Verification of calculations must be carried out without fail by all enterprises, this is required for the preparation of an accounting report, as well as an inventory of settlements with debtors and creditors, for example, may be required for third-party interested parties as additional information. The inventory process is not strictly regulated, but it should be carried out carefully, indicating all obligations - both internal and external.

General rules for conducting an inventory of settlements

An inventory of receivables and payables or an inventory of settlements, which, in principle, is the same thing, is carried out practically according to the same rules as the inventory of the warehouse, but with certain features. When conducting an inventory of settlements, a special commission is created, an order is issued, and all procedures are strictly controlled. The sequence of this process is prescribed in the accounting policies of the institution. According to the results of the inventory of settlements with debtors and creditors, an act is formed. It is reflected in accounting. In the process, you need to check the following calculations:

- with counterparties;

- with employees (bonuses, advances, bonuses, salaries and compensations);

- with accountable citizens;

- other payments to employees (from financial liability for arrears to a loan issued);

- inventory of settlements with other debtors and creditors (for example, under lease agreements or requirements);

- internal corporate settlements (for example, between different trading points);

- with banking institutions for loans and borrowings;

- with budgetary and extra-budgetary funds (insurance, taxes and fees).

The main distinguishing features of the inventory of calculations from the same warehouse check are that persons with material liability cannot enter the commission. Verification of calculations is carried out based on the results of the work in the process of preparing annual reports. To simplify the task, an inventory can be carried out more often, this will help to more accurately represent the state of affairs. The results of the audit are displayed in the accounting and reporting of the period when it is completed.

An inventory of settlements with debtors and creditors is required first of all to the company management in order to understand the actual state of affairs. In fact, the results of such a check provide accurate information about where and at what point the money is located. The correct use of an automation program will help to avoid frequent checks. With regular entry into the program of information on all financial transactions, you can easily collect the required forms in the report. Thus, you will receive all the necessary information for making decisions without additional verification costs.

The procedure for the inventory of settlements with debtors and creditors

An inventory of settlements with debtors is carried out as part of the management of receivables and provides data for its analysis. Consequently, an inventory of accounts payable is an element of the management of accounts payable and a source of information for the analysis of accounts payable. The debt inventory procedure makes it possible to understand the following:

- the amount that needs to be urgently requested (in the inventory of settlements with customers);

- Amount for urgent payment (in relation to verification of settlements with banking institutions and suppliers).

In the process of inventorying settlements with manufacturers and consumers, it is first of all necessary to analyze unbilled deliveries (those products that have already been received but not yet paid) and paid but not yet delivered (the opposite is the case - the goods are paid for but not yet received). The inventory commission is studying the acts of reconciliation of settlements.

Types of debt

Conducting an inventory of settlements with debtors and creditors will reveal whether you have outstanding debts subject to penalties. In addition, you should make sure that this debt is recorded correctly, since it can be of several types:

- short-term (delay less than 1 year);

- long-term (non-payment longer than 12 months);

- overdue (recorded separately).

In the process of checking settlements with banking institutions, credit agreements are checked first. Among other things, during the inventory of settlements with creditors and debtors, the following contracts are checked (if any):

- rent;

- commissions;

- assignment of rights of claim (cession);

- errands.

Dates and Tasks

An inventory of settlements with debtors and creditors is carried out in a number of cases:

- before the preparation of annual reports;

- in the process of changing financially responsible persons (for example, chief accountant);

- in case of emergency (natural disaster, fire, etc.);

- upon liquidation or reorganization of a company.

In addition to the mandatory inventory of settlements, the organization has the right to describe accounts receivable and payable in terms that are most relevant to accounting needs for management and so on. For example, if the rules of the company provide for the quarterly formation and submission of reports to the founders, then it is reasonable to check the settlements on the final day of each reporting stage. The inventory system in this case should be spelled out in the accounting records of the organization.

The task of both planned and voluntary verification of settlements is:

- the establishment of debt amounts appearing in the accounts of accounting, confirmed by documents;

- assessment of accounts payable and receivables for possible repayment, that is, consideration for doubtful and bad debts.

It follows that the calculation inventory procedure involves not only the verification of accounting information with the primary documentation, but also a further study of the results.

Who is a member of the commission

To compile an inventory and conduct an inventory of settlements with different debtors and creditors, a special commission is created that operates on a long-term basis, which can be of two types:

- commission organized upon the occurrence of certain conditions;

- inventory team appointed by the company’s manager.

The following specialists may be included in the commission:

- authorized administrative department (AHO);

- accounting specialist;

- other employees (engineer, lawyer, financier, etc.).

The only exceptions are employees of the internal expertise of the company and representatives of the audit organization.

The leading person of the enterprise is not included in the commission, but his presence is an indispensable condition.

Commission Objectives

The primary tasks of the verification team are as follows:

- statement of the situation on the status of settlements with debtors and creditors;

- checking the correct price range;

- formation of an act on the results of the audit.

An act of inventory of settlements with debtors and creditors is required in order to comply with settlements with manufacturers, contractors, consumers and customers.

Reporting

In 2013, Federal Law No. 402 was adopted.Part 4, article 9, speaks of independent development by companies of the form of primary accounting documentation, which also includes documentation on conducting an inventory of settlements. The established forms, as mentioned above, must be reproduced in the accounting policy of the company and certified by the general director. Most institutions did not “invent a bicycle” and took the following forms of documents as a base:

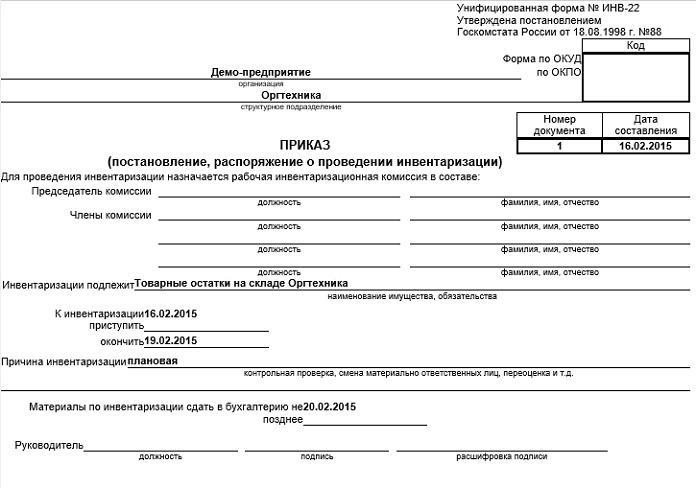

- an order to conduct an inventory of settlements with debtors and creditors (a sample can be found below) according to INV-22 type;

- an act of verification of settlements with consumers, manufacturers and other debtors, and creditors with an investment in the form of a certificate (INV-17 form).

Additionally

Because an inventory of settlements with debtors and creditors is also carried out to identify doubtful and bad obligations, it makes sense to add additional information to the annex to the act.

1. To establish doubtful obligations:

- payment delay period in days;

- availability of collateral.

The line “For what debt” marks: debt obligations are associated with the sale of goods, services and work or not, because this criterion is the most important condition for classifying debt as doubtful.

2. For the disclosure of bad debts:

- beginning of the limitation period (in most cases, this date does not coincide with the period of arrears, which is determined by the terms of the agreement);

- information on the interruption of the limitation period (number and basis);

- data on the expiration of the limitation period (including interruption);

- the reasons why the debt is recognized as hopeless.

The above information will help you to easily calculate the amount of doubtful receivables in order to create reserves for doubtful debts, as well as establish the amount of bad debt for subsequent write-off. In addition, the results of the verification of calculations will be very useful in the process of company management.

The procedure for writing off receivables

Debt obligations to debtors are written off in several steps:

- Each debt amount is written off separately, using the counterparty or agreement.

- The relevant documentation is drawn up.

- The total values of the inventory are entered into the database.

- An order is issued indicating the amount of debt that will be written off.

- The documentation is endorsed by the head.

Accounts Payable Procedure

The write-off process also contains several steps:

- Preparation of documentation confirming the fact of delay.

- The amount to be paid is agreed upon.

- The bill of lading is being verified.

- Checking the certificate of completion.

- The paperwork is drawn up to verify the debt.

- An inventory of settlements with debtors and creditors is compiled.

- Documents are certified by the General Director.

Conclusion

An inventory of settlements requires a detailed analysis of financial transactions with each counterparty on the basis of a single agreement or other document. To do this, the finance department reconciles the balances on certain accounts. An objective assessment of accounts payable and receivable helps to verify the calculations with the budget and counterparty.

We must not forget that the results obtained should be properly reflected in the accounting documentation of the company.