Today we have to find out what features IP has on UTII and on STS. These two taxation regimes often attract citizens. And so you need to know about them to the maximum. After all, the wrong choice of a tax payment system often leads to a loss-making business. This, in turn, does not have the best effect on the Russian economy. Therefore, each entrepreneur must decide how he will pay taxes when starting a business. What is provided for at UTII and at STS? What points should you pay attention to first of all?

UTII is ...

To begin with, a few words about what a particular tax payment system provides. Let's start with UTII. This is a regime in which citizens pay a single tax on imputed income. It is calculated from the estimated income per year. At the same time, neither the costs of the business, nor the real profit of the entrepreneur are taken into account. This system is beneficial for those whose income is significantly higher than the estimated.

In all regions, UTII is different. He is constantly changing. UTII or USN for FE choose? It’s hard to answer. Nevertheless, at UTII a citizen is exempted from the following taxes:

- Personal income tax;

- on the profit of organizations;

- VAT;

- property.

This greatly simplifies life. Thus, you will have to pay only UTII and compulsory insurance premiums. But about them later.

STS - definition

First, we’ll try to figure out what the STS is. This system is called "simplification." UTII in the people is called "imputation".

With a simplified tax system, you can use 1 of several available tax calculation schemes. Namely:

- "Income-expenses". The amount of tax is set in the range from 5 to 15%. It all depends on the region of residence of the entrepreneur and on the activities. The tax base is the amount received after deducting all expenses incurred.

- "Revenue". In this case, 6% tax is calculated. It is charged on the entire annual income of a citizen. Therefore, the exact amount of payment is difficult to name.

In the case of STS, as in the case of UTII, you need to pay only one tax + contributions to extra-budgetary funds. In fact, it can be difficult to choose between STS and UTII.

Conditions for using UTII

"Impute" can be applied not in all areas of entrepreneurship. There are a number of restrictions that sometimes prevent the use of such a tax payment system.

The thing is that UTII can be opened if the organization has no more than 100 employees. In addition, it is important that the share of other companies is no more than 25%.

Also, when using "imputation", the type of company activity is taken into account. This mode can be used in the following areas:

- household and veterinary services;

- vehicle maintenance, washing and repair;

- parking for vehicles;

- transportation of goods and passengers;

- trade (retail) with premises not exceeding 150 m2;

- catering services;

- distribution of advertising using special equipment;

- provision of housing and premises for living (not more than 500 m2);

- temporary transfer to the use of trading places and land.

All other activities do not include the use of "impute". IP on UTII and on the simplified tax system may not be open everywhere. Indeed, in some regions of the Russian Federation, UTII has already been abolished.

Conditions for USN

But there are certain limitations when applying the simplified tax system. There are not many of them. That is why the "simplified" in practice is most often found. Especially when it comes to working for yourself, without employees.

UTII or USN for SP more profitable? There is no definite answer.But consider the "simplification" for a business under the following conditions:

- in the company no more than 100 people;

- the company has no branches;

- the organization receives less than 60 million rubles a year.

The bulk of the types of activities allows you to use STS. Therefore, this mode attracts many entrepreneurs.

Reporting

IP on UTII and on the simplified tax system at the same time occurs in practice quite often. But after 2021 there will be no such scenario. After all, "imputation" is going to be completely canceled by the specified year.

While there is a chance to use both taxation regimes, it is worth paying attention to their features.

The accounting policy of IP (UTII, USN) is quite simple. After all, these modes do not require special paperwork. "Importer" provides for quarterly reporting. Moreover, the declaration shall be submitted no later than the 20th day of the month following the reporting one.

In the case of the simplified tax system, reporting is provided for quarterly, semi-annual, 9 monthly and annual. Minimum paperwork. The declaration is filed no later than April 30 of the year following the reporting year, once a year. It is very convenient.

About taxes

Now a little about how IP on UTII (and on the simplified tax system) pays taxes. Usually this issue is treated very carefully.

"Importer" often provides for quarterly tax payments. Moreover, money is transferred to the Federal Tax Service no later than the 25th day of the month following the reporting period. With the simplified tax system, taxes can be paid both quarterly and once a year. In addition, advance payments are possible.

Simplified requires payment of taxes no later than April 30. This implies the year that followed the reporting year. This is a normal occurrence. That is, in 2016 you will have to pay for 2015 and so on.

Contributions

Contributions to extra-budgetary funds by all SPs are made without fail. So says the current legislation. An individual entrepreneur at UTII and at the simplified tax system transfers fixed amounts of money to the FIU and for medical insurance. Since 2017, such deductions are accepted by the Federal Tax Service.

Contributions are made in both modes:

- for employees;

- for myself.

Moreover, the size of payments depends on the minimum wage. In 2017, you will have to pay a little more than 27,000 rubles for both taxation systems for insurance and as contributions to the FIU. This amount is for 1 employee or "for yourself."

If an individual entrepreneur works with subordinates, he can reduce the amount of tax by 50% of the listed mandatory contributions to extra-budgetary funds. When doing business "on your own," you can reduce the tax by 100% of the contributions made, but not more than the amount of taxes.

Thus, contributions sometimes allow you to get rid of taxes at all. You can list them both quarterly and once a year. IE on UTII and STS insurance premiums are required to pay, as in all other cases.

An additional 1% of income over 300,000 rubles per year must be transferred to the FIU. This percentage is added to the mandatory fixed payments. For example, if a company earned 330,000 rubles a year, then in addition to fixed contributions, it is necessary to transfer 1% of 30,000 rubles to the Pension Fund.

Contribution Contributions

FE contributions when combining STS and UTII require special attention. Indeed, in this case, it will be necessary to clearly distinguish between employees - who will work with what system. Contributions are made for all employees and for each regime separately.

At the same time, tax on deductions made can be reduced only in relation to regime 1. His entrepreneur chooses himself. If an individual entrepreneur works with employees, then the tax can be reduced no more than by 50% of all transfers, otherwise - by 100%.

Nuances of combination

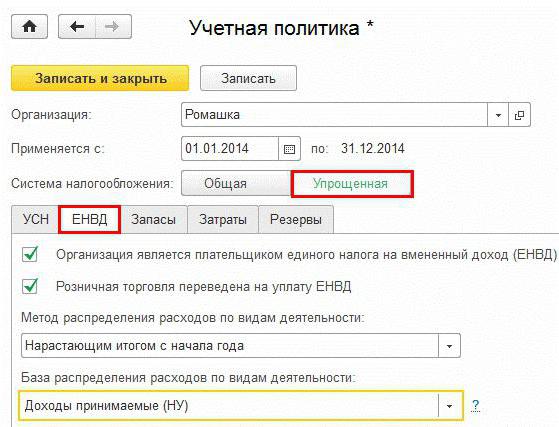

If an individual uses USN and UTII, he may encounter some difficulties. Especially at first.

The thing is that the accounting policy of entrepreneurs under such circumstances provides for a clear distinction between workers and property according to the chosen taxation systems. This means that for the "simplified" and "imputed" it is necessary to keep different reporting.

There are no more conditions for accounting policies.The main thing is that it helps to determine the tax base without errors in a particular case. General expenses for taxation systems are distributed in proportion to income for "imputed" and "simplified", respectively.

One type of activity

It is also worth paying attention to the fact that an individual entrepreneur on UTII and STS (with or without employees) cannot work with several types of taxation if the entrepreneur carries out the same activity. What does it mean?

According to the legislation of the Russian Federation, it is forbidden to use UTII and STS at the same type of business at the same time. Each taxation should have its own scope.

As a rule, the simultaneous use of “imputation” and “simplification” occurs when a citizen first began to work on UTII, and then he began to conduct another activity on STS.

About income and expenses

In Russia, entrepreneurs with USN are exempted from the mandatory use of cash equipment. This makes life much easier. And with "imputation" and "simplification", an entrepreneur is not required to keep a serious record of income and expenses.

Nevertheless, you need to get a document called "book of accounting for expenses and income." In it, as we have said, it is necessary to separately record all income and expenses for a particular type of taxation. This document may be requested by the Federal Tax Service during inspections.

Combining UTII and USN for IP is possible. But, as practice shows, now more and more people prefer only one type of taxation. And given the fact that they want to get rid of the "impute", entrepreneurs have to forget about combining these modes.

How to make a choice

Some are interested in what is better - IP on UTII and on the simplified tax system, on the "imputation" or only on the "simplified". It is definitely impossible to answer. After all, the answer will depend on many factors.

For example, such as:

- type of activity;

- real profit from the business;

- organization expenses;

- number of employees;

- reporting.

Most often, when combining STS and UTII, a "simplified woman" is selected with a 6% tax. This eliminates unnecessary paperwork. Entrepreneurs working without employees often use only the simplified tax system with a 6% tax base. UTII in real life is applied when the real profit significantly exceeds the tax itself. And if in the selected area of activity a chance is provided for the use of "imputation".

With small real incomes, most often at first it is recommended to give preference to STS 6%. If the profit is not high, and there are expenses, you can look at the “simplification” with the income-expense tax calculation scheme.

About transition statements

IP on UTII and on the simplified tax system, as a rule, is not created immediately. But such scenarios are also provided. In this case, the citizen must, at the opening of the IP, apply to the Federal Tax Service for the use of “simplified” and “imputed” at the same time. At the same time, activities within a particular taxation system are clearly delineated.

In general, newly opened companies can apply for the transition to the simplified tax system no more than 30 days after the start of their activities. When changing the tax regime, a notification must be sent no later than December 31 of the year preceding the transition to "simplification".

SP switches to STS with UTII? Then you can apply a new scheme for calculating tax from the month of the end of work with the "impute". But you must first notify the Federal Tax Service of your intentions.

A request for the application of UTII must be submitted no later than 5 days after the opening of the business. If no notifications are given, then the IP starts working with OSNO. And such a tax regime is not always convenient. Especially at low incomes and unwillingness to mess with reports and declarations.

Summary

Now it is clear that provides for the combination of UTII and the simplified tax system for individual entrepreneurs. And how these two modes look separately from each other. Their features, too, from now on will not be a mystery.

Is it always profitable to combine "simplified" and "imputation"? Not. Such a step is beneficial only in certain circumstances. And you can’t say exactly when the combination will be needed.

In real life, USN is becoming an increasingly popular destination among entrepreneurs. Especially for those who work only for themselves. That "simplified" is given greater preference.

FE contributions when combining STS and UTII are paid without fail. In the same way as without combination. It is important to understand that the simultaneous use of several taxation systems requires a clear distinction. Otherwise, combining modes will be prohibited. If an individual entrepreneur combines UTII and the simplified tax system, one must be extremely responsible in reporting.