6-personal income tax is a new type of reporting of tax agents, which covers the general data: about all employees receiving material resources from it, about all accrued and paid amounts of income, about tax deductions provided, about calculated and deducted personal income tax. When filling out the report, some financial specialists had difficulties, so further we will analyze all the nuances of how to fill out 2 section 6 of personal income tax.

For whom new reporting has been instituted

Form 6-NDFL was introduced for individual entrepreneurs and enterprises that are tax agents, that is, those who pay employees and other individuals wages and other accruals stipulated by the legislation of the Russian Federation. In simple words, the 6-NDFL form must be submitted to the tax authority by those who fill out the 2-NDFL form.

The differences between these forms are that 2-personal income tax is done separately for each employee of the company, and 6-personal income tax is formed once a quarter for all employees at once.

Report submission deadlines

Form 6-NDFL for the year is issued several times, or rather, every quarter and is determined by the established time frame:

- 1st quarter - the second day of May;

- 2 quarter - the last day of July;

- 3rd quarter - the last day of October;

- Reporting for the last quarter is submitted simultaneously from 2-NDFL to April 2 of next year.

Features of data display in form 6-NDFL

When entering information into the report, it is necessary to pay attention to the following nuances:

- The amount of calculated NFDL should be calculated and recorded in rounded figures, while amounts less than 50 kopecks are not taken into account, and equal and above 50 kopecks are rounded up to the full ruble. Profit and costs in foreign currency are calculated on the date of actual receipt and expenditure, at the current rate of the Central Bank of the Russian Federation.

- When reporting in paper form, no corrections are allowed, including those made by corrective means.

- Printing of the report should be exclusively one-sided.

- Sheets must be neatly bonded without visible corrections.

- Lines are filled from left to right, in the empty columns the symbol “-” is put.

- A document can only be filled with the following ink colors: black, blue, violet.

What information is contained in section 2 of 6-personal income tax

A new type of reporting contains summary information regarding:

- Citizens to whom the tax agent paid income.

- All payments and charges.

- Deductions made.

- Calculated and withheld income tax.

Section 2, in turn, includes the following data:

- The date when the transfer of funds was actually made, which is the profit of the individual.

- Tax deduction period.

- For how long was the tax transferred.

- The size of the received profit upon.

- The amount of tax withheld.

Most often, at the same time, income is paid to several individuals at the same time, in which case the amounts must be added up, and the total result should be reflected in the report.

You do not know how to fill in the 2nd section of 6-personal income tax accurately? Read more about this later.

How to enter information in the report

In order to correctly enter information into section 2 of form 6-personal income tax, you need to distribute all the profits into two categories:

- According to the actual period of issuance of profit.

- By dates when the deducted tax goes to the state treasury.

From this it follows that each separate period of the actual receipt of funds should be supported by a separate tax amount.But if several receipts came to the company’s account at the same time, for which different terms for the payment of personal income tax were provided, then these amounts must be entered in section 2 separately.

All information entered by the accountant in 6-personal income tax should relate to one reporting phase, that is, over the past 3 months.

Section 2. Lines

Form 6-PIT includes section 2 lines in which the following information must be displayed:

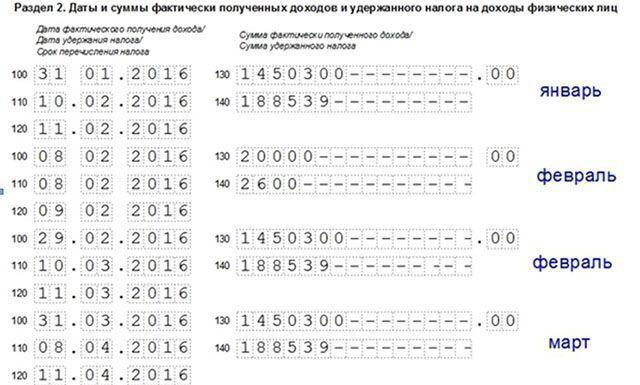

- Paragraph 100 - is intended to reflect the actual date of payment of income. Here, the financial employee contributes information on the payment of wages to employees. The important point is that the payment date in this case is considered the last day of the month when it was carried out.

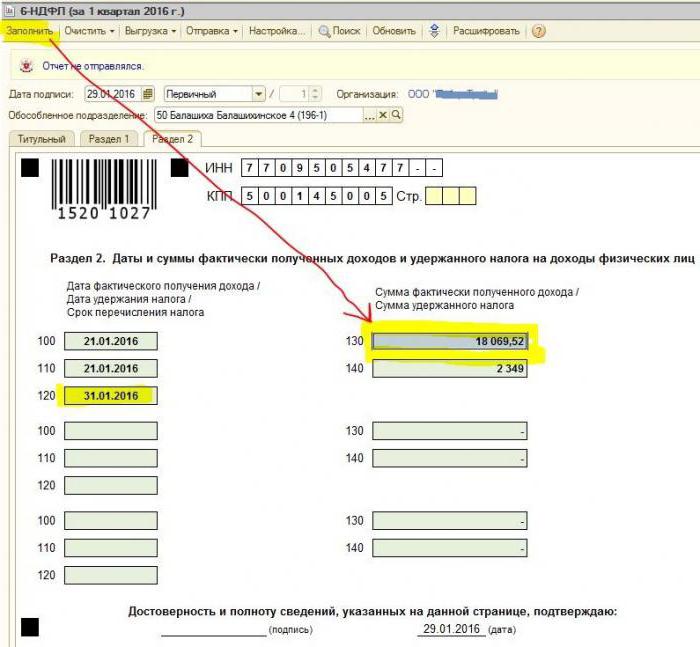

- Paragraph 110 of the form 6-NDFL section 2 - tax deduction. It indicates the date when the funds paid in reality.

- Paragraph 120 - time of transfer of tax funds to the state treasury. As a rule, this day is considered the next date after the payment of wages to employees. And also this line is required to fill in the month of dismissal of the employee.

- Point 130 - the total amount of income is displayed here. For example, line 130 records the sum of the salary paid accrued by the financial employee on a monthly basis.

- 6-NDFL section 2, line 140 - this paragraph indicates the result of tax withheld for the quarter.

Important! In the case when different types of income were received at one time, but at the same time the numbers of their personal income tax transfers differ, then paragraphs 100–140 must be filled out separately for each transfer period.

Sometimes it happens that wages are paid not on the last day of the month, but in part. How to fill out 2 section 6-personal income tax in this case? Such payments are carried out as advance payments; accordingly, the deduction of personal income tax can be reflected only when the following material payments are made. Thus, the first 3 lines in the section should be arranged as follows:

- Point 100 is the last day of the month on which the employee is paid salary.

- Clause 110 of the form 6-NDFL section 2 - the date of the advance payment.

- Paragraph 120 - indicates the number that follows the day of advance payment.

Line 080, what is it for?

Quite often, the accountant in the process of filling out the report is faced with the final indicators of personal income tax, which cannot be calculated within a year. It is these figures that must be recorded in paragraph 080. These indicators should be summarized before the beginning of March of the next reporting year.

As mentioned above, the reporting of 6-personal income tax for the year is required to be submitted 4 times, that is, once a quarter. In the event that all the information does not fit on one page, then it is allowed to add more sheets. The final page of the report indicates the final indicators.

The rules for filling out Form 6-NDFL stipulate that all data in the report should be reflected correctly, without violating legal requirements. In order to make sure that there are no errors, the accountant is recommended to use special verification ratios that will help in the following:

- Independently and without unnecessary efforts to check the accuracy of the data specified in the report.

- Understand what questions may arise from controlling persons in the process of checking the report if they reveal certain inaccuracies.

- Anticipate what actions will follow from the reviewers in the event of an error.

Important! Income of an individual received in the form of a gift or material assistance in section 2 of 6-personal income tax for the tax period is not taxed.

How to reflect vacation payload in section 2 of the report

This section records all vacation pay amounts that were paid for the quarter.

You do not know how to fill out the 2nd section of 6-personal income tax and how many blocks need to be filled? According to the rules, it is required to reflect in the report the same number of blocks as the number of days during which three days vacation pay was paid.If employees were given funds not on the same day, but scattered, then the blocks for each need to be done different. In the case of paying vacation pay to several employees on the same day, the amounts are added up, the final result is reflected in the block.

If there is not enough space on one page of 6-NDFL 2 sections (vacation), then it is necessary to fill in as many sheets as needed. The main thing is to number them correctly, without forgetting about the title page.

- Lines 100 and 110 - to indicate the number when the employee paid vacation pay.

- Line 120 is the last day of the month in which the action was performed.

- Lines 130 and 140 of section 2 of 6-personal income tax - vacation pay (exact amount) and tax deducted from it.

If vacation pay was paid simultaneously with wages, then these amounts still need to be divided into several blocks, because these types of income have a different personal income transfer period (wages are transferred the next day after the actual payment, and deduction on vacation - on the last day of the month).

As in section 2 of the form 6-personal income tax is displayed sick

In accordance with the legislation of the Russian Federation, only temporary disability benefits are taxed, including caring for a sick child. In this regard, in the report of 6-NDFL of section 2, hospital certificates are recorded only of this kind.

The rules for entering data on payments on a temporary disability certificate are the same as holiday pay. That is, these amounts are reflected separately from wages, because the term for transferring to the budget differs from them.

For example, funds paid on temporary disability certificates in the 2nd quarter in section 2 of 6-personal income tax will be displayed in a separate block:

- Line 100 and 110 - the number of payments to the employee accrued funds on the sheet of temporary disability.

- Line 120 is the final day of the month in which the payment was made.

- Lines 130 and 140 - the size of the sick leave payment and the amount of personal income tax deducted from it.

How the report shows the dismissal

The dismissal of an employee is displayed in the report as follows:

- Line 100 - upon dismissal of an employee, the actual date of receipt of a calculation under the law shall be considered his last working day for which wages were accrued. In addition, this should include the amount of compensation for unused vacation, payments on sheets of temporary disability (if any) and vacation payments. The date of calculation is the day of receipt of income.

- Line 110 - PIT is deducted during the actual payment of funds.

- Line 120 - For wages and compensation for unused vacation, the last day of the transfer of personal income tax is the next number after the calculation. For sick leave and vacation pay - this is the last day of the month in which the payment was made.

How dividends are displayed in section 2 of 6-personal income tax

Since the information in Section 2 is compiled on a quarterly basis, the report does not require information from the beginning of the year. So, the data on the form 6-NDFL section 2 on dividends are reflected as follows:

- Clause 100 - Date of transfer of dividends or their issue in property form.

- Paragraph 110 - the day of calculation and withholding of personal income tax coincide. In the absence of the ability to withhold personal income tax, a date with zero indicators is displayed.

- Clause 120 - the date of tax transfer is considered to be the day following the calculation or indicating zero indicators in line 110. If it falls on a weekend, then the next first working day should be indicated.

- Item 130 - amount of dividends.

- Paragraph 140 - Withholding tax.

In a situation where there is no cash on the organization’s account, the payment of dividends may be made in cash. In the report, the date of issue shows the day when the transfer of assets was actually made. It is important that the right to receive dividends in the form of property of the organization was recorded in the constituent documentation.

The value expression of the transferred property must be consistent with market valuation. When displaying information in paragraph 140 of the report, a digital indicator will be absent, “0” is indicated.

Common Mistakes in Reflecting Dividends

When an accountant makes dividend data in a 6-personal income tax report, the following errors often arise:

- The second section of the report 6-personal income tax is filled only at the time of transfer of personal income tax. In further reports of the year, this information is not taken into account.

- The information in section 2 is displayed on the day that personal income tax is held on the last day of the quarter.

- Making amounts that are not dividends. Information about transfers accrued disproportionately to the shares of participants, in case of inferior contributions to the authorized capital, liquidation of the organization within the limits of the share of the contribution and other cases established by law, is not displayed.

- Inclusion in the list of recipients of persons who do not have the right to receive dividends. For example, those who were not included in the number of shareholders at the time of the adoption of the payment order.

In the process of making settlements, difficulties arise in setting the date of actual payment. Remember that the settlement day is determined by the time period for displaying information in the reporting form.

Reporting Procedure

Form 6-NDFL is submitted to the tax service in two ways:

- In paper form. The report can be filled in by hand or using software.

- In electronic format. This option is only possible with a qualified digital signature.

Important! A paper report can only be submitted if the number of employees in the organization does not exceed the number of 25 people. In other cases, the reporting of 6-personal income tax, certificates of 2-personal income tax, reports about the impossibility of holding personal income tax are filed exclusively in electronic form.

Where does the reporting go

Reporting is submitted for verification to different authorities, depending on the form of taxation:

- If USN and UTII are used, then form 6-NDFL must be submitted to the tax office at the place of residence.

- When UTII reporting is filed at the place of registration as a payer UTII.

The date of submission of the report is recognized:

- The day of actual adoption - if form 6-NDFL is submitted first-hand or by a tax agent representative.

- Sending day - when sending a document through the Russian Post with a description of the attachment.

- The day of sending recorded by the system when sending the report electronically on the Internet.

Penalty for failure to report

If form 6-NDFL has not been submitted within the prescribed period, a fine of 1 thousand rubles is charged for one month of delay. However, this should not be delayed, because if the company does not provide the calculation even longer and does not submit the documents 10 working days after the completion of the delivery period, the tax authorities have the right to block the organization’s accounts. Perhaps this is a good argument to submit a report on time.