivity growth rates, etc.

Factors affecting the acceleration of working capital turnover

These include:

- reduction of the total time spent on the technological cycle,

- improvement of technology and production process,

- improving the supply and marketing of goods,

- transparent payment and settlement relations.

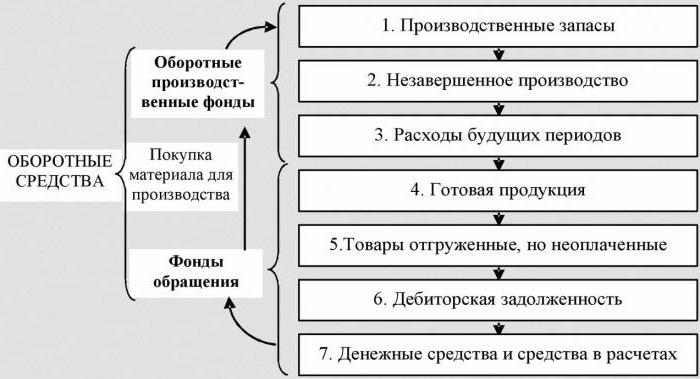

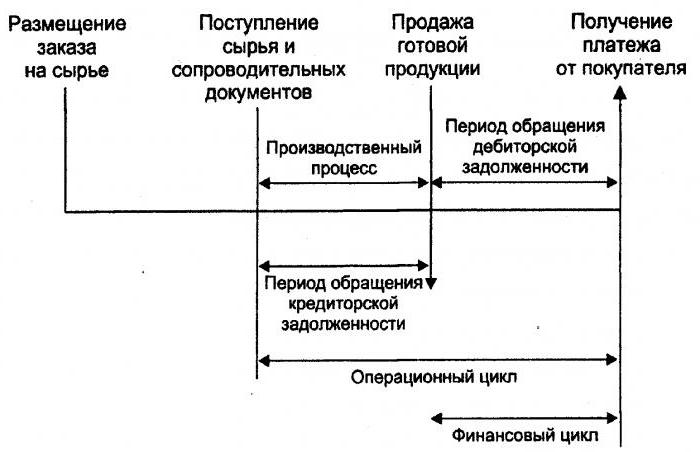

Money cycle

Or, as it is also called, working capital is a temporary period of cash turnover. Its beginning is the moment of the acquisition of labor, materials, raw materials, etc. Its end is the receipt of money for goods sold or services provided. The magnitude of this period shows how effective is the management of working capital.

A short money cycle (a positive characteristic of the organization) makes it possible to quickly return the funds invested in current assets. Many enterprises with a strong market position, after analyzing the turnover, receive a negative working capital ratio. This is due, for example, to the fact that such organizations have the ability to impose their terms on both suppliers (receiving various payment delays) and customers (significantly reducing the payment term for delivered goods (services)).

Inventory turnover

This is the process of replacing and / or completely (partially) updating stocks. It goes through the transition of material values (that is, capital invested in them) from a group of stocks into the production and / or sale process. Analysis of inventory turnover makes it clear how many times the balance has been used over the billing period.

Inexperienced managers for reinsurance create surplus stocks without thinking about the fact that this excess leads to a “freeze” of funds, over-expenditures and lower profits.

Economists advise avoiding such low-turnover stocks. Instead, by accelerating the turnover of goods (services), release resources.

The inventory turnover ratio is one of the important criteria for evaluating the activity of an enterprise

That is why its thorough analysis is recommended.

If the calculations show an excessively high ratio (compared to the average or the previous period), this may mean a significant shortage of stocks. If on the contrary, the stocks of goods are not in demand or very large.

It is possible to obtain a characterization of the mobility of funds invested in the creation of stocks only by calculating the stock turnover ratio. And the higher the business activity of the organization, the faster the money is returned in the form of revenue from the sale of goods (services) to the accounts of the enterprise.

There are no generally accepted norms for the turnover ratio of funds. They are analyzed within the framework of one industry, and the ideal option is in the dynamics of a single enterprise. Even the slightest decrease in this coefficient indicates an excessive accumulation of stocks, inefficiency of warehouse management or the accumulation of unusable or obsolete materials. On the other hand, a high figure does not always characterize the business activity of the enterprise. Sometimes this indicates a depletion of stocks, which can cause disruptions in the process.

It affects the inventory turnover and the activities of the organization’s marketing department, since a high return on sales entails a low turnover ratio.

Accounts receivable turnover

This ratio characterizes the rate of repayment of receivables, that is, shows how quickly the organization receives payment for goods sold (services).

It is calculated for a single period, most often for a year. And it shows how many times the organization received payments for products in the amount of the average debt balance. He also gives a description of the policy of sales on credit and the effectiveness of work with customers, that is, how efficiently receivables are collected.

The accounts receivable turnover ratio does not have standards and norms, since it depends on the industry and technological features of production. But in any case, the higher it is, the faster the receivables are paid. At the same time, the efficiency of the enterprise is not always accompanied by high turnover. For example, sales of products on credit give a high balance of receivables, while the rate of turnover is low.

Accounts payable turnover

This ratio shows the relationship between the amount of money that must be paid to creditors (suppliers) by the agreed date and the amount spent on the purchase or purchase of goods (services). The calculation of the turnover of accounts payable makes it clear how many times during the analyzed period its average value has been repaid.

Financial stability and solvency are reduced with a high share of accounts payable. While it also gives the opportunity for the entire time of its existence to use "free" money.

The calculation is simple

The benefit is calculated as follows: the difference between the amount of interest on the loan, equal to the amount of debt (that is, a hypothetically taken loan) while it is on the balance sheet of the organization, and the volume of accounts payable.

A positive factor in the activity of the enterprise is the excess of the receivable ratio over the payable turnover ratio. Lenders prefer a higher turnover ratio, however, the company is profitable to keep this ratio at a lower level. After all, unpaid amounts of accounts payable are a free source for financing the current activities of the organization.

Resource return, or asset turnover

It makes it possible to calculate the number of capital turns for a single period. This turnover ratio, the formula exists in two versions, gives a characteristic of the use of all assets of the organization, regardless of the source of their receipt. It is important that, only by determining the coefficient of resource return, you can see how many rubles of profit falls on each ruble invested in assets.

The asset turnover ratio is equal to the quotient of dividing revenue by asset value on average for the year. If it is necessary to calculate the turnover in days, then the number of days in a year must be divided by the asset turnover ratio.

Leading indicators for this category of turnover are the period and speed of turnover. The latter is the number of revolutions of the organization’s capital for a certain period of time. Under this interval, understand the average period for which the return on funds invested in the production of goods or services.

Asset turnover analysis is not based on any norms. But the fact that in capital-intensive industries the turnover ratio is much lower than, for example, in the service sector, is definitely understandable.

Low turnover may indicate a lack of efficiency in working with assets. Do not forget that the rates of return on sales also affect this category of turnover.So, high profitability entails a decrease in asset turnover. And vice versa.

Equity turnover

It is calculated to determine the rate of equity of the organization for a given period.

The capital turnover of the organization’s own funds is designed to characterize various aspects of the financial activity of the enterprise. For example, from an economic point of view, this coefficient characterizes the activity of the money turnover of invested capital, from a financial one - the speed of one turnover of invested funds, and from a commercial one - surplus or insufficient sales.

If this indicator shows a significant excess of the level of sales of goods (services) over invested funds, then as a result, credit resources will begin to grow, which, in turn, allows reaching the limit beyond which lenders' activity increases. In this case, the ratio of liabilities to equity increases and credit risk increases. And this entails the inability to pay these obligations.

The low turnover of equity capital indicates their insufficient investment in the production process.