In accordance with the Tax Code, the obligation of legal entities is the deduction of amounts during the year property tax. Advance payment due date determined by regional law. It should be borne in mind that deductions are made only from real estate. Let us further consider how the transfer is carried out. property tax advance payments. The form Report to the IFTS will also be described in the article.

General rules

Within the meaning of Articles 373 and 374 of the Tax Code, objects recognized as fixed assets in accounting are taxed property tax. Advance Payments it does not carry out organizations using UTII and USN.

In accounting, fixed assets are reflected in accounts 01, 03. The accounting procedure is established by PBU 6/01 and in the Methodological Instructions approved by order of the Ministry of Finance No. 91n of 2003.

Until 2013, organizations paid tax on movable and immovable property. Cancellation of payment is provided for in Article 374 of the Tax Code (Subitem 8 Clause 4).

Features of movable things

If the assets were capitalized as part of OS 01.01.2013 or later, property tax and advance payments on it is not charged. In practice, however, difficulties often arise when classifying objects as movable things.

With vehicles in general, everything is clear. They are uniquely movable objects. But what about the inseparable improvements that the tenant has made? According to the position of officials of the Ministry of Finance, they are recognized as subject to taxation. The relevant explanations are contained in the letter of the Ministry of April 15. 2013. Inseparable improvements are large-scale works on the modernization or reconstruction of structures. Naturally, he will not be able to take such objects with him.

As for air conditioners (not included in the air conditioning system of the building), billboards and other similar elements, they are exempt from taxation, as they are recognized as movable objects. Similarly, linear-cable networks and communication facilities are considered.

With fire and burglar alarms, things are not so simple. Their assignment to movable objects depends on whether they are included in the engineering system of the building. If their movement without significant damage to the building is impossible, then, accordingly, they are recognized as immovable. If they do not belong to the general system, then they are not subject to taxation. Such explanations are contained in the letter of the Ministry of Finance dated 03/27/2013.

Special order

If the company combines UTII and OSSO, property tax and advance payments on it is accrued in relation to the operating system, which are used in general operating activities. If the organization does not want to carry out the reorganization, you can get out of the situation by buying a used object. When registering movable used property, tax is not charged. Moreover, it does not matter the fact that the seller of the object reflected them until 2013 as an operating system. The correctness of this approach is confirmed by the letter of the Ministry of Finance of 02/07/2013.

Calculation of advance payments on property tax

After determining the objects of taxation, as well as the availability of rights to benefits, you can proceed to direct calculations. To calculate down payments on property tax, you need to multiply the base and bid. The result is divided into 4.

Each region sets its own rates. However, they cannot be higher than 2.2%. The corresponding order is contained in article 380 of the Tax Code.

Special rules

According to the law, the property comprising the unit investment fund is taxed by the managing organization. Payment is made, respectively, at the expense of objects included in the investment fund. As a base for calculation of advance payments on property tax advocates its average value for the reporting period.

For example, take six months. Calculation of advance payment of corporate property tax produced by the following formula:

NB = (Ost1 + Ost2 + Ost3 + Ost4 + Ost5 + Ost6 + Ost7) / 7, in which:

- NB - tax base (average number of items);

- Ost1 ... Ost7 - residual value for each month included in the reporting period.

It is quite possible that the asset is completely new. For example, the building was acquired in April. This means that at 01.04 and previous months the residual value will be zero. At 01.05, the initial cost is taken, since it is from this date that depreciation began. However, to determine advance payment of property tax, the base is calculated according to general rules: all indicators are added to the first days of the months, the result is divided by 7.

Example

Take the following source data:

- On the balance sheet of the company is a passenger car.

- On 01.01. 2013, its residual value is 810 thousand rubles.

- In accounting, a linear method of calculating depreciation is used. 30 thousand rubles are written off monthly.

The average cost of an object for the first six months of 2013 will be as follows:

(810 + 780 + 750 + 720 + 690 + 660 + 630) / 7 = 720.

The company is not eligible for benefits. In accordance with the provisions of regional legislation, the rate is 2.2%. Accordingly, aorganization property tax payment is equal to:

720,000 x 2.2% / 4 = 3960.

Specificity of deductions

By virtue of the provisions of paragraph 1 383 of the Tax Code, the timing of advance payments of property tax is determined by regional authorities.

Generally, amounts must be paid within 30 days. from the end date of the reporting period. The deduction is usually carried out at the location of the company, at the details of the inspection in which it is registered. Meanwhile, there are a few special cases.

For example, on the balance sheet of an enterprise is an immovable object located in another territory (in another constituent entity of the Russian Federation). In this case, the amount advance payment of property tax deducted to the budget of the corresponding region (in which the object is registered). Such an order is contained in Article 385 of the Tax Code.

Separate units

For organizations with branches / representative offices, special rules for deductions are also provided. property tax advance payments.

The legislation allows 2 payment options:

- Transfer is carried out in the budget of the region in which the unit is located. In this case, the branch / representative office must have an independent balance sheet.

- Transfer is made at the location of the main office. This option is used when the unit has no independent balance.

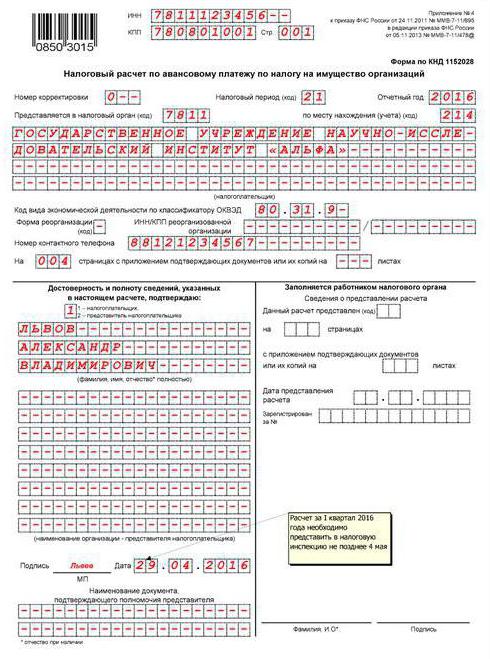

Advance payments for property tax: filling out documentation (general requirements)

The calculation of the amounts is executed, in accordance with Article 379 of the Tax Code, for the 1st quarter, 6 and 9 months. year (calendar).

Values of cost indicators should be indicated in full rubles.

Estimated Pages property tax advance payment form must be numbered starting from sheet 01 (title page).

Correction of errors, including using corrective or other similar means, is not allowed.

Use violet, blue, or black ink when filling.

Double-sided printing of information on sheets, as well as bonding leading to damage, is not allowed.

Features indicating indicators

There is one field for each indicator in the document. It consists of a certain number of familiarities.

Special rules are provided to reflect quantities expressed in decimal or regular fractions.

Indication of the date is carried out in the fields day (2 familiarity), month (2 familiarity), year (4 familiarity). Numbers are separated by a dot.

In the case of filling out a document using software, the values should be aligned according to the last (right) familiarity.

In the absence of any indicator, a dash is inserted (a straight line in the center of the field along its entire length).

OKTMO Code

This is the municipality code.

Under the code allotted 11 familiarity. If the number of digits is less than the specified number, the remaining cells are not filled. They put a dash.

Presentation Features

The settlement document can be sent to the IFTS by post or email. In the first case, the subject makes an inventory of the investment.

In addition, the calculation may be provided personally by the payer or by the representative of the applicant. In this case, the presentation of information on paper with the attachment of their electronic copy is allowed.

If the document is submitted in electronic form, it must be certified with a digital signature in accordance with the procedure approved by the order of the Ministry of Finance of 02.04.2002.

If the date of submission of the Settlement, as well as the payment of the advance payment, falls on a non-working / holiday, the date is postponed to the first working day following it.

When sending a document by mail, the day of sending is considered the date of its submission. Similarly, the period for sending the Settlement in electronic form via telecommunication channels is calculated. In the latter case, after the acceptance of the documentation, the IFTS must provide the payer with a receipt confirming receipt.

Section 1

It is filled in with respect to the amounts payable at the address of the enterprise (the place of registration of the permanent establishment of a foreign company), its separate division, which has its own balance sheet, or the location of the property.

The Section provides the following row information:

- 010 - OKTMO code, according to which the amount given in page 030 is payable.

- 020 - BSC, by which the payment should be credited.

- 030 - the amount of the advance payment at the place of provision of the document.

Index p. 030 is determined by adding the differences of values on lines 180 and 200 of all the second sections of the calculation with OKTMO codes and the differences of the values of pages 090 and 110 of the third sections of the document with OKTMO codes.

Section 1 information must be certified by signature.

Real Estate Acquisition

To resolve the issue of the need to pay tax, it is necessary to assess the condition of the facility.

If the structure is suitable for operation without additional investments, then it is subject to taxation. The building is included in the base for calculating from the 1st day of the month following the one in which the acceptance certificate was signed and it is capitalized.

If the object is unsuitable for use and requires additional investments, the tax is not paid. The calculation will begin after the commissioning of the facility. In addition, it is necessary to form the initial value of the property. It includes the cost of bringing the building to a usable condition.

Leasing or rental

By law, the tenant does not pay tax. This obligation is assigned to the owner.

As for lessees, they are also exempt from tax. However, the company will succeed in saving if the subject of the transaction is on the lessor's balance sheet. Otherwise, the deduction is made by the recipient. In such a situation, the company must reflect the asset in the account. 01.

Transfer of the object for free use

In this case, the lender must pay the tax advances. This is due to the fact that property is not deducted from the balance sheet.

In general cases, the recommendations of officials are as follows. The company, determining the composition of the property, must take into account the provisions of OKOF (All-Russian Classifier of Fixed Assets), approved by the resolution of the Standardization Committee No. 359 of 1994.In addition, the norms of the Federal Law No. 384 should be taken into account.

Important point

Lawyers remind that if certain objects of movable property can be used outside the immovable without causing disproportionate damage, then such things should not be included in the immovable object. This provision is also true for movable assets, the purpose of which is not related to the operation of the structure / building. The relevant conclusions are present in the letters of the Ministry of Finance.

Thus, if, for example, the machine can be moved from one place to another, and it will work properly, there is no need to pay tax and advances on it.

Reorganization

It is considered one of the ways to optimize taxes. Of course, during the reorganization, it is necessary to solve a number of procedural issues, which is associated with certain monetary investments.

Nevertheless, financiers believe that property received by the successor after the reorganization should not be taxed. This position is relevant for any form, including conversion. In other words, to optimize taxes, it is enough to turn an LLC into an AO. As a result, the tax on movable assets received in accordance with the deed of transfer after 2013 is not paid. It is worth saying that a similar conclusion follows from the letters of the Ministry of Finance from 14.05 and 3.04. 2013 year

Privileges

They can be of two types:

- Federal. They are mentioned in article 381 of the Tax Code.

- Regional They, respectively, are established by the authorities of the subjects at their discretion.

There are no difficulties with federal benefits in practice. Separate OS categories or objects of certain types of enterprises are exempted from taxation. For example, property of prosthetic and orthopedic specialized organizations, bar associations, bureaus, legal consultations are not taxed.

Firms whose main activities are related to the production of pharmaceutical products can also take advantage of the benefits. These companies are exempt from tax on property that is used to create immunobiological veterinary products designed to combat epizootics and epidemics.

In general, in all cases specified in Article 381 of the Tax Code, property tax is not paid.

With regional benefits, the situation is somewhat more complicated. For example, take Moscow. Section 4 of Law No. 64 of November 5, 2003 provides for benefits for commercial enterprises. These organizations are exempt from taxation in respect of property used for storage of deicing reagents (in solid and liquid form).

Benefits are also provided for companies that own multi-storey parking garages. Exemption for such business entities is also provided if such facilities are leased.

Conclusion

In general, the provisions of the legislation regarding the calculation and timing of the deduction of advances for property tax are quite transparent. There should not be any difficulties when preparing reporting documents submitted to the supervisory authority, since the Federal Tax Service approved the procedure for filling them out, and explanations to it are given in the letters of the Service.