Many individual entrepreneurs use tax special regimes to simplify reporting and save. Nevertheless, IP on the main taxation system is not uncommon today. Most often, this is a conscious choice, which is dictated by the decision to pay VAT for the convenience of partners. Less commonly, the subject simply has no other option. For example, if it does not meet the criteria for special modes or has exceeded the limits set for them. Next, we will analyze in detail taxes and reports of individual entrepreneurs on OSNO.

FE status features

An entrepreneur as a taxpayer has a dual status. On the one hand, he conducts economic activities, earns income and pays taxes related to this. On the other hand, he is an ordinary individual who also has certain tax obligations. Thus, IP taxes are made up of two parts - personal and entrepreneurial.

The personal taxes of the individual entrepreneur on OSNA, that is, payments not related to his entrepreneurial activity, depend on what he owns. These are the so-called property taxes on individuals. These include:

- transport tax;

- property tax - apartment, house, cottage;

- land tax;

- water tax - per well or well.

The payment of these taxes by the entrepreneur is the same as any physical person. IP does not submit any reports to OSNO on them.

IP taxes in general mode

Being on OSNO, SP pay the following taxes related to business:

- Personal income tax on own income, if available in the reporting period.

- PIT for its employees as a tax agent. Entrepreneurs who do not engage in wage labor are exempt from tax.

- VAT. Paid from the sale of most goods and services, although there are many exceptions.

The kind of reporting that an individual entrepreneur should have to submit and which taxes to pay depends on the specifics of his activity. After all, some taxes are associated with industry specifics. These include excise taxes, mineral extraction tax, water tax in the implementation of industrial water withdrawal, fees for hunting and fishing, and some others.

It must be remembered that taxes and fees are both federal and established at the regional or local level. This means that in individual entities or localities different rates and even their own payments may apply. In particular, Moscow has a trade fee, which is payable, including by entrepreneurs, who fall under its criteria.

Apart from taxes are insurance premiums. And here the dual status of the individual entrepreneur pops up again - as a self-employed person and as an employer. The entrepreneur is obliged to pay contributions - own and for employed persons, as well as submit reports on the latest payments. IP on OSNO without workers pays contributions only for itself - there is no reporting on them.

VAT

In general, sales in Russia are subject to VAT. It is charged by the seller in addition to the cost of the goods (services) and is included in its price. VAT is charged for each transaction and is shown on a separate line in the invoice. This document must be drawn up by the supplier no later than 5 days from the date of shipment of the goods (provision of services) or from the date of receipt of funds - which of these events will occur earlier.

There are currently three VAT rates:

- 18% - base rate;

- 10% - a preferential rate that applies to many food and children's goods, medical products and print periodicals;

- 0% - the rate used for export operations.

The calculated VAT can be reduced by the amount of deductions - the amount of input tax indicated in the invoices received from suppliers. The total amount will be VAT payable. Taking into account some features of the application of deductions, sometimes a negative difference can be obtained that is subject to compensation, that is, return from the budget. However, it should be remembered that in this case an additional check is mandatory, and I can require supporting documents from the entrepreneur.

Submit a VAT return at the end of each quarter. Dates of submission: for the 1st quarter - April 25, for the 2nd - July 25, for the 3rd - October 25 and for the 4th - January 25 of the next year. Reporting of IP to OSNO for VAT is carried out strictly in electronic form.

Personal income tax

IP income tax is paid on the amount making up the difference between income and expenses. In this case, business income and documented expenses (professional deductions) are taken into account. For individual entrepreneurs, the standard personal income tax rate is 13%.

Reporting of individual entrepreneurs on the income tax base begins with filling out form 4-NDFL. It is intended to reflect the expected income of an individual and is served upon its initial receipt. The deadline for submission is no later than 1 month and 5 days from the date of receipt of the first income. Also, this form is submitted if the entrepreneur’s income increases or decreases by more than 50%. Based on the data from 4-NDFL, the inspectorate will calculate advance payments. They are paid in the following order:

- Half of the amount of advance payments is transferred for the first half of the year. Deadline for payment is July 15.

- 1/4 of the amount is paid for July — September and for October — December. Terms of payment - until October 15 and January 15, respectively.

Until April 30, IP submits a report in the form of 3-NDFL for the past year. It serves to calculate tax payable taking into account the actual income received and advance payments. According to the results of the year, personal income tax must be paid no later than July 15. If the advance payments exceeded the amount of tax payable, the overpayment from the budget can be returned.

Personal income tax for employees

If an individual entrepreneur has personnel, then he is obliged to fulfill the role of a tax agent for personal income tax. This means that he must accrue and withhold tax on payments to his employees, and then transfer it to the budget.

The tax base is the employee’s income for the month, reduced by the amount of tax deductions (property, for children, for treatment, for education). It is worth considering that personal income tax is not taxed on all individuals' incomes - some of them are not included in the database. In particular, personal income tax is not subject to compensation, maternity benefits, gifts within 4 thousand rubles and some other types of income.

Personal income tax rate - 13%. It applies to citizens of the Russian Federation. If non-residents are hired, then the rate will be 30%. In general, the tax is transferred to the budget immediately when income is paid or no later than the next day. But there are exceptions. For example, personal income tax on vacation pay and disability benefits, including for children, can be paid no later than the end of the month in which these incomes are paid.

Several forms of reporting are associated with the income tax of employed individuals. SP on OSNO with employees must submit to the IFTS:

- certificate for each employee in the form of 2-personal income tax - for the past year is submitted until April 1;

- calculation of 6-personal income tax - quarterly, during the first month after the end of the reporting quarter;

- information on the number of employees - until January 20 for the previous year.

Insurance premiums for yourself

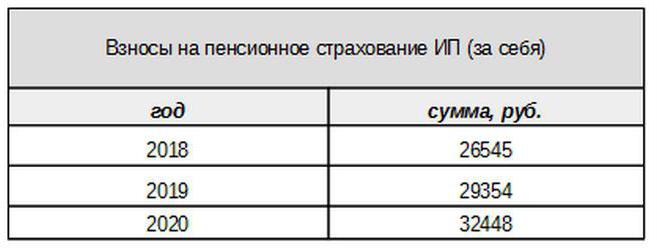

Own contributions for compulsory insurance are paid by the entrepreneur, regardless of whether he received income in the current period or not. The base contribution in 2017 is tied to the minimum wage. However, from next year this link will not be. Individual contributions to the Pension Fund for income from less than 300 thousand rubles are set in the form of a fixed amount:

Incomes over 300 thousand rubles, as before, will be taxed at a rate of 1%.Moreover, the maximum amount of contributions will not exceed 8 times the minimum wage.

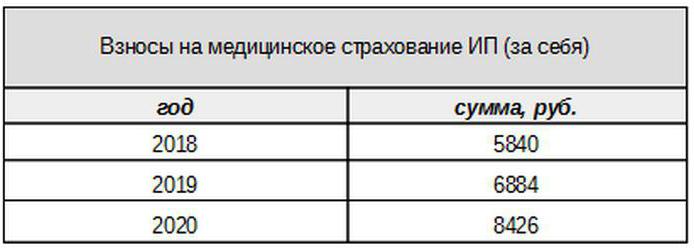

Medical fees will be paid in the following amount:

Contributions for Insured Persons

The entrepreneur must pay insurance premiums from payments to insured persons, that is, his employees, as well as submit several reporting forms. IP on OSNO in this case pays contributions at the following rates:

- on pension insurance - 22%;

- social - 2.9%

- for medical - 5.1%.

These are the basic rates applicable for incomes not exceeding a certain limit. If incomes have exceeded this level, then lower rates will be applied for the calculation (excluding medical fees). In addition, reduced contribution rates exist for certain categories of payers.

IP employers also pay contributions for accident insurance, or as they are also called, for injuries. The rate at which these contributions are calculated depends on the specifics of the entrepreneur and varies from 0.2 to 8.5%. To find out at what rate the individual entrepreneur must pay injuries, he needs to confirm the main activity by submitting the appropriate form to the Social Insurance Fund. This should be done annually no later than April 15th.

What kind of reporting does the IP on OSNO provide for insurance premiums?

The employer must submit several forms for insured persons to the IFTS and funds. For these reports, different submission periods and deadlines are also provided. Reporting IP on OSNO with employees includes:

- Calculation of insurance premiums. Starting in 2017, he replaced the RSV-1 form and is now being submitted not to the FIU, but to the IFTS.

- 4-FSS. Submitted to the Social Insurance Fund once a quarter. The deadline is up to 20 (for the electronic form - up to 25) of the first month of the next quarter.

- SZV-M containing information about the insured. It is submitted to the Pension Fund every month until the 15th day of the next month.

- SZV-HUNDRED - a new form about the experience of employees, which will first need to be submitted to the FIU in 2017. The deadline is until March 1 of next year.

IP on OSNO: zero reporting

It happens that an entrepreneur is registered, but has not started activity or has temporarily suspended it. However, this does not mean that he does not need to submit reports. In this case, for some payments, he must submit a form with zero indicators.

If the entrepreneur does not use hired labor, then in the absence of activity, he submits zero returns for VAT and 3-personal income tax. If there are employees, then the following forms will be added:

- Calculation of insurance premiums (zero);

- 4-FSS form (zero);

- SZV-3 (with data).

Since there were no transactions in the reporting period, including the payment of income to employees, the contributions will also be zero. Therefore, the calculation of insurance premiums and 4-FSS served with zero indicators. At the same time, 6-NDFL and 2-NDFL are not filed - since there were no payments, the IP does not arise as a tax agent. But the SZV-M form, in principle, does not contain indicators that depend on the conduct of activities, therefore it is submitted completed.

About accounting

The reporting rules referred to above relate to tax accounting. As for the financial statements for the year, IP on OSNO, like other entrepreneurs, are exempt from it. They are not required to keep accounting, that is, apply a chart of accounts and make postings.

But this does not mean that IP operations can not be fixed at all. To reflect them, the entrepreneur fills out a book of accounting for income and expenses. In addition, if an individual entrepreneur pays VAT, he is obliged to reflect operations in the purchase book and sales book.

In addition, the IP may have other accounting objects, for example, fixed assets, personnel, cash register operations. All this requires the maintenance of appropriate registers and clearance. And of course, the entrepreneur is in no way exempted from the “primary” - acts, invoices, invoices and other documents.

To summarize

So, reporting IP on OSNO largely depends on whether it has employees. If there are none, then the entrepreneur generally pays VAT, personal income tax and insurance premiums for himself. The main reporting forms are the VAT return and 3-NDFL. If hired labor is used, personal income tax for employees and mandatory contributions for insured persons are added to the above payments. But the list of reporting forms of the employer-employer is much richer.

In addition, you need to know about regional and local features of taxation, as well as about industry payments (excise taxes, mineral extraction tax and others). And do not forget that the entrepreneur remains an ordinary citizen. Therefore, if there are objects of taxation, he is obliged to pay property taxes - real estate, transport, land. They are paid at the notice of the tax authorities and do not require any form.