Organizations that apply the simplified tax regime must file financial statements once a year. This obligation has appeared for them since the beginning of 2013, together with the entry into force of amendments to Law No. 402-FZ, which regulates accounting rules. Only organizations fall under this requirement, but individual entrepreneurs can still not keep accounting and do not submit financial statements.

Accounting reporting at the simplified tax system

As you know, reporting is tax and accounting. The main form of tax reporting under the simplified tax system is the tax return, which is paid in connection with the application of this system. In addition, organizations report on other taxes and fees of which they are payers. As for accounting reporting, there is no special form for “simplified workers”, that is, they are subject to general requirements. However, there is one caveat.

A simplified tax special regime has been introduced in order to provide preferences to small businesses. It can be used by companies that satisfy certain parameters in terms of income and number of employees. Therefore, in practice, most organizations using the simplified tax system are small businesses. And such subjects of economic activity can report not in classical but in abridged form.

Thus, if a company meets the criteria of a small business and applies a simplified tax system, it can submit financial statements in a simplified form. Otherwise, she must present classical reporting.

How to find out if a company on the STS is a small business

The law considers small those companies that fit such conditions:

- If there are legal entities within its founders, their share shall not exceed:

- 49% if the founder himself does not belong to the category of small companies or is a foreign legal entity;

- 25% if the founder is a municipality or a constituent entity of the Russian Federation, a charitable foundation, public or religious organization.

- Over the previous year, the company received an income of not more than 800 million rubles. All taxable income is taken into account.

- The average number of people working in the organization over the past year did not exceed 100 people.

In addition to these criteria, there are also special conditions prescribed in the law on accounting. For example, simplified reporting cannot be applied to organizations subject to statutory audits. And absolutely all joint stock companies are subject to it. Thus, the joint-stock company does not have the right to hand over accounting in an abridged version, even if it meets the criteria of small business. There is also a restriction on reporting in a simplified form for certain types of companies. For example, these are organizations from the public sector, housing cooperatives, microfinance companies, law firms and some others.

So, while satisfying all the requirements established for small businesses, the company can submit to the simplified tax reporting system on the simplified tax system.

What is the difference between full and abbreviated reporting

Classical financial statements consist of the following documents:

- Balance sheet.

- Reports:

- on financial results;

- on changes in capital;

- cash flow statement;

- for non-profit organizations - on the targeted use of funds;

- Explanatory note.

In this case, the main forms of reporting are the balance sheet and the report on financial results. Everything else is just an appendix to the two forms mentioned. So, small companies may not make these applications.Thus, for small companies on the simplified tax system, financial statements will include:

- Balance.

- Income statement.

As you can see, the number of forms that small companies can submit within the financial statements is significantly reduced. But the preferences do not end there. The reports themselves can be compiled in either a regular or a simplified form.

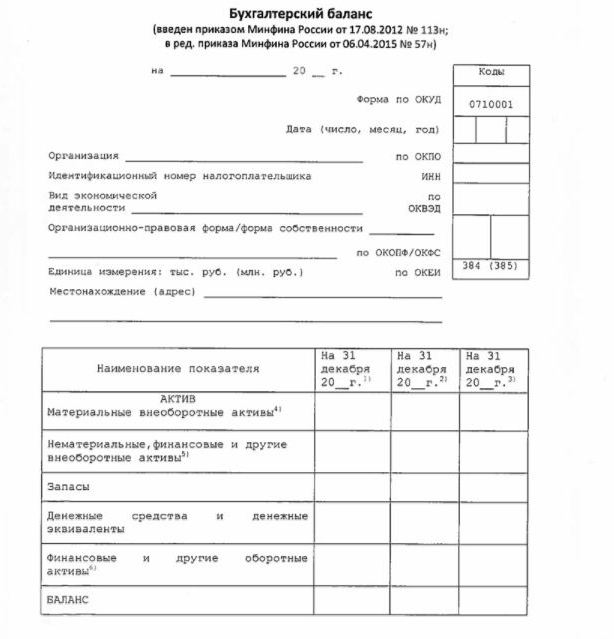

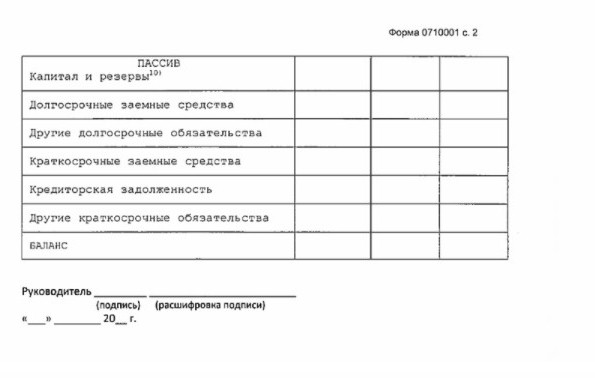

Simplified balance

The balance sheet in a simplified form shows the assets and liabilities of the organization in a rather enlarged form. Its form and drawing up procedure are given in the order of the Ministry of Finance No. 66n (Appendix No. 5).

The simplified balance, like the classic one, consists of an asset and a liability. However, the data in it is presented without granularity, so each of these sections contains only a few lines. The balance sheet includes information for the reporting and 2 previous years.

A sample of financial statements on the simplified tax system, namely its main form - a simplified balance sheet, is presented in the following image.

The source of information in the balance sheet is the accounting data of the company. For small enterprises, there is an opportunity to simplify not only reporting, but accounting itself. In particular, it is allowed to apply a simplified chart of accounts, not to use some PBUs, not to create reserves (except for the provision for doubtful debts), to correct accounting errors in the current period.

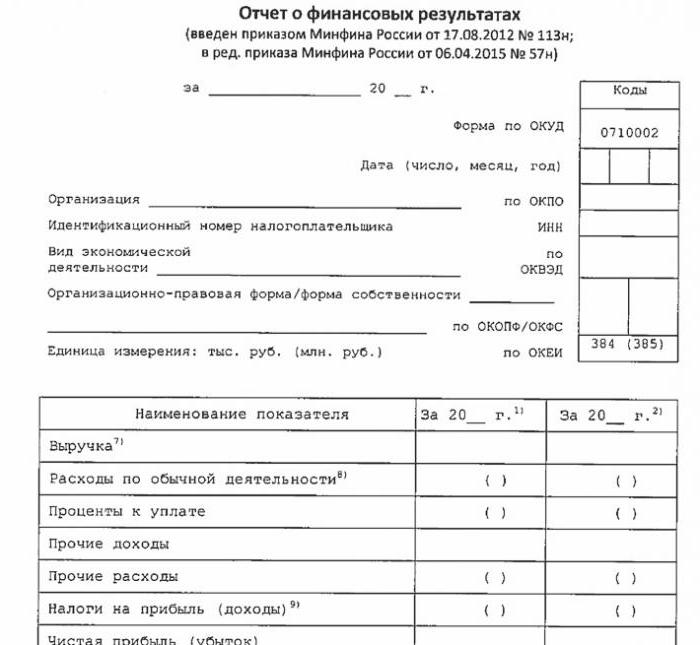

Simplified statement of financial performance

The simplified form of this report is also greatly reduced compared to the classic. In its tabular part only 7 lines. The report shall be reflected in revenue, expenses for the main activity, interest calculated on payment of any borrowed funds, other income and expenses, tax liabilities, as well as profit or loss. As in the balance sheet, the data are presented strengthened, without detail. The report includes information for the reporting and previous years.

The report form is shown in the following image.

How to report

Financial statements are submitted once a year. The deadline is no later than 3 months after the end of the reporting year. That is, reporting for 2017 must be submitted before March 31, 2018. As a general rule, if this date falls on a weekend, then the deadline is shifted to the next business day. The frequency and deadline does not depend on whether the company reports on a full program or a simplified one.

Since 2013, annual financial statements for the simplified tax system have been filed in two instances: the IFTS, where the company is registered, and the territorial division of the state statistics body. So, reporting should be done in at least three copies: one for each supervisory authority, and the third for itself.

Reporting is submitted on paper or electronically. In the second case, this can be done by TKS through a specialized operator company. Reporting to the Federal Tax Service in electronic form can also be submitted directly to the service website. To submit you will need an enhanced digital signature.

We also note that LLC LLCs are required to submit financial statements to the USN in the event that they did not conduct activities in the reporting year.

A responsibility

If the reporting is not submitted on time, this will result in a fine under article 126 of the Tax Code. For each unrepresented form, the organization will pay 200 rubles. A responsible official may also be punished - on the basis of Article 15.6 of the Code of Administrative Offenses, he faces a fine of 300-500 rubles.

For errors before the statistical authorities the punishment is more serious. In this case, Article 19.7 of the Code of Administrative Offenses applies, and the fine will be from 3,000 to 5,000 rubles for the organization. An official can also pay for his indiscretion - a fine of 300-500 rubles is prescribed for him.

Distortion of financial reporting data is severely punished if it is 10% or more, and the error has not been fixed before approval. In this case, a fine will be imposed on the official in accordance with article 15.11 of the Administrative Code of the Russian Federation and will amount to 5,000-1,000,000 rubles.

To summarize

So, if a company uses the simplified tax system, it can only submit financial statements in an abridged form if it meets the criteria of a small business. Otherwise, full reporting with all appendices and an explanatory note is submitted. Simplified reports are quite simple in structure compared to their classic versions.

The use of simplified forms is not imputed to legal entities from among small business entities, including those applying USN. Accounting for small enterprises is only a preference provided by law. To use it or not - each legal entity decides on this issue independently.