Personal income tax means personal income tax. The amount of income and tax withheld from it are entered into the document in the form 2-NDFL. Certificate 6-NDFL is considered a new form of employers' report, which indicates all taxes accrued, withheld and paid in total. Both forms of certificates have legal force in state organizations; there should be no discrepancy in 6-personal income tax and 2-personal income tax.

Many have questions about filling out reports. And if according to the first familiar reference everything is more or less clear, then confusion often occurs with the new form. In this article, we will figure out how to properly draw up and submit annual reports to the tax service.

About 2-PIT

This form is mandatory:

- Full information about the employer (company name, its details).

- Information about the employee (F. I. O., TIN, passport information, place of residence).

- Monthly income, 13% - this is his rate.

- Information about the deductions with their codes (standard deduction, social or property).

- Amounts of tax withheld.

- Total amounts (income, deductions and taxes).

Inquiries of this form give out:

- An individual with an income from which the employer is taxed.

- An individual with an income from which the employer is not taxed.

Filling out this certificate is carried out on a specially designed form. In the new form of the form in the upper left corner there is a bar code that was assigned in accordance with the rules. Further information is filled out in the following order:

- period for which the certificate is issued;

- tax agent (employer);

- employee information;

- information on income taxable at a rate of 13% (it is important to indicate the income code);

- tax deduction information;

- Information about the total amount of income and taxes.

How to fill it in correctly?

It is important to have information about the correct completion of the annual report of 6-NDFL and 2-NDFL, since it is accepted by the tax service of Russia, certificates of 2-NDFL are issued to employees at their request, for example, to the bank.

Amounts are recorded in rubles with the obligatory indication of kopecks, except for income tax. It is provided in full in rubles. If the amount is penny, then less than 50 kopecks. discarded, and more than 50 kopecks are rounded off, while a unit is added to the amount in rubles.

If different rates were applied to employee income during the year, respectively, paragraphs 3-5 will equal their number.

Actions for making a mistake in the help

There are times when there are errors in the certificate. In this case, you must act in accordance with the procedure for correcting errors. The title has a special field “Correction Number”. Corrections have their own numbers:

- “00” means filling out the primary form;

- “01”, “02”, etc., are indicated when completing the corrected certificate, which is issued instead of the previous one, by one more than indicated in the previous certificate;

- “99” means cancellation of the certificate.

The corrected form of the 2-NDFL annual report form is submitted to eliminate the error in the form that was submitted at the beginning, and the annulment form is submitted to cancel the data that are not necessary for submission. If the tax authority has not accepted the certificate (for this, errors with format control are indicated in the protocol), a new certificate is written, not an adjustment. Therefore, when filling out a new certificate, indicate the number “00” and the new date.

What is the deadline?

The certificate, where the income of the organization’s employees is indicated, must be submitted on time. The tax agent provides information on the income of employees according to the 2-NDFL certificate of the Federal Tax Service at the place of registration. The reporting will be the past tax period. It indicates the amount of taxes calculated, withheld and transferred to the budget of the Russian Federation.

The report must be submitted every year on time, in the form, format and order, which are approved by the federal executive services authorized for inspections and supervision in the field of taxes and fees.

Information should be provided in electronic form using telecommunication channels or in paper format (on electronic media). If, from the beginning of 2016, an enterprise paid income to 25 employees or more, it must submit 2-NDFL certificates for 2016 in electronic format using telecommunication channels through an operator engaged in electronic document management. You can’t use hard drives, flash drives, etc. If the employer has paid less than 25 employees in the tax period, certificates are provided in paper format.

These amendments are provided for in paragraph 2 of Article 230 of the Tax Code. They also relate to 2015 reports. Accordingly, if the employer transferred income to 25 employees or more in 2015, the information should be provided only via the Internet.

Information on the impracticability of tax withholding for 2017 must also be provided in electronic form if the employer transferred the income to at least 25 employees.

At the end of the year, the employer without fail provides a certificate, for example, 2-NDFL for 2016, to the inspection:

- Not later than the first of March with a mark of "2". Such a certificate is issued for those employees from whose personal income tax is not withheld (for example, providing financial assistance or giving gifts to people who do not work in the organization, in the amount of more than 4,000 rubles.

- Until the first day of April of the month with the mark “1”. Here is information on income in the total amount earned for the previous year, the tax base with which the personal income tax is withheld.

These are the deadlines for submitting the 2-NDFL annual report.

Help 6-personal income tax

Certificate 6-NDFL is a document for the submission of the statements of the employer paying income to individuals. It is presented in the form of a summary of general information on the income of employees for a certain period and on tax withheld from these amounts. Reporting is quarterly, that is, every three months. Reporting is required in electronic form. But if the organization has less than 25 employees, you can send it in paper format.

When issuing a certificate, you need to make sure that all the cells are filled. Blank columns are filled with a dash, both on the title page and on the second page. All tax agents are required to submit this form. These include individual entrepreneurs, lawyers, notaries. Revenues should reflect all individuals who work in the enterprise. Speaking of income, they mean salaries, dividends, remuneration under civil law contracts.

How to submit an annual report 6-personal income tax?

It is important to know that it is necessary to submit a report on an increasing basis, four times a year:

- in the first quarter;

- in half a year;

- at 9 months;

- in year.

In accordance with the law, quarterly reports on this form are submitted to the inspection no later than the beginning of the last day of the month following the reporting quarter. The annual calculation is sent before the first day in April of the following year. There is a penalty for late submission of a report. For each month of delay, the cost is one thousand rubles. So it is better to try to send reports on 6-personal income tax on time since 2017.

In paper form, such a certificate is only allowed to those organizations with less than 25 employees.

Sample certificate 6-PIT

The 6-NDFL annual report sample has been valid for about a year, but tax agents and accountants have many questions to fill out.

Help has a title page and a second page, which has two more sections. If there are not enough lines for the report, you can number additional sheets. Usually there is not enough space when filling out the second section, which is on the same sheet as the first. In this case, you do not need to copy the contents of the first section.

In the footer of the first sheet, the TIN and PPC of the organization that submits the statements are filled. If the information is provided by the branch of the company, then the checkpoint of the branch is filled out.

Under the heading is the line “Adjustment Number”, suggesting the ways in which the report is filled. If an error or inaccuracy is found in the report, they can be corrected by sending a modified version of the report. Accordingly, if the report is sent for the first time, three zeros are indicated in the necessary column. If it is necessary to clarify the calculations, indicate the numbers "001", "002", etc.

Previously, when submitting reports on personal income tax, the year was not divided into reporting periods, respectively, according to the Tax Code of the Russian Federation, the “reporting period” did not matter with respect to this tax. Now, the value “presentation period” is entered in the sample report, this is the deadline for submitting the annual report of 6-personal income tax for which the report is submitted.

The tax code is written below, in which the employer sends the statements. The code is four digits: the first two numbers are the region number, and the second two numbers are the inspection code. It must be remembered that the report is submitted to the inspection at the location of the enterprise or branch. Individual entrepreneurs submit reports to the tax office at their place of residence.

By the code in the line “By location (accounting)”, you can determine which organization submits a report. These codes are indicated in the Procedure for filling out the annual report 6-NDFL:

- where the Russian organization is registered - “212”;

- where the branch of the company is registered - “220”;

- large taxpayers indicate - "213";

Individual entrepreneurs have their own codes:

- IP on the USN or the general system - "120".

- IP on UTII or patent - "320".

In the line about the tax agent indicate the name of the organization. You can also indicate a short name, if any.

When filling in the All-Russian Classifier of Territories of a Municipal Formation (OKTMO), it is mandatory to indicate the education code on the site of which the organization or its branch is located and registered (upon delivery of the report for the branch). That is, the code of the annual report is 6-NDFL. It happens that employees receive income, for example, wages, bonuses, etc., both from the parent company and from its unit. In this situation, inspections provide two calculations with different codes for OKTMO.

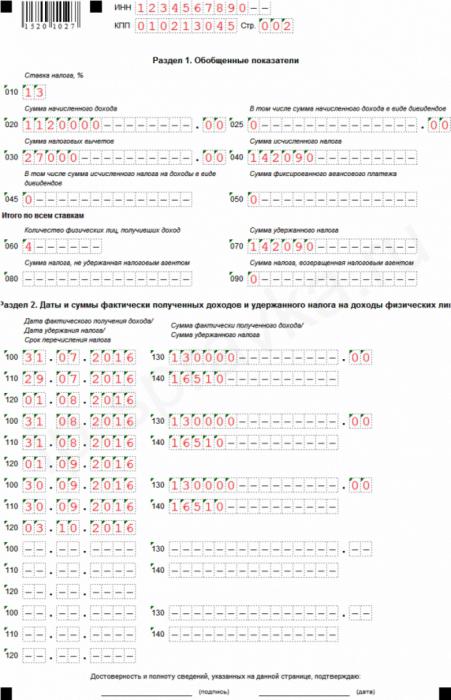

The second page of the help 6-personal income tax

On the second page of the help there are two more sections to fill out, each of which in turn is further divided into subsections.

In the first subsection of generalized indicators, the tax rate that is used in the organization is indicated. At one enterprise, employees are taxed at several rates. The basic rate is 13%. The rest, high rates, are used in relation to individuals of non-residents of Russia (15 and 30%), and in relation to winnings in the lottery, competition or advertising campaign (35%). If the organization uses only the basic rate, then the section is filled once.

The second subsection summarizes the results for all used income tax rates.

The second subsection indicates the totals. The line contains the number of employees who received accruals for the period. In cases where the employee quit and then returned to the organization, the information does not change.

There are cases when the tax withheld in the 6-NDFL and 2-NDFL annual reports does not coincide with the amount of the calculated tax.This happens due to the fact that some tax amounts were transferred earlier, and withheld from employees later.

Also indicate the amount of personal income tax, which could not be held for some reason.

The second section of the 6-personal income tax for the last quarter contains information, that is, the period from the beginning of the year does not count. Here are filled in the dates of accrual of income to employees and their amount. Dates are indicated in chronological order:

- The date on which the employee received the income. The indicated date and month depend on the type of payment. The day that the employee earns the income also depends on this type. Salary, therefore, is the income of an individual received at the end of the month (issued on the last day) for which it is paid, that is, the last day is indicated, for example, January 2017, and the employee received his salary for this month in February. Vacation and sick leave are income on the day they are received.

- Date when tax is withheld by the company. To take personal income tax from earnings is necessary on the day it is paid. The employee income tax on vacation or sick leave is also withheld by the company on the day they are paid.

- Date of tax deductions to the budget in accordance with the law. Salary tax must be paid to the budget the next day after payment, not later, but from vacation and sick leave until the end of the month when they are paid.

- The amount that employees received on a specific date, without tax.

- The amount of tax withheld upon the payment of income to employees on the date of tax withholding by the enterprise, regardless of transfers to the budget.

When checking 6-NDFL and 2-NDFL, it is necessary to check their internal data, but also to compare the sample 6-NDFL with other reports, and with information from accounting and tax registers.

The Tax Code of the Russian Federation determines the timing for the provision of information on the income of employees of the organization and the amount of tax withheld, calculated and transferred to the budget of the Russian Federation for the year for each employee on the annual report 6-NDFL and 2-NDFL.

The deadlines for the submission of these reports are the same: no later than the beginning of April of the year that began over the past tax period. If the last reporting day falls on a weekend or public holiday, filing is permitted on the next business day after it. For example, if the first day of April falls on Saturday, then the deadline for reporting on forms 2-NDFL and 6-NDFL on the 3rd.

Compliance of annual reports 2NDFL and 6 personal income tax

Not only the deadlines combines these reporting. A letter from the Federal Tax Service of Russia indicates control ratios for them.

For the annual calculation of 6-personal income tax, the final ratio is applied to the annual reference 2-personal income tax, which has the attribute “1” (indicating the total amount of income earned by the employee for the previous year, the tax base from which tax amounts were withheld). Since the 6-personal income tax certificate contains generalized information, and the 2-personal income tax certificate is filled out separately for each employee who earned his income in the enterprise as a salary, when checking 6-personal income tax and 2-personal income tax, they should have some data:

- The number of employees who earned income for the reporting period should not differ from the total number of certificates issued 2-NDFL.

- At tax rates (each of them), the accrued income must be equal to the total of the lines “total income” for all 2-personal income tax certificates, and the tax rate will be exactly the same.

- Dividend income must be equal to the amount of the same income for all references 2-PIT.

- The full tax that is withheld from the employee’s total income in rubles without kopecks should be equal to the sum of the line “tax amount calculated” for all forms of 2-personal income tax with the corresponding rates.

- An individual’s tax not withheld for any reason should be equal to the amount of tax that the tax agent did not withhold in all certificates.

In the reports in 6-personal income tax and 2-personal income tax discrepancy is not allowed.

2-personal income tax and 6-personal income tax in accounting

In the 1C accounting program, a tax on income tax is generated on the basis of data received from the 1C: ZUP program. There, information for the statements of 2-NDFL and 6-NDFL on dividends is generated on the basis of the documentation.

When using the 1C accounting program, you don’t have to worry about fulfilling the ratios in the annual report of 6-personal income tax and 2-personal income tax. An automatic reporting mode guarantees a mandatory automatic compliance with all necessary control ratios. To do this, you need to monitor the current version of the program and update if necessary.

By filling out sample reports, the accountant is required to check all the information entered to be sure of the correctness and reliability of the information provided. The annual report of 6-personal income tax and 2-personal income tax should be the same. If there are any discrepancies, the Federal Tax Service has the right to send the employer an order to make adjustments to the Calculation, or to submit written explanations for a period of five days. Also, if an error is detected in the Calculation, the Federal Tax Service has the right to recover a fine from the employer.