Single imputed income tax is a tax payment regime that can only be used in certain types of activities, such as, for example, trading or providing services to the public.

Distinctive features

The main feature of the regime is that the amount of income received does not matter when determining the tax base. The calculation is made on the size of the estimated income, which is determined at the state level. Hence the vernacular name "imputed". In other words, state bodies establish or rather impute the size of profit.

The tax system does not imply the following taxes:

- on income of individuals;

- VAT;

- property tax.

Liquidation

The definition of liquidation of IP is the termination of registration of an individual as an entrepreneur. As soon as a person goes through the whole procedure and receives written confirmation of removal from the registry, he immediately loses all the rights and obligations that he had while carrying out his activities. Naturally, there is a limitation. If debts remain, then an individual, not having the status of an entrepreneur, must pay off them.

In addition to the desire of an individual, the liquidation of IP on UTII can be carried out in the following cases:

- bankruptcy;

- expiration of registration documents allowing legally to be in the country;

- adjudication by a court;

- death of an individual.

In principle, all the described methods can be attributed to coercive measures, not counting the bankruptcy procedure that was initiated by the individual himself.

Voluntary liquidation

Before starting the voluntary procedure for the elimination of IP at UTII, a number of preparatory measures are necessary.

First of all, it is necessary to find out to which territorial tax authority it is necessary to submit documents, to clarify the amount of the state duty to be paid, as well as the details for making the payment. You can get this information on the website of the Federal Tax Service or by contacting the service in person. In 2017, the duty is 260 rubles.

Filling out the application

Before submitting documents, you must fill out an application in the approved form P26001. The form can be taken at the territorial office of the Federal Tax Service or downloaded from the official website.

The application can be filled out on a computer or manually. If the second option is chosen, then it is better to use a pen with black paste, and write all the letters in capital letters.

Font when filling out a document on a computer, you must select Courier New with a height of 18 pins.

In the upper part of the document are filled in columns with information about the name and OGRNIP of an individual entrepreneur. Then, the method by which the application will be transmitted, contact details, up to e-mail, is indicated.

closing date

The date of liquidation of the IP on UTII is considered to be that affixed to the document issued by the tax service after the submission of the application (form P65001). While there will be no documentary evidence on hand, one cannot assume that the IP is closed. In light of this, 5 days after submitting the application, it is recommended to contact the body to which documents were submitted for obtaining a certificate.

Reporting

In addition to the above measures, it is necessary to complete the UTII upon liquidation of the IP, to submit reports, even for an incomplete period.

When paying tax on imputed income, statements are submitted before the 20th day of the month following the reporting quarter.Therefore, if the certificate was received in March of the current year, then it is necessary to report until April 20. In cases where the 20th day falls on a public holiday or a day off, you can transfer the paper on the next business day.

General rules for filling out a report

All data is entered from right to left. If any cells do not fill out, be sure to put dashes in them. All indicators that are not integer-valued must be rounded off as a general rule. The following requirements should also be followed:

- if the report is filled in manually, then all letters must be in capital letters;

- the color of the pen should be black or blue;

- absolutely all pages of the declaration should be numbered in the format 001, 002 and so on;

- the first page of the report should contain the date of completion and the signature of the compiler, that is, the IP;

- the exact code of the tax period for the liquidation of IP on UTII;

- if there is a print on the cover page, a print is placed on it.

The declaration cannot be stapled and printed on both sides on one sheet. In no case should the report contain corrections or blots. The declaration does not indicate the accrued penalties and interest.

The rest of the reporting is no different from other cases of filling out such documents.

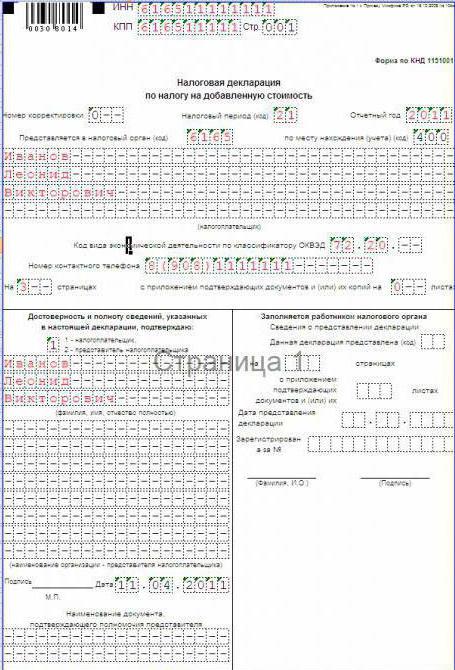

Title page

In the field under the name "TIN" the number is indicated, which is indicated in the certificate or in the extract from the register. The code consists of 10 digits. The form is designed to be completed by legal entities and individuals. Therefore, PI in the last two cells puts dashes.

Individual entrepreneurs do not fill out the field with the name “KPP”.

Depending on the period of work of an individual as an entrepreneur, the data is entered in the line “Adjustment number”. If the report is being compiled for the first time, then 0 is put, if the report is submitted for the second quarter of work, then 1 is put down and so on.

The next column is “Tax period”, that is, the column confirming the period for which the report is submitted. As mentioned earlier, when liquidating an IP on UTII, the code of the tax period is very important.

Then comes the item “Reporting period”, where the period for which the report is submitted is specified.

In the "Submitted to the tax authority" field, the tax authority code is indicated. In the column "At the place of registration" displays the code of the place where the declaration is submitted.

The report indicates personal data of the taxpayer, full name. Then codes are written that correspond to the classifier of OKVED and are registered in the charter documentation, that is, for individual entrepreneurs they are indicated in the extract from the register of registration of legal entities and individuals. If the activity is carried out in several directions, then the type of activity where the maximum income is indicated is indicated.

Then the data is entered in the line “Form of reorganization”. The block is subject to filling only in case of liquidation or reorganization. In other cases, dashes are put down.

In the field "Contact phone number" is a number by which you can contact the submitter of the declaration.

In the block “On pages” the number of attached pages in the format “000 ...” is prescribed.

The column “Power of attorney and completeness of information” follows. If the declaration is submitted by proxy from an authorized person, then code 2 is affixed. If the report was filled in by the IP, then 1.

Place of declaration

The UTII declaration during the liquidation of individual entrepreneurs is filed at the actual place where the business is carried out. If it is impossible to clearly define it, for example, an individual entrepreneur provides motor transportation services or carries out portable trading, then the documents are submitted at the place of registration of the individual.

In cases where there are several points of doing business, and all of them are located in one locality, only one declaration is submitted, but with summary indicators for all points, information about which is displayed in the second section.If the activity is the same, but the points are located in different territorial units, then each tax service will have to submit a separate report, the second section of the report is not filled out, but the indicators are simply summed up.

Declaration Methods

When liquidating an IP on UTII, there are no reporting features.

The first method is a paper version, which is submitted in 2 copies. On the second, the tax office must put a mark on receipt.

The second way is through the post office. It is desirable to issue a letter registered. It is recommended that documents be sent with a notification, which after receipt of the tax service should be returned to the sender. Do not forget that there is a time limit for shipping, which must be taken into account. Therefore, the declaration should be sent in advance.

The third way is through the Internet. For this method, you will have to notarize your signature. If this was done earlier, then there will be no problems with the delivery of the report.

Filling out a declaration

It is very important to correctly indicate the code of the tax period during the liquidation of IP on UTII. It is he who makes it possible for the specialists of the Federal Tax Service to understand that the business is closing.

In general, tax period codes are a two-digit number:

- 22 corresponds to the 1st quarter;

- 23 - 2 quarter and so on.

If it is a matter of closure, then the code for eliminating IP in the UTII declaration is different:

51 | Reorganization or liquidation of individual entrepreneurs in the 1st quarter |

54 | Reorganization or liquidation of individual entrepreneurs in the 2nd quarter |

55 | Reorganization or liquidation of individual entrepreneurs in the 3rd quarter |

56 | Reorganization or liquidation of individual entrepreneurs in the 4th quarter |

In addition to the code of the tax period when closing the IP, you must specify the code of the reorganization form, that is, give clarification. The liquidation code is 0.

Zero Declaration

Many businessmen are interested in the question of whether it is possible to file a UTII declaration when closing an IP with a liquidation code and a zero result. No, you can’t do that. Do not forget that the amount of imputed tax is calculated by the state and in no way depends on the income that the entrepreneur actually received during the reporting period. Therefore, even if there was no profit, you have to pay tax. Even if the entrepreneur has really justifiable factors, there was a fire or robbed the store, you can not submit a zero declaration. Simply put, the point of view of regulatory authorities is only one: do business - pay tax, do not conduct - deregister.

Penalties

Even with the liquidation of IPs, one should not forget that penalties are provided for failure to report.

Violation | Size of sanctions |

In case of untimely submission of reports but payment of UTII | 1 thousand rubles |

In the absence of a report and tax evasion | 5% of the amount of tax, and for each month of delay, even if it is incomplete. Penalties are charged from the moment that is set for the submission of the report, but cannot exceed 30% and cannot be less than 1 thousand rubles. |

What to do after elimination

Any individual must remember that even after the closure of the IP, a person is not exempted from paying all taxes, insurance premiums and debt obligations that appeared during the course of doing business.

If the IP had a seal, then it is not subject to mandatory destruction. After all, it can be used when opening a new IP. And you can open a new enterprise the day after closing. Documents that were generated during the activities of the IP should be stored for 4 years.