Accounting is the main type of accounting in the organization, as a result of which continuous, continuous, documented and interconnected registration of business transactions is carried out.

All business processes are recorded in accounting, due to which systematization and obtaining of a complete picture of them for certain periods are carried out. Primary business operations are recorded with primary documents, which gives accounting evidence of evidence, allow you to control activities, receive reliable and reasonable information.

To begin with, it is worth noting that if an organization performs not only processing of raw materials of a subcontracting type, but also the production of goods from raw materials of its own, as well as the subsequent sale of these products, it is required to keep separate records. This requirement is due to the fact that such operations should be reflected in accounting fundamentally differently.

This article will look at how subcontracting materials are accounted for in accounting.

What do such materials mean?

In the event that there is a transfer of raw materials for subsequent refinement, the owner of the specified property remains the dealer. In this case, the processor does not have the right to display the property of others in his balance sheet.

In terms of accounting accounts for the accounting of raw materials, as well as materials that were transferred to the organization for revision on a toll basis, there is a special off-balance sheet account. This account is called “Materials that have been accepted for processing” and has a serial number 003. In this case, the distinction is made between subcontracting materials that are directly in stock and materials that have already been transferred to production. These two types of materials are accepted for accounting on sub-accounts 003-1 and 003-2. Accordingly, they are called “Materials in stock” and “Materials in production”.

Quantitative and cost reflection

How is subcontracting accounting done? The document should reflect both the quantitative expression of the materials and the value. These data are contained in the documents accompanying the transfer of raw materials. In addition, it is necessary to organize accounting in the context of customers, the type of materials, their physical location.

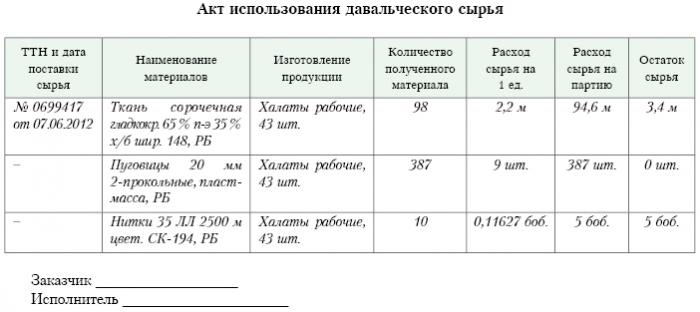

An invoice in the form of M-15, transmitted by the customer as supporting documentation for the transfer of materials, is the basis for accepting the material for accounting. The form of this consignment note is enshrined in law by resolution of the Goskomstat of Russia dated October 30, 1997 No. 71a.

It is necessary to pay attention that at the moment the unified form, reflecting the receipt of tolling materials in accounting, is not approved. In this regard, in the column “basis” in the consignment note it is necessary to make a note “on tolling terms under contract No. ...”.

Exactly the same mark should be on the receipt order of form M-4, which is issued by the processing company upon receipt of materials of a tolling nature. What is the subcontracting report? A sample is given below.

After work on the production or processing is completed, the final product is transferred to the customer. In this case, the corresponding act of acceptance and transfer, as well as the consignment note, must be drawn up. The processor must report on how he used the raw materials entrusted to him. If a surplus is formed as a result of processing, it can be returned to the customer.Although the contract may provide for a situation where the raw materials make a partial payment for the work performed.

Reflection on correspondent account

On the correspondent account 003 “Materials that are accepted for processing”, not only raw materials received for processing, but also finished products should be taken into account. The latter is reflected in this correspondent account until it is transferred to the customer.

Those costs that accompany the processing of materials should be recorded in the accounts for the costs of the implementation of production. Such costs include: the cost of personal materials that were used in the processing, salaries of employees, UST, expenses of a general economic and general production nature, as well as depreciation, which affects fixed assets.

Postings

The organization engaged in the processing of tolling materials in accounting should take into account all business operations. These transactions must be reflected using the following postings:

1. According to the debit count. No. 003 “Materials that are accepted for processing. This correspondent account reflects the total cost of all materials that have been accepted for processing.

2. According to the debit count. No. 20 “Main production” - on a credit account. No. 02, No. 10, No. 23, No. 25-26, No. 69-70. This posting reflects in the account all the costs that occurred to be in the processing of materials and raw materials.

3. According to the debit count. No. 90 "Sales", by subaccount. "Cost of sales" - on a credit account. No. 20 “The main production. This posting allows you to write off the costs that arise in the process of transferring the final product to the customer.

What postings still reflect the accounting of tolling materials?

4. By debit count. No. 62 - on a credit account. 90 "Sales", subch. "Revenue." This posting reflects the size of the revenue that was received as a result of processing activities. The important thing is that this does not take into account the cost of raw materials that are received from the customer.

5. According to the debit count. No. 90 “Sales”, for the “VAT” subaccount - for a credit account. No. 68 "Calculations made for taxes", subch. "VAT". This posting displays the calculation of VAT. But these are not all tolling transactions.

6. According to the debit count. No. 90 “Sales”, in the subaccount “Profit and loss from sales” - for the loan account. Number 99, Losses and Profits. This posting reflects the result in financial terms that results from the processing of tolling materials.

7. According to the debit count. No. 51 “Settlement accounts” - on the loan account. No. 62 "Settlements made with buyers and customers." This posting displays the operation to repay the receivables of the organization acting as a contractor.

8. On a credit account. No. 003 "Materials that are accepted for processing." This posting allows you to write off the total cost of all materials that have been accepted for processing from the customer.

Consider the posting data for a specific example.

Example

Suppose a manufacturing company, on the basis of a contract for tolling, received meat from a certain farmer, from which sausage should be produced with a total weight of 15 tons. The cost of this product will be 900 thousand rubles. The parties agreed that under the work contract they will be paid in the amount of 236 thousand rubles (of which VAT will be 36 thousand rubles).

In order to produce the above products, the meat-packing plant will have to use its own materials for a total of 40 thousand rubles. The remaining costs incurred in the production of goods amount to 83 thousand rubles, including:

• Salaries to employees totaling 50 thousand rubles.

• UST in the amount of 13 thousand rubles.

• Depreciation expenses equal to 20 thousand rubles.

Vesenny LLC must reflect all its operations in the following way:

1. Debit No. 003. The amount of 900 thousand rubles. Posting reflects the total cost of raw meat that has been accepted for processing.

2. Debit ct. No. 20 - Credit Account Number 10. The amount of 40 thousand rubles. The posting reflects the write-off of the cost of those own materials that were used.

3. Debit ct. No. 20 - Credit Account No. 02, 69, 70. The amount of 83 thousand rubles. This posting displays the total cost of producing goods from meat raw materials.

4. Debit ct. No. 62 - Credit Account No. 90.1. The amount of 236 thousand rubles. This posting shows the revenue that came from the production.

5. Debit ct. No. 90.3 - Credit account Number 68. The amount of 36 thousand rubles. Displays VAT calculation.

6. Debit ct. №90.2 - Credit account 20. The amount of 120 thousand rubles. This posting displays the write-off of expenses incurred during production.

7. Debit ct. No. 90.9 - Credit Account No. 99. The amount of 77 thousand rubles. This posting displays the total financial result.

8. Debit ct. No. 51 - Credit Account Number 62 The amount of 236 thousand rubles. This posting displays the receipt of funds from the farmer in accordance with the contract.

9. Credit 003. The amount of 900 thousand rubles. This posting represents the write-off of the cost of raw materials that have been processed.

As we can see, the organization should keep records of operations associated with the processing and use of tolling material on account 003, which is off-balance sheet. In this case, until the finished product is transferred to the customer, double entry is not applied.

How is accounting?

Accounting and analytics of tolling raw materials and materials on account 003 can be carried out both by customers and by type of raw materials, its evaluation.

As with any production, after processing materials, waste or surplus may be generated. An agreement may include several situations. Such waste may be returned to the contractor or may remain with the processor. But a report on the use of tolling materials must be compiled.

In the event that the contract provides for a situation in which the waste must remain with the processor, it is necessary to reflect the loan operations account. No. 003, reflecting the cost of raw materials that were transferred for processing, as well as to make simultaneous accounting for the account. No. 10 “Materials”.

Some nuances

It is worth paying attention to the following nuances. It is very important to consider this point: is there a decrease in the transaction price by an amount in the amount of the cost of waste that occurs as a result of processing, or does not occur. This should reflect the contract for tolling.

In the event that the waste arising from the processing of tolling raw materials must remain with the processor due to the partial repayment of the debt for the payment for processing, and they are recorded on the balance sheet, for example, as auxiliary materials, an account must be made in the account with the debit account. No. 10 “Materials”, according to subaccount. “Other materials” - under the credit account. No. 60 "Settlements made with suppliers and contractors."

In the event that the waste arising from the processing does not affect the amount of the transaction price, such an operation is considered as a gift operation. In this case, the account debit posting must be used. No. 10 “Materials”, to the sub-account “Other materials” - for the loan account. No. 98 “Income that will be received in the future period”, to the sub-account “Gratuitous receipts”.

After that, the cost of the waste will be gradually deducted as a result of their use in production. No. 91 “Other income and expenses”, subaccount “Other income”. In this case, the debit account posting will be used. No. 98 “Income that will be received in the future period”, to the sub-account “Gratuitous receipts” - for the loan account. No. 91 “Other income and expenses”, subaccount “Other income”.

Non-operating income

The cost of property received by the processor on a gratuitous basis, when maintaining tax accounting, should be included in non-operating income.These incomes are recognized on the date on which the signing of the act on the commissioned material, that is, the act of acceptance and transfer of such waste.

It is worth noting that when conducting tax accounting, income is generated in it earlier than when conducting accounting. It follows that the processing company is obliged to use PBU 18/02, as well as to record a tax asset of deferred nature in its accounting. The subcontracting report reflects this.

Settlements between the parties under the terms of the contract

From what form of calculation the parties use the contract to be submitted, the reflection of the settlements stipulated by the contract will depend. Settlements can be made using cash, by transferring raw materials to the appropriate amount or finished products.

Payment by cash

This option is the simplest possible. It is a classic scheme for the implementation of a contract: the processor takes upon himself the obligations to perform certain works, and the customer, in turn, takes on the obligation to pay for the work performed in cash. After that, a report on the tolling material is compiled.

The example that we examined above reflects just such a scheme for making calculations.

The mixed nature of the contract

In the event that payment is made by transferring raw materials or finished products (in full or in part), the nature of the contract is mixed: in the part where the work is directly provided, it is a classic contract, and in the part where it is reflected payment scheme, it is a classic contract of sale.

There are grounds for using such an interpretation. If we consider the rules by which the amount of payment is determined in accordance with an agreement providing for the fulfillment of obligations arising by non-monetary means, then it is necessary to be guided by “PBU” No. 9/99 pt 6.3. According to "PBU" No. 10/99 pt 6.3, it is believed that the amount of payment should be determined in the form of the value of goods that are transferred by the organization. If it is not possible to determine this value, then the value of the goods that are received is used. But on the basis of the essence of the contract itself, the organization engaged in processing does not actually transfer any goods, exchanging them for certain values. Formally, the transfer of tolling materials takes place, that is, the result that arose as a result of the processing of materials or raw materials. These products are not owned by the processor by ownership, and the very subject of the contract is the performance of certain works. Thus, the assessment of the cost of the work that the processor performs must be clearly recorded in the contract.

It is important to note that if a contract contains information that payment should be made by transferring raw materials or finished products, then it can be classified as a contract involving payment for work by non-monetary means.

In this case, when determining the price of work and the cost of raw materials transferred as payment, it is necessary to apply the rules that are established for contracts of this kind. That is, the cost of the work performed should be determined on the basis of the cost of the raw material itself, and this value is determined in a special way. For example, the cost of his own work can be determined by the processor based on the prices at which he independently acquires such raw materials, and this price can significantly differ from those at which the raw materials were purchased in this case.

Contract conclusion algorithm

To avoid such nuances, the following algorithm is recommended:

• An agreement should be concluded involving the processing of customer-supplied materials, which fixes the cost of the work performed, but does not contain information that payment will be made by transferring raw materials or finished products. In the event that the calculation will be carried out in this way, it is worth concluding a contract of sale for the amount that will be equal to the cost of the received raw materials or final products.

• Arrears should be offset. If the amount of the contract is the same as the amount of the contract of sale, then the offset is considered executed. If the amount of the contract of sale is less than the amount of the contract, then after the offset will be formed the debt of the customer, which is payable by cash.

Raw materials (partially or fully) will be transferred to pay for the work.

In the event that the customer makes a simultaneous shipment of raw materials for processing and raw materials at the expense of payment, the contractor will have to take into account the cost of the raw materials in the account. No. 45 "Shipped goods." It is precisely this account that is used, since in such a case the ownership of the raw materials passes from the customer to the processor upon the fulfillment of obligations to perform processing.

After the work is completed, the transfer of tolling materials and raw materials at the expense of payment for work should be reflected in the account. No. 91 “Other income and expenses” as a transaction for the sale of other assets.

The processor, in turn, must reflect the fact of receipt of materials, as well as raw materials as payment on account 002 “goods and materials that are accepted for safekeeping”. This account is off-balance sheet. Raw materials are reflected on it until the moment the work is completed.

How to write off tolling materials?

It is important to pay attention to the fact that in fact the same raw materials will be accounted for in two accounts: 003 and 002, but will have a different valuation. So, the raw materials that were accepted for processing will be accounted for in the amount at which it is reflected in the account. No. 10 at the customer, that is, at cost. And the same raw materials that were received for safekeeping as payment for the work performed must be transferred to the processor at the price at which it will be sold. In this case, the margin and VAT are taken into account. That is why all the raw materials received can be reflected on account 003 only if all the transferred raw materials go into processing, and its surplus arising from the processing will then remain with the processing company to pay for the work that has been completed.

If the raw materials transferred on account of payment will be shipped after he has completed the work, then the customer needs to reflect the write-off of tolling materials as per invoice. No. 90.2 “Cost of sales”, without using the invoice. No. 45 "Shipped goods." The processor, in turn, must reflect the raw materials received on account 10 “Materials”, and without intermediate use of off-balance account No. 002 “Materials and materials accepted for safekeeping”.

So, we examined the tolling materials, how to draw up a report on their use, also described in detail. We hope you find this information useful.