Interest-free loans are considered to be quite demanded ways to get the right amount. Agreements are drawn up not only between citizens, but also between different companies. The procedure for providing funds depends on the status of participants. If it is implemented between two organizations, it is important to pay a lot of attention to competent registration in accounting. An interest-free loan between legal entities is issued taking into account many features.

Basic concepts

Lending is considered an important area of activity in which not only banks, but also other organizations work. Often, different companies need a free amount of money, but at the same time drawing up a standard loan is considered an inexpedient decision. Therefore, an interest-free loan agreement between legal entities is used. When applying it, it is not required to pay interest and commission for the use of money.

Even when using such a loan, a certain participant has a material benefit. Therefore, it is important to correctly reflect the implementation of this transaction in the financial statements. A company that makes a profit must pay taxes, otherwise it will have problems with the tax authorities.

Loan concept

An interest-free loan between legal entities is represented by the process of providing one organization of the second company a certain amount of funds at no cost. No interest or commission is paid for this money.

When using such a loan, the borrower has a material gain represented by the percentage savings.

When using an interest-free loan between legal entities, the basic conditions that must be observed by each party to the transaction are prescribed in the contract. If there are any violations, they are resolved with the help of the court.

There is no material benefit if funds are allocated for the purchase of residential real estate or the construction of a house. This also includes the situation when a company representative draws up a tax deduction from the purchased property.

Contract Drafting Rules

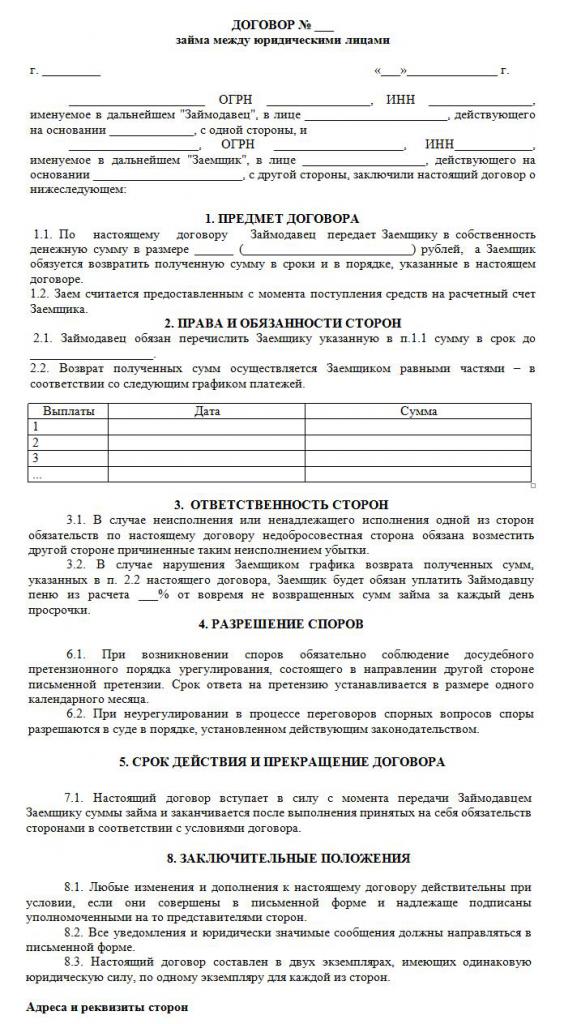

If funds are transferred free of charge, then an interest-free loan agreement between legal entities is certainly drawn up correctly. In its formation, numerous requirements are taken into account. The law does not have a certain strictly established form, so you can use the free form.

A document is written only in writing. Its essential condition is the absence of accrued interest and commissions. A sample interest-free loan agreement between legal entities can be studied below.

The main rules for the formation of this document include the following:

- drawn up exclusively in writing;

- signed by both parties to the agreement;

- since the parties to the contract are companies, they certify the signing of the document with seals;

- if the subject of the transaction is a monetary amount, it is directly stated that interest is not accrued on it, otherwise both participants will have unpleasant tax consequences;

- if property is transferred under the document, then no specific instructions are required; therefore, by default, such an agreement is considered interest-free;

- if an amount exceeding 600 thousand is providedrub., then such an agreement must be registered with state bodies.

Only when these facts are taken into account is it possible to correctly form a contract.

Essential conditions

When drafting this contract, certain basic conditions must be included. Additional information is agreed upon by two participants in the collaboration. According to the law, the conditions are necessarily included in the agreement:

- direct indication that the loan does not imply interest;

- the amount of money transferred is indicated, and it should not exceed 50 minimum wages;

- the transfer of money should not have any relation to entrepreneurial activity;

- a method of transferring money is given, as it can be issued in cash or transferred to the company account;

- The exact date when the money or other item must be returned by the borrower is indicated.

Based on Art. 809 of the Civil Code, it is possible to conclude such an agreement not only in the transfer of funds, but also in the provision of a certain thing that has some generic characteristics.

Other conditions in the contract may vary significantly depending on different situations. An important point is that each participant is vested with certain rights and obligations, which must be strictly observed. Therefore, if the recipient of the money is not able to return the money in a timely manner, then he will face numerous negative consequences of an interest-free loan between legal entities. The main negative point is the possibility of confiscation and sale of his property. The funds received from this process are sent to the creditor to pay off the debt.

The nuances of the formation of the contract

An interest-free loan between legal entities will be correctly executed only if there is a correctly drawn up contract. During its formation, the following features are taken into account:

- the parties are not allowed to be interdependent, since otherwise they could attract the attention of such an agreement to tax inspectors or employees of other government bodies;

- the model contract contains both essential and additional conditions;

- if there are no important conditions, then such a transaction will be considered invalid;

- the full name of both companies involved in the transaction is indicated;

- lists the rights and obligations arising from enterprises after signing such an agreement;

- each party’s liability is provided in case of violation of the terms of the agreement;

- methods are prescribed by which companies can solve problems or force majeure, and it is usually indicated that representatives of organizations should initially try to resolve issues in a peaceful way, and only then go to court;

- reasons are given for early termination of the contract.

If you correctly draw up the contract, indicating important information in it, then this document will not attract the attention of the competent authorities. Only on the basis of such a document interest-free loans are issued between legal entities. A sample contract is located below.

Amount Limitations

Under the law, there are no requirements or restrictions on the amount disbursed by an enterprise of another company. It is determined only by agreement of the parties. But at the same time, there are some requirements for the process of transferring money, which can be performed in cash or non-cash. The taxation of interest-free loans between legal entities depends on this. Therefore, the following rules are taken into account:

- if the transaction assumes that the money is paid in cash to the organization’s cash desk, then at a time it is impossible to use an amount in excess of 100 thousand rubles. under one contract;

- if the borrower needs money in excess of 100 thousand rubles, then it is necessary to draw up several contracts or transfer funds in non-cash form;

- if a non-cash method of transferring money is used, then with an amount of more than 600 thousand rubles. it is imperative to register the drawn up contract.

In case of violation of the above conditions, an audit will be carried out in respect of both parties to the transaction. This can lead to the fact that organizations will be held accountable for identified violations.

Is there a material benefit?

The tax consequences of an interest-free loan between legal entities should be taken into account by each participant in the transaction. A company that receives money for use without interest, has a certain benefit from this process. Therefore, the profit should be taken into account by the enterprise when calculating the tax base for income tax.

The accountant must correctly understand how this material benefit is calculated correctly. Since no interest rate is indicated in the contract, the Central Bank refinancing rate is used in the calculation.

Material benefit is calculated by the formula: material benefit = refinancing rate * 2/3 * amount of debt / 365 * loan term in days. The resulting value is included in the tax base necessary for calculating the corporate income tax. The calculation procedure will be performed on the day when the loan amount is fully repaid to the lender. It does not take into account how the debt was repaid, therefore, the amount can be paid in installments or in a lump sum payment at the end of the term specified in the contract.

If the tax on the amount received is not paid, the tax inspector may hold the company accountable. This risk of an interest-free loan between legal entities should be taken into account by each organization.

Taxation of parties to a transaction

Each company accountant should know how to get an interest-free loan between legal entities. Taxes are paid exclusively by the party that received any material benefit from this process.

A company issuing money without interest accrues no profit, therefore it has no tax consequences.

The borrower receives the benefit due to the lack of interest, therefore, based on the refinancing rate, the benefit is calculated, after which it is added to the tax base for the corporate income tax.

According to Art. 25 of the Tax Code, many enterprises through the courts try to prove the absence of the need to pay tax. To do this, they turn to the arbitration court. In judicial practice, there are indeed cases where the court satisfied the claims of the plaintiffs, so borrowers were exempted from paying tax, but in most cases representatives of the Federal Tax Service proved that the company had material benefits.

Errors in the preparation of the document

It is important to correctly draw up an interest-free loan agreement between legal entities. The founders check the correctness of the formation of the document, since if there are errors in it, then this may become the basis for its challenge.

The most common mistakes:

- there is no clause that the loan is interest-free, which leads to the fact that even the lender has a need to calculate and pay income tax, as employees of the Federal Tax Service will be sure that the company receives interest;

- the date when the funds should be returned is not indicated, which leads to difficulties in the process of debt collection;

- the parties to the transaction are interdependent persons, therefore, each party has tax risks.

To prevent errors in such a complex and specific contract, it is recommended to use the help of a lawyer in the process of drafting it.

Nuances of contracting between related companies

An interest-free loan between interdependent legal entities gives rise to numerous tax risks.First of all, it refers to the fact that employees of the Federal Tax Service require the lender to pay tax, for which the benefits received from this process are assessed.

Additionally, such transactions are considered as a way to hide state revenues or use various fraudulent schemes. Therefore, unscheduled inspections can be conducted for both companies.

Can an IP be a participant?

Individual entrepreneurs are not legal entities; therefore, when drawing up various contracts with them, the rules applicable to citizens should be used. Entrepreneurs, as individuals, are required to pay personal income tax, so when you receive an interest-free loan from another company, a citizen has financial gain due to the lack of interest.

This benefit is calculated as 2/3 of the refinancing rate, after which the resulting value is multiplied by the amount of the received amount. The calculated indicator is divided into 365 days and multiplied by the number of days during which the entrepreneur can use the borrowed amount.

The calculation results in a tax base with which 13% is paid.

Conclusion

An interest-free loan may be concluded between companies and individual entrepreneurs. It does not require the borrower to transfer interest to the lender. The execution of such an agreement has many advantages, but it is important to remember the tax consequences for each participant.

It is not allowed to draw up such an agreement between interdependent companies, as this can lead to unscheduled inspections and the calculation of significant taxes and penalties. When drafting the contract, it is advisable to use the help of a lawyer to prevent possible errors.