Often, borrowers are faced with the fact that their debt repayment costs are significantly higher than the actual amounts indicated by a smiling loan officer and enticing inscriptions on advertising banners. In order to present your real costs of repaying a loan, first of all, you need to calculate the effective interest rate. What is it and how to calculate it, we will tell in this article.

The effective interest rate is ...

Effective rate of interest has many definitions, but they all reveal the same essence from different angles. It:

- Credit rate, which includes all the costs of servicing a loan, insurance programs, commissions, etc.

- Compound annual interest rate, which is the value of the estimated profitability of a particular financial transaction.

- The real value of the loan, which contains all the costs of the borrower during the repayment of the debt.

- Actual value of the loan in excess of the nominal rate.

To better understand the essence of the effective rate, later we will draw a small parallel with the announced nominal.

What includes EPS on cards

We warn you that the highest effective interest rate awaits you when applying for a credit card so popular today. EPS will contain:

- Payment (commission) for the release of "plastic".

- Card maintenance fee.

- Current account maintenance fee.

- Commission for transactions on the card.

- If appropriate, a currency conversion fee.

- In case of violation of the terms of the loan agreement - a penalty for exceeding the limit or late payment.

- And, in fact, paying off the amount of debt and paying interest on it at a nominal rate.

The following conclusion can be drawn from this: do not stop at the bank offering the lowest nominal rate. Perhaps in another organization, where this figure is slightly higher, the effective rate will be several percent lower. What could be the reason for this? Due to the lack of a number of commissions (for example, for conducting a r / s, issuing a credit card), “voluntary-compulsory” purchase of insurance products for a lower amount, etc. Do not hesitate to ask a loan officer to voice the EPS. And only on the basis of this value to select the lender.

Nominal and effective interest rate

The nominal rate is a fixed amount, the size of the annual overpayment for the loan, which you see on attractive advertising brochures. It does not include the cost of insurance, commissions, credit card servicing fees - all those expenses that you have to incur along with paying interest on the loan and paying off the loan.

Why is the client not immediately voiced the amount that is equal to the effective interest rate? Firstly, this value is very difficult to calculate in advance. For example, if a client is late in payment or several installments, this amount will change to a larger side from the one that will be calculated first, due to the accrual of interest. And secondly, the bank will simply lose customers if it announces to them all their real expenses.

The fact that the loan officer tells the client only the nominal rate is not a hoax or "brainwashing." Surely in your loan agreement the overpayment enticing you is called that - the nominal interest rate. Alas, this borrower’s omission is that before concluding the contract he didn’t ask the operator at least the approximate amount of the effective annual interest rate.

Nominal and effective rates relative to deposits

As for bank deposits, here is a completely different situation:

- Nominal interest rate - A fixed amount of your annual income, expressed as a percentage. For example, 9% per annum.

- Effective interest rate - This is a floating value of your profit, depending on some conditions prescribed in the contract. As for deposits, it is higher than the nominal rate. This is primarily characteristic of deposits with capitalization (“compound” interest, interest on interest), when the amount of accrued interest is added to the deposit amount after a certain period, and over the next period of time, interest is accrued on this already increased monetary value. A deposit with 9% per annum with capitalization will bring much more profit than the same without capitalization. It is important to take into account its periodicity: if it occurs every month, then it is much more profitable than the case when "compound" interest is calculated once every six months.

And now let's move on to the "sick" issue - loans.

Effective Interest Rate Features

EPS must be prescribed in the loan agreement - this is prescribed by the Central Bank of Russia. But many are faced with the fact that their real costs are much higher and this value! This is due to the fact that the bank calculates EPS according to the formula proposed by the Central Bank of the Russian Federation, which has a number of drawbacks - insurance premiums and some of your other losses are not taken into account.

We warn you that the effective interest rate is a value that will always be higher than the nominal even for an idealistic model of a bank that does not offer insurance packages, commissions. The reason is that here, as well as for deposits, there are “compound” interest and annuity payments: one part goes to pay off the body of the debt, and the other to interest on it. That is, for each month, interest is accrued not only on the amount that you borrowed from the bank, but also on the amount of interest you have not yet paid.

Effective Interest Rate Calculation

The surest way to present your loan repayment costs as accurately as possible is to determine the effective interest rate yourself, using the ready-made formula. First of all, you need to clarify with what period the interest on your loan is accrued - every month, quarter, year, continuously, etc. Well, of course, you need to know the nominal loan rate.

Next, use the following formula:

E = (1 + N / P)P - 1, where:

- E is the effective interest rate:

- N - nominal rate;

- P - the number of interest calculation periods for one year.

If interest is accrued continuously, then another formula will work:

E = eN - 1, where:

- E - effective interest rate;

- N - nominal rate;

- e is a constant number equal to 2.718.

Alas, the above formulas do not provide for the inclusion in the result of expenses that you will definitely incur in connection with the purchase of insurance products, and issuing certificates.

The second way to calculate EPS

Another formula by which you can calculate the effective interest rate is as follows:

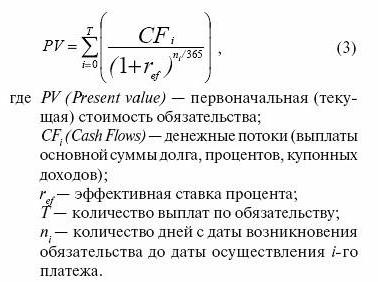

0 = (geometric progression) PV / (1 + EPS)(DP - D1) / 365 , Where:

- PV - the size of the last payment;

- EPS - effective interest rate;

- DP - date of the last loan payment;

- D1 - date of the first loan payment.

The calculations are complicated by the fact that to find the EPS you need to solve this equation.

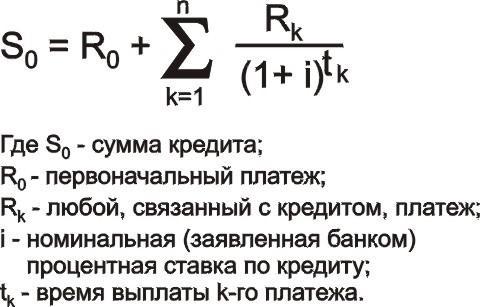

Another version of the formula:

K = P1 + ((geometric progression) Pn / (1 + EPS)ATn , Where:

- K - loan amount;

- P1 - first payment on the loan (it is necessary to take into account all commissions, insurance payments);

- Pn - the last payment on the loan (it is also necessary to include not only the amount of repayment of the body of the debt and interest on it, but also all incidental payments);

- EPS - effective interest rate;

- ATn - time of the most recent payment.

- n - month of payment on the account (12th, 15th, 36th, etc.)

Alternative counting methods

The effective interest rate formula is not the only way that will show you your real expenses:

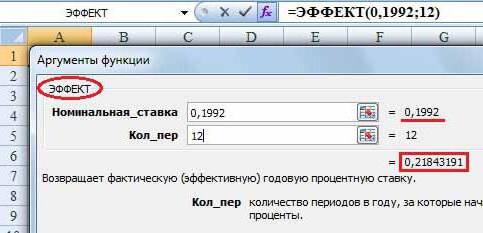

1. Use online calculators, in excess of those presented on the Web, from simple to very detailed, taking into account all payments.

2. Refer to the Exel program:

- The EFFECT () function will help you make calculations using the first formula.

- SERIESSUM is useful for calculations using the second formula.

Thus, it can be noted that, even knowing the nominal rate, the size of all commissions and the cost of insurance products, we ourselves (as, incidentally, a loan specialist) will be able to calculate only the approximate value of EPS. Independent settlements are complicated by "complex" interest, annuity payments, interest charges in case of late payment, which cannot be predicted in advance.