For various reasons, many people require borrowed funds for various purposes. Making loans at banks or pawnshops has numerous drawbacks, the most significant drawback being high overpayments. Therefore, people are interested in the possibility of obtaining loans without overpayments. In this case, the employer may issue an interest-free loan to the employee. Under such conditions, you can get the right amount of funds in a short period of time. No interest or tough conditions are required.

General concepts

If you plan to borrow a certain amount from your employer, you must comply with some requirements and take into account the nuances. These include:

- an interest-free loan agreement is drawn up for the employee of the organization, on the basis of which a certain amount of funds is transferred to him;

- the borrower must return the money in a timely manner;

- registration of such a loan is legal, therefore, in no way contradicts modern legislation;

- the agreement takes legal force only after it is signed by both parties;

- the contract is drawn up exclusively in writing;

- company employees who need funds to buy a home can get a loan from the company, and the funds are allocated from the company's net profit after taxes.

Most often, such loans are offered to EMERCOM employees as encouragement and support. Another purpose of giving money is the ability to retain valuable employees.

Interest free loan concept

An interest-free loan to an employee is represented by the issuance of a certain amount of money for various purposes without the need for the employee to pay interest on the use of borrowed funds. The features of such lending include:

- the employer may set low interest rates that do not exceed inflation;

- all conditions must be agreed upon by two participants in advance;

- not only funds can be transferred for use, but also property belonging to the company;

- according to the law, the size of the loan cannot exceed 50 times the minimum wage;

- it is not allowed to use the funds received for commercial purposes;

- the employee can return the funds in parts or in full;

- it is allowed to repay a loan ahead of schedule;

- the recipient will have to pay taxes on the money received.

The company does not have to pay taxes on the funds returned by the employee, as the company does not have interest income.

How are money issued?

An interest-free loan to an LLC employee can be provided in two ways:

- cash withdrawal from organization cash desk;

- transferring money to a bank account.

If a company transfers salaries to specialists on cards, then usually loans are issued in non-cash form.

Legislative regulation

The procedure for concluding a transaction, on the basis of which an interest-free loan is issued to an employee, is regulated by the provisions of Sec. 42 GK. Additionally, the norms and requirements of the Tax Code are taken into account. Since the loan is interest-free, you should take into account the information available in Art. 809 Civil Code.

The legislation does not contain any prohibitions on issuing interest-free loans by companies. It is only important that this process be correctly recorded in the financial statements. In addition, you must correctly draw up the contract and clearly indicate in it that the company does not receive profit in the form of interest. In this case, the company is exempted from taxation of an interest-free loan.The employee also needs to pay personal income tax.

If the funds are used to purchase residential real estate, then a citizen can receive a property deduction at the Federal Tax Service or at the place of employment. Based on Art. 807 ГК the company can provide employees not only cash loans, but also commodity loans. According to Art. 812 of the Civil Code, the contract can be challenged by a specialist if there is evidence that he did not receive the amount of funds agreed upon by the agreement, therefore under such conditions the document is invalid.

What conditions must be observed?

Initially, you should decide whether the organization can issue an interest-free loan to an employee. The procedure can be implemented if certain conditions are met:

- funds or goods received must be used by the employee for any purpose;

- it is required to return the money in the specified amount in a predetermined time;

- if a tangible item is provided, then it must be returned in its previous condition;

- the employer cannot demand any interest from employees;

- the procedure for transferring money is fixed by drawing up a written contract and a receipt;

- if money is issued for specific purposes, then it is not allowed to send them to other purposes, as this is a violation of the terms of the agreement.

The main terms of the contract are agreed between the two parties to the transaction, therefore they can make their own adjustments to this agreement, which should not contradict the requirements of the law.

How is a loan arranged?

The provision of an interest-free loan to an employee is carried out through the implementation of successive stages. To do this, the rules are taken into account:

- initially, the employee draws up a special application addressed to the head of the company, where he asks for a certain amount;

- indicates the reasons for which you need to apply for a loan at work;

- the exact amount of money to be received from the employer is given;

- if the management makes a positive decision, then the main terms of the agreement are preliminary agreed;

- Further, the employee prepares the necessary papers for the loan;

- an agreement is formed directly, where personal information about the borrower and data on the company providing him with funds are necessarily entered;

- The agreement is signed by the head of the company or a responsible person with the appropriate authority;

- at the end is the corporate seal of the organization.

The procedure is considered quite simple, but the management of the company should be aimed at providing such loans to its employees.

For what purposes are funds issued?

The organization issues an interest-free loan to an employee for specific purposes, which are prescribed in a statement drawn up by a specialist addressed to the head of the company. Most often money is sent for the following purposes:

- acquisition of real estate or car;

- Holidays at sea or abroad;

- treatment of various diseases;

- studying at a university.

Often, the contract directly indicates for what purpose the funds will be directed. In this case, the issuance of an interest-free loan, which is the target. Money under such conditions should be directed exclusively to the purposes specified in the application. If the employer receives information that the funds were spent on other needs, this may become the basis for early termination of the contract, so management will require a refund from the employee.

How is the application compiled?

Before drawing up an interest-free loan agreement, an employee needs to write an application addressed to the head of the company. When forming this document, the following rules are taken into account:

- a document is drawn up on a blank sheet of A4 format;

- the name and position of the director are indicated in the upper right corner;

- Further, the name and position of the employee of the company compiling this document are prescribed;

- in the middle the name of the document submitted by the application is indicated;

- in the main part, a direct request is written in obtaining funds from the company on loan;

- the specific amount required by the citizen is given;

- the goals for which the money will be spent are listed;

- indicates the period for which it is advisable to draw up an agreement;

- the conditions on which the money will be returned are given, for example, whether the full amount will be paid to the employer at the end of the term or if partially the funds will be transferred monthly;

- at the end of the document is the date of the application, as well as the signature of the citizen.

It is most convenient to use the scheme, on the basis of which each month the employer independently takes some of the funds allocated to pay off the debt from the employee’s salary. In this case, the employee will not face a serious credit load. A correctly prepared application is registered in the company’s office, after which the employee should only wait for the decision of the enterprise management.

Rules for drawing up a contract

If the head of the company makes a positive decision upon application, an interest-free loan agreement is drawn up for the employee. For this, a form specially developed by the company can be used. A distinctive feature of this document is the absence of interest accrual.

Be sure to enter information into this agreement:

- Subject of the agreement represented by the transfer of funds from the employer to the employee;

- purpose for which this loan is issued;

- duration of the agreement;

- rights and obligations arising from each party involved in the transaction;

- responsibility of the parties;

- grounds for termination of the contract before its expiration;

- rules on the basis of which disputes arising between the borrower and the employer are resolved;

- force majeure situations that may affect the cooperation of the two parties.

Information on the borrower submitted by the place of work, position held, passport data, place of residence and contact information is required to be registered. Information about the company is also entered, therefore its name, legal address, as well as other important details, are indicated.

If the object of the loan is not cash, but some property of the organization, then an act of acceptance of the transfer of values is additionally formed. Often, a payment schedule is drawn up containing information on which days the borrower should return the funds of the company.

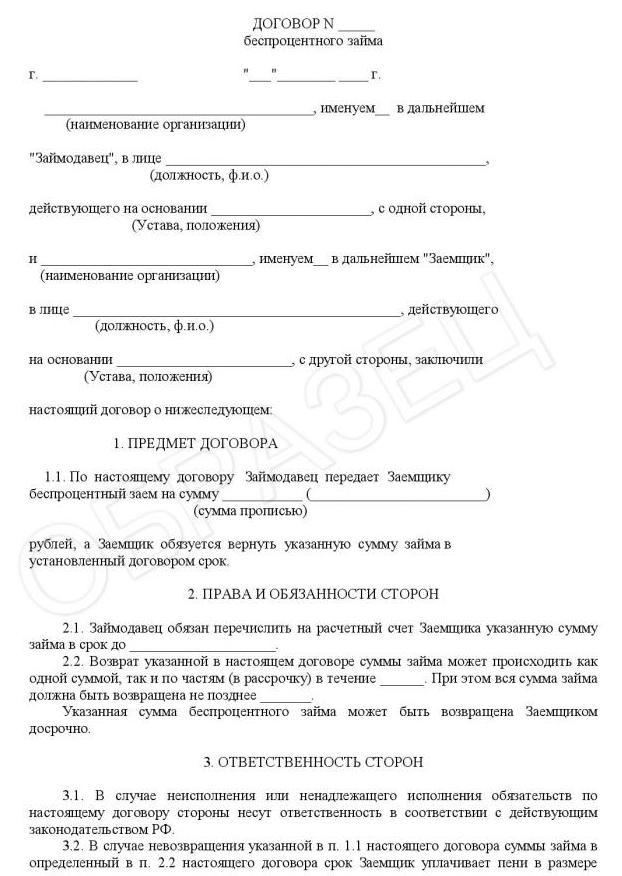

Particular attention is paid to the fines that the borrower will have to pay if he violates the important terms of the contract for various reasons. Usually they depend on the size of the loan and are calculated on the basis of the Central Bank refinancing rate. An example of an interest-free loan agreement with an employee can be found below.

Reflection in accounting

When issuing loans, employees are required to correctly reflect this procedure in accounting. Therefore, you must use the interest-free loan to the posting employee corresponding to this transaction. These include:

- D73.1 K50 - giving money to an employee on the basis of a loan agreement;

- D73.1 K 91.1 - accrual of interest, which should not be higher than the refinancing rate, since otherwise the loan will not be interest-free;

- D50 or D51 K73.1 - repayment of the loan.

If a company actually provides a loan, then this indicates that the employee is responsible and serious. If the posting is incorrectly reflected on an interest-free loan to an employee, then this may become the basis for problems with the tax authorities. Therefore, even under an interest-free agreement, it may be necessary to pay taxes by the company.

Tax consequences

Many companies offer the opportunity to issue an interest-free loan to employees.The tax consequences of such a decision are acceptable for any company, since taxes are not required to be paid. This is due to the fact that the company does not receive any profit in the form of interest from the employee.

At the same time, employees generate a certain income, represented by savings on interest. Therefore, he needs to pay a fee for income received if the company provides an interest-free loan to an employee. Taxes in this case are personal income tax. The fee is 13%, and the tax agent represented by the employer is responsible for the deduction. The company withholds tax on the employee’s salary, but such deduction cannot exceed 50% of the citizen’s income per month.

When is a loan considered repaid?

The moment of repayment of the loan is the day when the employee fully repays the debt to the employer. If it was provided in kind, then the employee’s obligations at the time of return of the property end.

If such a loan is repaid in installments represented by salary deduction, then the day when the entire amount is paid in full shall be considered the moment of termination of relations under an interest-free loan agreement.

Underwater rocks

The execution of such a transaction has nuances that should be taken into account by both parties. These include:

- the contract requires a detailed description of the subject of the transaction, since if it is impossible to identify it, then problems may arise in court;

- directly in the contract, it is required to clearly indicate that a loan is provided without the need for the employee to pay interest;

- the subject of the agreement may be not only the amount of money, but also the property of the company;

- when providing an interest-free loan, the company does not have material benefits, therefore, it is not required to pay taxes;

- the borrower can receive a property deduction if he directs the funds received to purchase real estate;

- if housing is transferred for temporary use, then the transaction will certainly be recorded.

By law, it is not necessary to contact a notary public to certify the contract, but many companies decide to use the services of this specialist, which greatly simplifies the process of concluding a transaction.

Can a company write off debt?

It is allowed for firms to forgive debts to employees, but personal income tax included in the borrowed amount will still have to be paid to the citizen. The tax is deducted from the specialist’s income until the required amount is transferred to the budget. Written-off debt of 13% is subject to taxation. For a company, such a decision is considered not too profitable, since it loses a significant amount issued to the employee. Typically, such actions are performed as a reward for a truly important and necessary specialist.

Conclusion

Interest-free loans may be issued by all employers to employees. The procedure is considered simple and beneficial for every specialist. For this, it is important to correctly draw up a loan agreement, which sets out the necessary conditions for cooperation. It is allowed to enter information on fines into the agreement. Since the company has no material benefit, it does not pay taxes, but the fee must be calculated and transferred by the direct recipient of the funds.