The basic rate of fuel consumption is a value that expresses the need for fuel of various types of vehicles. It is calculated on a strictly set number of km. The calculation is made, taking into account the mileage and the basic rate of fuel consumption per 100 km.

About relevance

This indicator is needed by enterprises that have cars for official use. These are vehicles listed in the property of the organization, and used in the course of its activities.

Sets the basic fuel consumption rate of the Ministry of Transport of the Russian Federation. All of his prescriptions serve only as recommendations. Enterprises apply the basic fuel consumption rate when calculating their fuel and lubricants.

general information

In order for the machines belonging to the organization to function smoothly, it is necessary to properly provide them with fuel. This is done by the enterprise itself, reflecting each procedure in accounting and tax transactions. The basic rate of fuel consumption per 100 km allows you to calculate gasoline, to control the consumption of raw materials. The legislation also regulates the issues related to the debiting of this material from the accounts of the organization.

Indicators of the basic rate of fuel consumption are used to keep records, calculate the real cost of transportation, which is carried out by vehicles for a clearly defined period of time. They are also used when taxing organizations. The basic fuel consumption rate is used when calculating household expenses with employees driving company vehicles.

When filling out reports, the employee writes in the necessary line the amount of consumable material that fits into the norm fixed by law. When a consumable has been consumed in an amount greater than the basic rate of fuel consumption, this must be entered into a special report form by an accountant. For these purposes, a separate line with the name "non-operating expenses" is reserved.

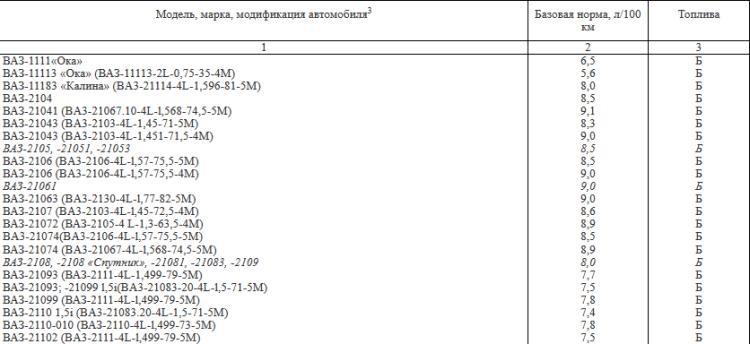

Be sure to keep in mind that the norm for different vehicles is different. So, the basic fuel consumption rate of Lada Vesta differs from other models of the same manufacturer. It is also affected by the period during which the machine has been operating, operating conditions, and so on.

At this moment

The basic linear fuel consumption rate was adjusted in 2015. In 2018, institutions that have their own fleets of vehicles can engage in the calculation of fuel and lubricants themselves or be guided by the basic rate of fuel consumption of vehicles recorded in the legislation of the Russian Federation.

In 2018, it was indicated that these standards are only recommendations, optional requirements. For this reason, organizations independently determine the basic rate of fuel consumption of cars for accounting, choose how to calculate it.

By brand

To calculate the costs, you need to know exactly the type of vehicle - whether a passenger car, truck, special purpose. After that, open the necessary lists and compare with the indicator of a particular brand of transport.

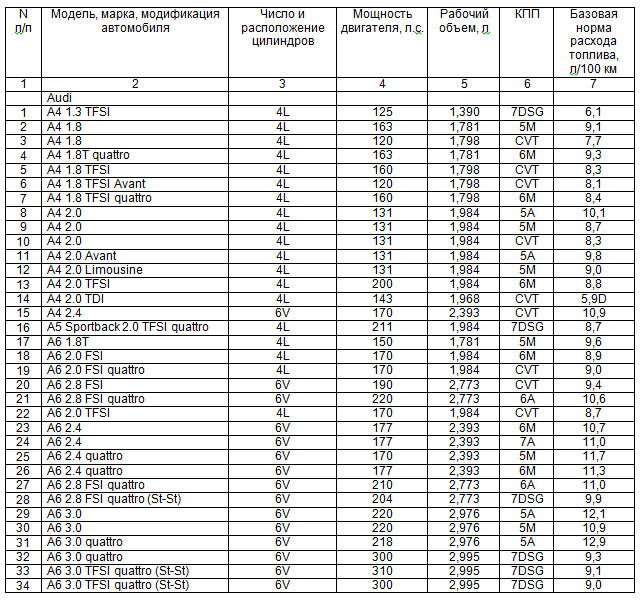

So, for the 2.5 Toyota Camry engine, the basic fuel consumption rate is 8.3 liters per 100 km. You need to know that a flow rate of up to 10 liters is considered a good indicator.

The basic fuel consumption rate of Lada Vesta is 8.1 liters per 100 km. When the figure reaches more than 10 liters per 100 km, the situation requires explanation.

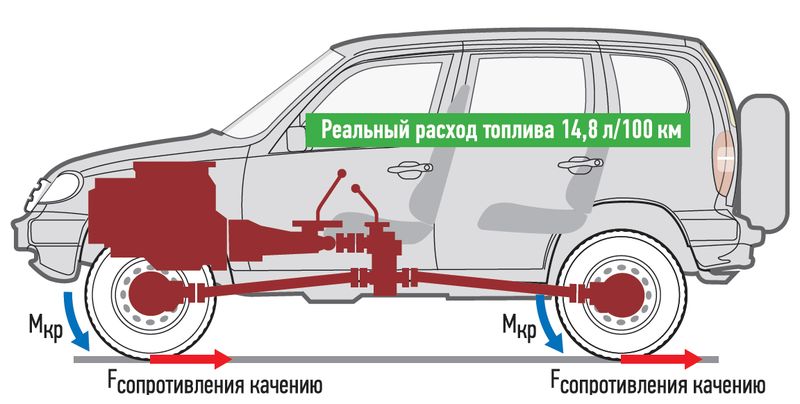

The basic fuel consumption rate of UAZ-Patriot is 9.5-14 liters per 100 km. In recent years, the best indicator, taking into account savings per 100 km, is a 6 liter consumption.

The basic fuel consumption rate of Lada-Largus is 7.9–8.2 liters per 100 km.

It happens that due to the peculiarities of vehicles or weather conditions, one more characteristic is used. They can introduce a correction factor to the base rate of fuel consumption.

Counting gasoline, take a number of the following indicators. In the cold season, a correction factor is applied to the base rate of fuel consumption. It varies significantly depending on the proximity of the territory to the northern territories. The increasing coefficient is used when using transport in urban settlements. The larger they are, the higher the coefficient.

How to count?

Gasoline consumption is calculated independently, however, when the authorities check it, the best decision is to indicate that the organization takes into account the recommendations of the Ministry of Transport, but reserves the right to independently calculate the indicator due to the nature of the use of vehicles.

In order to calculate the fuel used for a particular vehicle, it is important to divide the fuel volume by the number of kilometers covered, multiplying the number by 100. This method calculates the amount of fuel needed per 100 kilometers.

About decommissioning

Institutions involved in the delivery of goods write off fuel by waybills with the vehicle mileage recorded in them. To keep accounting, apply 10 account with sub-accounts. In order to supply gasoline for arrival, information is recorded in debit 10 of the account. At the time of writing off, this indicator is entered into the credit of the same account. The amount of fuel is calculated on the basis of the norm, which is indicated in the standards or was calculated by the legal entity itself, multiplied by the amount of consumable.

In tax accounting, fuel and lubricants are written off, attributing to material or other expenses. If a truck carries goods, fuel costs are classified as material costs.

With the introduction of tax accounting, fuels and lubricants are taken into account either on the fact or in accordance with official standards.

When an organization uses machines that were not listed in a regulatory act issued by the Ministry of Transport of the Russian Federation, it reserves the right to calculate the nominal indicator manually.

More about odds

Apply high standards in the cold season. In frost, transport needs more gasoline. For this reason, the rate for counting is increased by 5-20%. In each region of the Russian Federation, a separate percentage of premiums and its validity periods are applied. Data on this is contained in the norms established by law.

The same applies to mountainous areas: add 5-20% when transport moves through territories located above sea level. The higher it is, the higher the percentage premium will be.

The next case, when they use the increased coefficient, is the use of public transport. Apply a premium of 5-25%. They also work with special characteristics of the road surface in large settlements, increasing the norm by 5-25%. The final result is directly dependent on the number of inhabitants.

In addition, with an increase in the period of use of vehicles, the premium increases when calculating the rate of gasoline consumption. When the mileage of vehicles was more than 100,000 kilometers, and the car was used for more than 5 years, the consumption rate of gasoline rises by 5%.

Norm binding

The Tax Code of the Russian Federation does not require mandatory compliance with gasoline consumption standards when it comes to official vehicles. The organization can take into account the amount of fuel and lubricants spent by employees, according to letters from the Ministry of Finance of the Russian Federation. An exception are enterprises that are engaged in administrative activities and use special equipment on the chassis. The tax authorities believe that they have an obligation to write off expenses for fuel and lubricants according to the norms.In order to avoid the difficulties associated with justifying expenses, as well as to exclude the possibility that employees will abuse the situation, many enterprises prefer the recommendations of the ministry.

To take into account the costs, they apply the standards that they personally developed, the information of the car manufacturers or the gas consumption rate calculated by the Ministry of Transport of the Russian Federation.

About the risks

It must be remembered that the write-off of fuel costs carries certain risks. Fuel costs are not taken into account in tax accounting if the employee is paid compensation for work on personal vehicles.

Of course, the application of the standards already developed and established by the Ministry of Transport of the Russian Federation is much more convenient. They contain allowances that take into account the terrain, especially the time of year, the operation of transport. Through these factors, fuel costs can increase.

As of 2018

In 2018, the norms approved by the Ministry of Transport in 2015 are used.

The increasing coefficient, due to which the consumption rate increases, is allowed to be fixed taking into account the operating life of the machine and its mileage. For example, to start accounting for a factor of 5%, the vehicle’s mileage should be more than 100,000 kilometers or the life of the transport should be more than 5 years.

In addition, premiums were increased for the largest settlements, the coefficient for technological machines was increased, taking into account those that operate within the enterprise.

In 2018, the maximum allowance was 35%. This level is maintained for vehicles used in settlements with a population of more than 5 million people.

In urban settlements with a population of up to 5 million people, the rate of deduction of fuel and lubricants increases by 25%.

When it comes to technological vehicles, the maximum allowance is 20%. This fact applies to equipment moving not along roads, but through industrial zones, or for vehicles used in mining operations. These include excavators, industrial equipment, combines, pavers and so on.

Employers compensate employees for using private cars. The conditions and amount for reimbursement are determined in writing.

Mixed and basic flow rates

There are many differences between the two terms - mixed and basic consumption rates. Usually, after acquiring a new vehicle and getting acquainted with its transport characteristics, it becomes noticeable which cycle is preferable for him in work: urban, suburban or mixed.

You need to know that these terms belong to another area that has nothing to do with the methods of calculating basic norms. For this reason, it is important to determine whether fuel will be written off according to information from the technical characteristics or whether the consumption will be taken into account using the order of the Ministry of Transport dated 14.03.2008 No. AM-23-r.

After solving this issue, you need to understand that the calculation of the mixed norm for AM-23-p will not be possible. The thing is that there are no such concepts in it. If a mixed norm would be approved, then you need to be aware that in this way a person is removed from the very concept of the basic rate of fuel consumption.

General purpose vehicles

In relation to general purpose vehicles, the following types of rules apply. One of them is the basic rate in liters per 100 kilometers of the car. The second is the transport norm in liters per 100 kilometers of vehicles, relating to buses and dump trucks. The third type is the transport norm in liters per 100 ton-kilometers of trucks. It is she who is taken into account in addition to the basic rate of gasoline consumption when moving freight vehicles, trains with trailers for diesel cars and their gasoline varieties.

Or it is possible to use the calculation of increased accuracy performed by the Federal State Unitary Enterprise "Scientific Research Institute of Automobile Transport" according to programs for certain types of equipment.

The level of the basic rate of gasoline consumption will greatly depend on the device of the machine, its units, type and purpose of rolling stock, on the type of fuel that is used, it will take into account the state of the vehicle, the route and the nature of the movements during the trip.

The norm for the operation of the car includes basic norms, it depends on the carrying capacity of the machine, on the normalized loads, on the mass of the transported products. Take into account the features of the use of vehicles.

The fuel consumption rate per 100 kilometers of vehicles is recorded in specific measurement forms. For cars on gasoline or diesel - in liters of gasoline or diesel fuel. For vehicles operating on petroleum gas - in liters of liquefied petroleum gas. For machines operating on compressed natural gas - in cubic meters of liquefied natural gas.

For gas-diesel vehicles, the rate of consumption of compressed natural gas is fixed in cubic meters. In addition, the rate of diesel fuel consumption in liters is fixed. The proportions are calculated by the equipment manufacturers themselves.

Take into account road transport, climatic and other operational factors. At the same time, correction factors must be used, which are indicated in the format of percent increase or decrease in the initial norm values. They are recorded by the leadership of organizations that use automobile vehicles. They can also be recorded by local administration.

Additional Information

It must be remembered that the level of the basic rate of fuel consumption for vehicle mileage decreases if the road lies outside the suburbs, on flat and hilly areas at an altitude of 300 meters above sea level on roads of categories 1, 2 and 3 - up to 15 %

When a car is used in suburban areas outside the city limits, the use of correction factors is not applicable.

If necessary, they can use a number of premiums to the rate of fuel consumption at once.

The situation is regulated somewhat differently when it comes to the consumption of fuel for gas balloon transport in such situations.

Firstly, when it comes to entering or leaving repair areas after technical intervention has been carried out, the consumption rate increases by 5 liters per unit of gas-filled motor vehicles.

Secondly, with regard to the launch of gas cylinder engines, up to 20 liters of gasoline per month for 1 car are additionally taken into account. In addition, in the summer, spring, autumn time period, the winter allowance is taken into account.

Thirdly, an increase in the norm to 25% of the total fuel consumption occurs when it comes to driving on roads whose length is greater than the range of one full gas refueling. In these cases, the liquid fuel consumption of vehicles is standardized equally for gas and gas vehicles.

Taking into account the many changes in the technogenic and natural character, the diversity in the conditions of the use of vehicles, the condition of the road surface, the nuances of cargo transportation and passengers, if necessary, individual correction factors are introduced or specified to the fuel consumption rate by decision of the regional leadership.

For the latest models of vehicles, for which the Ministry of Transport of the Russian Federation has not yet approved the basic norms of gasoline consumption, the regional leadership has the right to issue orders to put into effect the provisional norms from FSUE NIIAT, which were in force before the norms were approved by the Ministry of Transport of the Russian Federation.

About lubricant consumption

The rate of lubricant in vehicles is taken into account, based on the calculation of the specific consumption rate of oils, lubricants, their need should be justified documented.

The operating consumption rate of lubricants, taking into account the replacement and current refueling, is set based on 100 liters of the total gasoline consumption, which was calculated in accordance with the recommendations for this type of vehicle. It is fixed in liters per 100 liters of gasoline.

The oil consumption rate rises to 20% for machines that have gone through major repairs and have been used for more than 5 years.

The consumption of lubricant during the overhaul of parts of vehicles is fixed in the amount corresponding to one complete filling of the lubrication system of this mechanism. The consumption of brake, cooling and other type of fluid is calculated in the amount of refueling and refueling for 1 car, taking into account the recommendations of manufacturers, instructions that are always attached to the vehicle.

Conclusion

Thus, for accounting, the basic rate of fuel consumption of cars is the most important indicator relating to vehicles, which requires reflection in accounting. It will be calculated individually for each brand of car. It is important to remember that competent calculation opens up many opportunities for reducing the tax base. This information is relevant for any enterprise that uses automotive equipment in its activities.