Standard tax deductions can apply to many employees. However, not every employee knows about this. By the way, the personnel department or accounting department is not obliged to inform the applicants about it, as the provision of documents is the right of the employee, and not his duty. Deduction codes 126 and 127 are most common, as they relate to the first and second child.

general information

Tax deduction is a kind of privilege for an employee. It is noteworthy that there are several types. The most popular are personal deductions for children.

The former include small amounts that are not taxed and for which war veterans, as well as persons with disabilities of the first and second groups, are entitled.

The second large group includes those amounts that are not taxed at the rate of thirteen percent due to the fact that the employee has children. Here, the classification is quite large-scale, since everything affects the deduction code, from the presence of the second parent to the child’s account.

How can I calculate my tax?

If the employee himself wants to check his tax, then he must know how to calculate it correctly. In the general case, the entire amount of his salary is multiplied by thirteen percent or by 0.13.

However, if an employee has the right to a tax deduction and has provided a full package of documents, then he should not tax the entire amount of his salary, but only part of it.

The deduction code 126 and 127 suggests, for example, that an employee who has a first or second minor child has the right to a deduction in the amount of 1,400 rubles. If there are two children, then the amount doubles. However, it is necessary to bring all documents to the children on time. Otherwise, you will have to return the lost amounts through the tax authorities and only for a certain period.

A practical example. Tax calculation

An employee, Ivanova I.I., presented documents for her children. Deduction codes 126 and 127 are applied to her, that is, on the first and second child, respectively. If the total amount of Ivanova I.I. earnings per month amounted to 10,000 rubles, then without an exemption she had to pay the state 1,300 rubles.

But, since the employee has the right to standard tax deductions of code 126, 127, then from her salary when calculating the tax, one can safely subtract 1400 and 1400 rubles. Total, the amount of 7200 rubles is taxed. The amount of tax transferred to the budget is 936 rubles. This means that the privilege of Ivanova I. I. saved her 364 rubles.

Deduction code 126: what is it?

Tax deduction with code 126 denotes a personal income tax benefit for the first child. It is noteworthy that not only one whose child has not reached the age of eighteen can use it. When providing a certificate from an educational institution confirming that the child is studying full-time, the benefit continues to be valid until the child reaches the age of twenty-four.

It is also worth noting that this deduction code has been used since the end of 2016. Earlier, code 114 corresponded to it, which also applied to the first child under the age of majority or receiving education, but only in full-time education.

The amount of the deduction code 126 is 1,400 rubles. This means that it is this part of the employee’s wages that is not taxed. That is, a monthly savings of 182 rubles.

Also, one should not forget that the deduction ceases to apply if the amount of wages for a calendar year has reached 350,000 rubles. In the month in which this amount was collected, deduction codes 126 and 127 will not apply.

If a child was born: we carry documents

If an employee who works at the enterprise has a child, he can immediately bring the whole package of documents to provide a standard deduction of code 126 and 127, and any other.It all depends on what kind of child appeared in the family.

This requires only two documents: a personal statement and a copy of the birth certificate of the child. However, nuances are possible. If the parent brings up the child alone, he also needs to provide documents that confirm this.

These include a certificate for single mothers in the form of number 25, a certificate of death of the second parent, a certificate stating that he was missing. It is also worth bringing a copy of the passport, which states that after the death of the spouse or the status of a single mother, the parent did not marry. This is necessary so that accounting knows which codes to use. The personal income tax deduction code 126 and 127 applies only to those who raise a child in a full family. For a single parent, these amounts will be doubled.

It is also worth paying attention to the change of surname. This is especially true for women. If the maiden name is inscribed in the birth certificate, and now the employee has other data, then it is also worth bringing a document confirming this. In this case, it will be a certificate of marriage.

The personal statement should indicate your data in which department the employee works, as well as the data of the child, starting with the last name, first name and patronymic and ending with the date of birth. It is also worth putting a signature and the date of writing the application.

Pulling the provision of documents is not worth it, because even if the baby appeared on the 29th, the deduction will be provided for the entire month worked. This should be taken into account by accountants. A tax deduction for a child is provided from the month he was born, subject to the timely provision of documents.

New place of work. What do you need?

If an employee has come to a new place of work and wants to receive a tax deduction, then in addition to the documents listed above, he needs to provide a certificate in the form of 2-NDFL. This is necessary so that the accountant can enter information about the employee's salary from the beginning of the year. This allows you to prevent the deduction from reaching the threshold of 350 000 rubles.

Also, if an employee takes a new position in the same month in which he was dismissed from another organization, the accountant can check whether deductions for this month have already been accrued to him.

The deduction code 126 and 127 in the certificate 2-NDFL can be seen directly under the column with the employee's income. Dividing the sum of each of them by 1400, you can find out how many months the deduction was provided. If an employee has already received his benefit for the given month, then the employer sets deductions only from the next month. If there was a break between places of work, then a refund for this period is not provided.

It is noteworthy that if an employee managed to change several jobs in a year, he will have to take certificates from each of them. Even if it was worked there for several days. The income must be summarized and entered into the base in order to correctly calculate taxes.

Otherwise, for those who want to use the tax deduction code 126 and 127, you need to bring a copy of the birth certificates of children, as well as a personal statement. It is also worth bringing certificates from places of study if the child is over eighteen years old.

Code 127. Features

The deduction code number 127 indicates a benefit for those who have a second child. Provide it to those who transmit a package of documents. The amount of deduction in this case coincides with the amount of benefits for the first child and amounts to 1400 rubles.

This means that every month an employee who is entitled to a benefit saves 182 rubles. The limit for using this deduction is the same as for the first child, namely 350,000 rubles.

Until the end of 2016, the designation number 115 corresponded to this code; it had all the same parameters. This code is also used by those parents whose second child has reached the age of majority, but has not yet reached the age of twenty-four and is still studying full-time.

Documents for deduction. Code 127

Tax deduction codes 126 and 127 are similar, therefore they have a similar set of documents.However, for the latter, it will be somewhat wider.

If the employee has two children under eighteen or full-time students, he must provide the following documents:

- Personal statement. In one, you can enter both children at once.

- Birth certificate of both children, as well as copies thereof. It is worth noting that even if the child already has a passport, it is the certificate that is provided, since it is in this document that there is information about the parents.

- Certificate in the form 2-NDFL, if the employee gets a job.

It is also worth noting that if the first child no longer fits the category of persons for whom the deduction is granted, then you still need to bring a certificate for him. This confirms the fact that the child on whom code 127 is used is the second.

What if an employee did not receive a benefit?

It happens that the employee did not know that he was entitled to any personal income tax benefit. Probably, he was either not informed about this or did not provide timely documents. In this case, he can return the amount that he has paid excessively to the tax authorities.

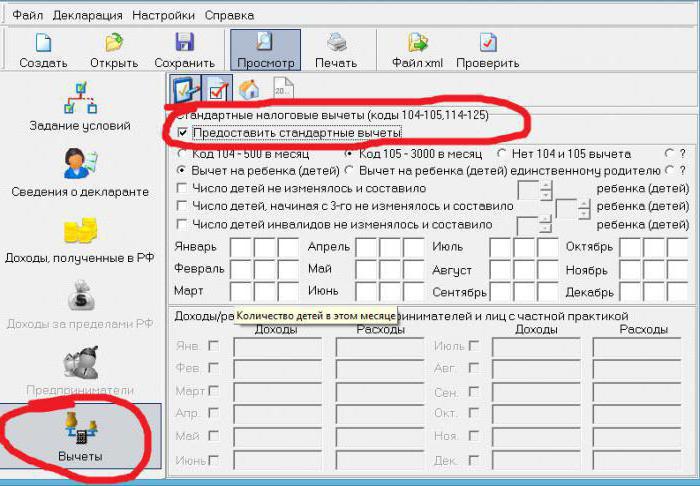

For this, it is necessary to provide a package of documents to the tax service. The deduction code 126 and 127 in the 3-NDFL declaration will also have to be indicated if it is under this value that the appropriate deductions pass.

It is also necessary to take a certificate from the place of work in the form 2-NDFL, as well as copies of the birth certificates of children, if necessary, and a certificate from their place of study. It is worth remembering that you can return the amount only for the last three years. That is, in 2017, you can get money for 2014, 2015, 2016.

The deduction codes 126 and 127 in the declaration will sit automatically if you specify them in a specific tab in the program provided by the Tax Service website. If the return is carried out in a few years, then there will have to be several declarations, separately for each year.