The most important place in ensuring the effective functioning of the tax system of the Russian Federation is occupied by tax authorities. According to the current legislation, it is advisable to include the Federal Tax Service and the Ministry of Finance of the Russian Federation, including their structural units operating in the country. In this article, we will focus on the powers, functions and organizational structure of the Federal Tax Service.

Structure

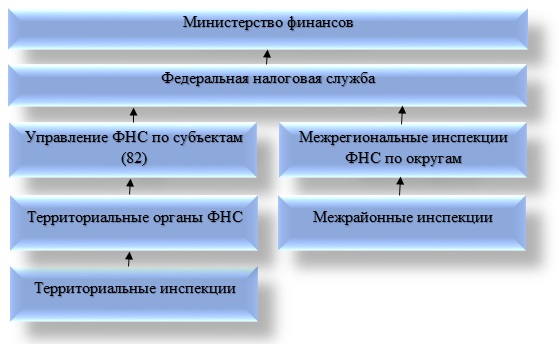

The modern system of bodies for taxes and duties in Russia is built in accordance with the national-territorial and administrative division, which was adopted by the legislator. It consists of four levels. Each link in the system and its elements has its own specifics and functions.

The central structure of tax administration in the country is considered to be the Federal Tax Service of Russia. The Ministry of Finance of the Russian Federation plays an important role. The Federal Tax Service has subordinate organizations in the entities under the jurisdiction of the Federal Tax Service of Russia, as well as territorial departments and inspections of the inter-regional level. Do not forget about inter-district formations.

The structure of the Federal Tax Service of the Russian Federation is rather concise. Consider each of its components in more detail. In this case, the federal service should be understood as the executive authority that is engaged in the registration of entrepreneurs and legal entities, as well as bankruptcy cases. It is important to note that it is the FTS that sets tax rates. The management of the service may appoint and dismiss the Government of the Russian Federation on the proposal of the head of the Ministry of Finance.

Interregional inspections, which are part of the structure of the Federal Tax Service of Russia, are formed to exercise control over the largest taxpayers. It is interesting to know that each inspection deals with control over representatives of only one industry. The departments of the Federal Service for Subjects (abbreviated as UFNS) are the components of the regional level Federal Tax Service. Their duties include ensuring control in a methodological plan, as well as coordinating the activities of lower authorities.

Another important element of the structure of the Federal Tax Service is considered to be inter-district inspections. They are engaged in the control of tax accounting of taxpayers at the regional level. It should be borne in mind that such inspections are subordinate not only to the Federal Tax Service, but also to the Federal Tax Service in accordance with the subject. The territorial inspection for some classifications is also included in the structure of the Federal Tax Service of Russia. This body exercises tax control in municipalities. We are talking about cities, districts or small towns, not separated in more detail.

As it turned out, the structure of the inspection of the Federal Tax Service of Russia implies the existence of four levels. Among them are federal, federal-district, regional, as well as local levels. The presented hierarchy is fully consistent with the state administrative-territorial division.

Supervision and control by the Federal Tax Service of Russia

The structure and functions of the Federal Tax Service are interrelated categories. Among the control and supervisory functions, it is advisable to distinguish the following:

- Compliance with the law in force in the country regarding taxes and fees.

- Correctness of calculation, timeliness and completeness of taxes and fees to the relevant state budgets. It is worth adding that this paragraph also applies to other payments that are mandatory.

- Supervision in the field of production of ethyl alcohol, alcoholic and tobacco products.

- Strict compliance with currency laws within the competence of tax structures.

- Informing taxpayers regarding tax legislation issues, as well as explaining the tax system in force in the country, if necessary.

Executive Body Functions

Each of the elements of the management structure of the Federal Tax Service of Russia has its own functions. You should be aware that the Federal Service is an authorized executive body of federal significance, which implements the following functions:

- state registration of individuals as individuals, as well as legal entities;

- Representation in cases related to bankruptcy and related procedures of requirements for making payments of a mandatory plan, as well as related to monetary obligations.

Features of the activity

The constituent structures of the central office of the Federal Tax Service are under the jurisdiction of the Ministry of Finance. In the course of its activities, the Federal Service is guided by the Constitution of the Russian Federation, acts of the government and the president, constitutional laws of the federal level, regulatory acts of the Ministry of Finance, international agreements and, of course, the Regulation on the Federal Tax Service.

The structures of the Federal Tax Service described above carry out activities both directly and through their territorial bodies, subject to interaction with other federal executive authorities, local government institutions and state extra-budgetary funds, executive bodies of the constituent entities of the Russian Federation, as well as public plan associations and other organizations.

At the head of the service is a leader who is appointed to the position and dismissed from it - as already noted - by the Government of the Russian Federation in accordance with the proposal of the Minister of Finance. The structure and powers of the Federal Tax Service are approved exclusively by orders. Each tax authority is an independent legal entity, however, at the same time, they are all subordinate to the vertical type and are included in a single centralized aggregate.

Structural Reform Attempts

The reform of the structure of the Federal Tax Service of the Russian Federation has an interesting feature. It is about creating inter-district and inter-regional formations. Unlike the inspections of the traditional plan, which exercise control solely on the territorial affiliation of each of the taxpayers, they organize their own activities based on the industry affiliation and the category of taxpayer.

It is worth noting that interregional inspections in federal districts occupy an intermediate position between the Federal Tax Service and its territorial departments.

The objectives of creating interregional inspections

Interregional inspections in federal districts included in the structure of the Federal Tax Service are created to achieve the following goals:

- interaction with authorized representatives of the President of the Russian Federation in federal type districts on issues that are included in their competence;

- full control over compliance with applicable laws in the country regarding taxes and fees in relation to a specific federal district;

- implementation of tax audits.

Authority issue

At the interregional level today, there are seven inspections of the interregional type for the largest taxpayers in the following areas:

- exploration, production, subsequent processing, transportation and sale of natural gas;

- exploration, subsequent extraction, refining, delivery and sale of oil, as well as oil products;

- turnover and production of ethyl alcohol and tobacco, and from all currently known raw materials of tobacco, alcohol-containing and alcoholic products;

- power industry, where it is advisable to include the production, distribution, transmission and subsequent sale of thermal and electric energy;

- production and sale of products of the metallurgical industry;

- the implementation of communication services;

- the implementation of transport services.

Subject Tasks

The described formation of the structure of the Federal Tax Service at the level of entities (territories, republics) perform the following tasks:

- full monitoring of compliance with legislation in the field of taxes and fees in the territory of a subject of the Russian Federation;

- ensuring the receipt of tax payments and other obligatory payments to the state budget.

You need to know that the leadership of the Federal Tax Service Office in the subject is appointed by the head of the Federal Tax Service of Russia after the mandatory approval procedure with the authorized representative of the president for a particular subject.

Today, two types of inspections of the Federal Tax Service of the inter-district level can be distinguished. Among them are the following:

- Inspectorates of the Federal Tax Service of Russia, which control the territory of not only but several administrative districts;

- inspections included in the structure of tax authorities (FTS), which exercise control over the largest taxpayers.

The latter are somehow subject to administration in the field of taxes at the regional level.

Powers of the tax authorities

In accordance with Article 31 of the Tax Code in force on the territory of the Russian Federation, tax authorities are entitled to:

- Demand from the taxpayer documentation on the forms that are established by government entities and local governments. These securities serve as the basis for the calculation and subsequent payment of taxes. Explanations, documents that confirm the correctness of the calculation, as well as the completeness and timeliness of the repayment of tax payments, are also appropriate in this category. It is worth noting that this right is exercised in the implementation of tax control. The current procedure for demanding documentation is discussed in the description of methods and forms of control in the field of taxes and fees.

- Organize tax audits in the order established by the Tax Code. It is necessary to add that they are visiting and cameral.

- For a certain period of time, stop operations related to taxpayer accounts in banking institutions and seize their property complexes in the manner prescribed by the Tax Code. In accordance with the law in force, operations on accounts are stopped, as a rule, if tax returns are not submitted within the time limits established by law. It can also be a measure that ensures tax payments to state budgets at various levels. It is worth noting that if the declaration is not submitted on time, account transactions are usually suspended immediately before it is submitted. Property may be seized in cases provided for by tax laws in force in the country.

- To seize documentation during a tax audit from a taxpayer, which indicates the relevance of tax offenses.

- Inspect (inspect) any taxpayer used to generate income or related to the maintenance of taxable objects - regardless of their location - warehouse, industrial, commercial and other territories and premises. Carry out an inventory of the property complex owned by the taxpayer. It is worth noting that the inspection of territories and premises is carried out exclusively within the framework of an on-site tax audit.

- Determine the amount of tax payments to be paid by taxpayers to the state budget or extra-budgetary funds.In this case, a calculation method is used based on available information regarding the taxpayer, as well as information about other similar taxpayers.

- In an indisputable manner, to recover tax arrears from legal entities, as well as penalties, in accordance with the rules established by the Tax Code. It must be borne in mind that today penalties can be exacted exclusively in court. More specifically: from individuals and individual entrepreneurs all types of arrears are also recovered only in court, and from legal entities in a judicial or indisputable manner.

- Require documents from banking institutions that serve as confirmation of the execution of payment orders by taxpayers. It is important to note that this requirement is carried out in the order of control of taxpayers who realize the repayment of tax payments, as well as banking institutions that transfer money to the state budget as tax agents.

- To attract experts, translators and other specialists to organize tax control. The procedure is fully described in the methods and forms of tax control.

- Call as witnesses persons who may be aware of certain circumstances relevant to the implementation of tax control. It is important to note that the witness has the right to refuse to testify in some cases provided for by legislation in force on the territory of the Russian Federation. It is compulsory to draw up a protocol for interviewing a witness.

Conclusion

So, we examined the organizational structure of the central apparatus of the Federal Tax Service of Russia, its functionality and authority. In conclusion, it should be noted that, in addition to an impressive amount of authority, the Federal Tax Service has a number of responsibilities. They are described in detail in article 32 of the Tax Code in force on the territory of the Russian Federation. The primary responsibility is compliance with tax laws. It applies to both tax authorities and their officials. In case of violation of the law, the taxpayer is entitled to recover losses that are caused due to unlawful actions of the tax service.