How to indicate the tax period in the VAT return? This question arises for someone who first encounters this form of reporting. Also, for beginners, there are many other questions. After all, VAT has the glory of a complex and unloved by all tax. This is due to various factors, including the fact that greater attention is paid to reporting on it.

Features of VAT reporting

The VAT return is the only report that must be submitted exclusively in electronic form. It must be submitted to the tax authority via the Internet through an electronic document management operator. Such rules apply to all taxpayers, as well as persons who are not recognized as VAT payers, but for some reason are required to pay it from certain transactions.

On a paper form, a VAT return can be submitted only in one case - when a tax agent reports that does not pay this tax for itself. For example, an organization using special regime acquired services from a foreign counterparty that does not have a representative office in Russia. If they are subject to VAT, the buyer must fulfill the function of a tax agent in relation to the foreign seller. After all, he himself cannot pay VAT, since he is not registered with the Russian tax service.

In all other cases, the paper form of the VAT declaration will not be accepted, and the submitter will be considered unreadable. Such an outcome is expected regardless of whether the form is sent on paper by mail or transmitted in person.

The reporting deadlines for VAT reporting have changed since 2015 - now it must be submitted no later than the 25th day of the month following the reporting quarter.

Tax and reporting period - is there a difference?

The final calculation of any tax is carried out for a certain period of time, which is called the tax period. In addition to it, there is a reporting period - a time period, after which it is necessary to pay advance payments, and sometimes to submit a declaration (calculation).

The tax period may include one or more reporting. That is, these periods are different, although they are often identified. For example, the reporting period for income tax is a quarter, a half year, and 9 months, and the tax period is a year. As for VAT, everything is simple - the tax period coincides with the reporting period and amounts to one quarter.

How to indicate the tax period in the VAT return?

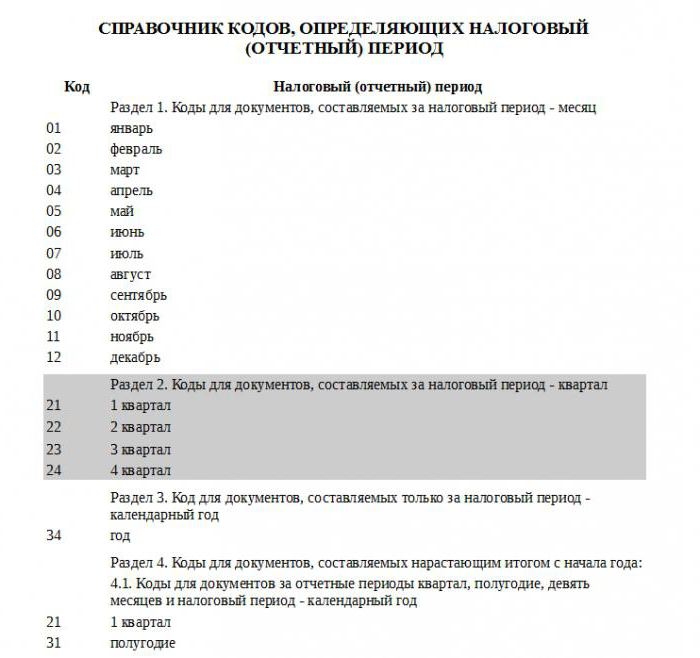

The tax period in the reports is indicated in the form of a code, which is taken from the directory approved by the Federal Tax Service. Each tax period has its own two-digit code. They are universal, that is, installed without reference to the type of payment.

Since the tax period for the payment in question is a quarter, the codes from section 2 of the referenced reference apply. Thus, the first quarter corresponds to the tax period code in the VAT declaration “21”, the second quarter - “22”, the third quarter - “23”, the fourth quarter - “24”.

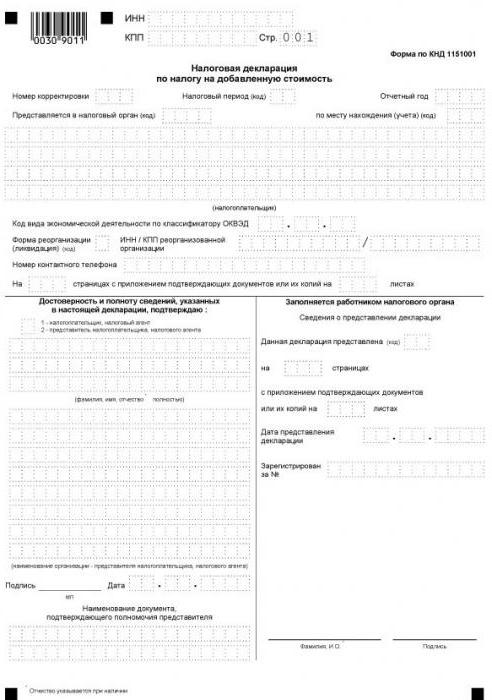

The composition of the declaration

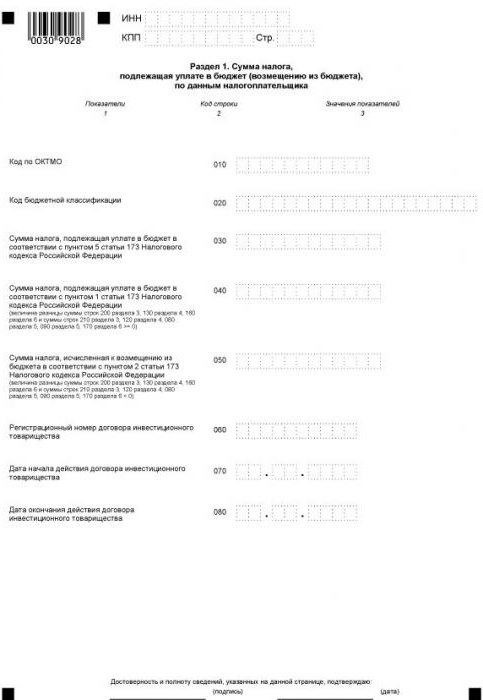

The current form of the declaration includes a title page and 12 sections, some of which have annexes. All reporting entities fill out the first page (title) and section 1. The exception is tax agents who do not pay their own VAT. That is, non-paying entities that, due to certain circumstances, have received the obligation to pay VAT for another person. They put dashes in section 1, and the reporting data reflect in section 2.

As for the other sections, it is necessary to fill out only those of them for which the organization or individual entrepreneur has data.

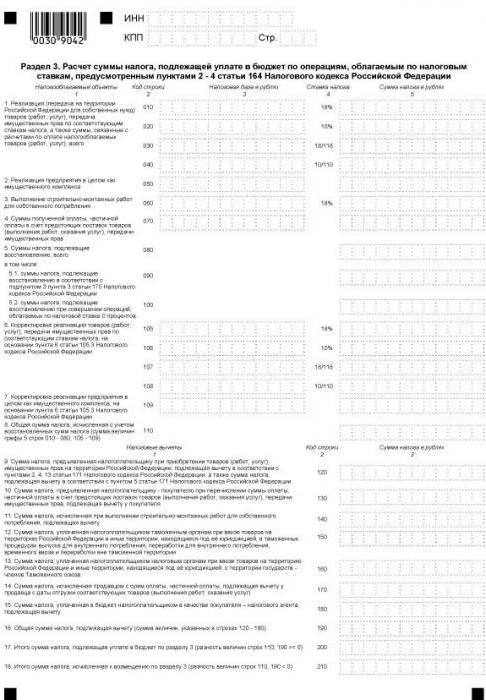

Section 3 is intended for calculating VAT at the rates of 18 and 10%, as well as reflecting tax deductions. It is filled in by all payers of their own VAT, which in the reporting period had operations taxed at the indicated rates.

The following 3 sections of the VAT return are for exporters. The following data is indicated here:

- in section 4 - operations for which the validity of applying the zero VAT rate is documented;

- in section 5 - data for calculating the amount of tax deductions for export operations;

- in section 6 - operations for which the discount rate is not confirmed.

Section 7 is filled out by VAT payers and tax agents who had non-taxable operations in the reporting quarter. This section also reflects the operations to receive an advance payment on account of the delivery of goods, the production cycle of which is more than six months.

Sections introduced relatively recently

Since 2015, information on purchase and sales books has been included in the reporting structure, which reflects all transactions and provides invoice data. This information is indicated in sections 8 and 9, respectively.

For mediation, sections 10 and 11 of the VAT return are provided. These sheets are filled out by agents, commission agents, developers, forwarders - all those who issue or accept invoices in the interests of another person.

And, finally, the last, 12th section of the declaration is intended for persons who are not VAT payers, however they issued at least one invoice in the reporting period, highlighting the amount of tax in it. In this case, the subject has the obligation to pay the allocated VAT and report on this in a timely manner.

How to check declarations

As mentioned above, the invoice information is sent to the tax office as part of the declaration. This helps employees of the Federal Tax Service Inspectorate to identify violators - those who underestimate the tax base, overestimate deductions or do not record individual transactions at all. To simplify this process, the filing of the declaration is done in electronic form.

Identification of violators is carried out through the reports of their counterparties. During a desk audit, the data of the buyer and seller declarations for each transaction are compared automatically. For any transaction from the taxpayer’s purchase book, a pair must be found, that is, the reverse operation reflected in the vendor’s sales book. If the pair is not located or there are any discrepancies in the data, then the tax authority will inevitably have questions.

Therefore, any requisite must be indicated correctly, including the tax period considered at the beginning of this article. There are no trifles in the VAT declaration - any incorrect information may lead to the IFTS requirement to provide clarification. Moreover, problems can arise not only with the taxpayer, but also with its partners.