Material assistance may be provided by the employer to his employee upon his written application. Having considered the situation, management may come to the conclusion that the employee really needs a specific amount. Then a new question arises, both for the accountant and for the employee who receives the help: “are people withheld from personal assistance?”. The answer to this question is not as clear as it might seem. It is worth noting that with regard to material assistance, the taxation of 2016 and 2017 does not have any special differences. Therefore, you can safely rely on the practice of the previous year. It is also worth paying attention to whether material assistance is correctly reflected in the certificate in the form of 2-NDFL. And attention requires reporting 6-personal income tax, which arose not so long ago.

Material assistance: what is it?

The concept of material assistance in most cases is vague. For example, the Tax Code contains a list of clauses specifying types that are tax-free at a rate of thirteen percent. To this, including financial assistance.

However, it is worth noting that the Tax Code of the Russian Federation in most cases lists payments related to emergency situations, such as natural disasters, illness, or the death of close relatives. At the same time, many material assistance is stimulating, for example, in connection with marriage or the birth of a child.

Thus, material assistance can calculate the incentive payments, as well as the amount that goes to the employee in connection with joyless events. In each case, taxes may be levied on both the entire amount and part thereof. And in some cases they are not removed at all.

Payments are lump sum or monthly?

Material assistance can be provided to an employee an unlimited number of times if this provision suits the employer and is confirmed by the organization’s internal document. However, those accruals that are made every month, the Tax Code refuses to understand as material assistance.

This document emphasizes that payments, which can be described as material assistance, exempt from personal income tax, are paid at a time. That is, once a year. So, an employee who is rewarded monthly in connection with the same event will pay personal income tax in full.

PIT: what is taxable?

It is generally accepted that it is the employee’s income that is taxed on income, as, in principle, the name implies. However, it is also worth considering that material assistance is often not included in the employee’s income if it is of a one-time nature.

It turns out that income tax is levied on the entire part of wages, with the exception of material assistance. However, it is worth considering what this assistance is paid for. Personal income tax with financial assistance can both be removed and leave it untouched. Also, when calculating personal income tax, the presence of benefits, such as deductions for the employee himself or for children, is also taken into account. There may also be property deductions.

Any personal income tax deduction is a certain amount that is not taxed from the total amount of wages. That is, if an employee brought a package of documents confirming that he has one child under 18 years of age, namely a birth certificate in which he is registered as a parent, as well as a deduction, then 1,400 of his salary should not be taxed will be. This, in turn, saves 182 rubles per month or 2 184 rubles per year.The rate in the general case for residents of the Russian Federation is thirteen percent.

Material aid. General case

What to do with personal income tax with financial assistance? It is worth noting that the legislation strictly regulated the amount that would not be taxed. There is a certain limit, it is achieved with the amount of four thousand rubles.

However, it is worth making a reservation. Material assistance to an employee is not taxable on personal income tax if he has not reached the above threshold for the year, on an accrual basis. That is, an employee can receive material assistance in the amount of 4 thousand, but it will be fully or partially taxed if in the previous months of this calendar year he already received any accruals of such a plan. And it makes no difference whether this material help was for one thing or not.

Case study

In order to finally understand this nuance, several examples should be considered.

So, if a certain employee in the month of January received two thousand rubles as financial assistance for treatment, personal income tax is not levied on the amount. However, in September, the employee also received a thousand rubles to collect the child in first grade. An internal document of the enterprise, namely the Collective Agreement, this action is provided. At the same time, the total amount of financial assistance for the year amounted to three thousand rubles, therefore, in September, personal income tax will not be withdrawn from financial assistance.

By December, the employee, again relying on the collective agreement of the organization, received another fifteen hundred rubles for the New Year. The total amount, which consists of two thousand in January, one in September and one and a half in December is 4,500. That is, 500 rubles in this case is exactly the excess that will be taxed.

Material assistance: having a baby

Material assistance at the birth of a child is a special article. It is worth noting that it is for this type of accrual that the Tax Code makes an exception. As mentioned above, one-time payments are recognized as material assistance. That is, they are charged once. It is impossible to stretch the amounts partially for several months.

But in this case there are some nuances. The main difference from other payments is that financial assistance at the birth of a child is not taxed up to fifty thousand rubles. However, this amount is calculated per child and is divided into two parents. In the event that each of them receives material assistance at his workplace in connection with this event, the total amount of their charges should not exceed fifty thousand rubles. Otherwise, everything that is charged in excess of the norm will be taxed.

Documents for the provision of financial assistance

Regarding material assistance, taxation 2016 does not specify whether the employer should request certificates from the workplace of the other parent confirming the payment of material assistance for this child. However, many are safe. This is because it is the employer who is responsible for the correct calculation of taxes to the state.

In general, an employee must write a statement addressed to the director or accountant, sometimes addressed to the chairman of the trade union organization. The person responsible for writing out material assistance depends on the organization’s internal documents. A child’s birth certificate is attached to the application, for which they ask for a certain amount. Also, upon request, you need to provide a certificate from another parent. The amount of payment at the place of work of one employee depends on the Collective Agreement.

Case study

A certain couple brought to their places of work applications for the payment of material assistance, which was due to them because of the birth of a son.

The spouse brought a handwritten statement, as well as a birth certificate for the child. In accounting, she was also asked to bring a certificate from her husband's place of work, which stated that the spouse received four thousand rubles per child.Five thousand were accrued to the girl, since this amount was fixed in the organization’s internal documents. Since the total amount does not exceed fifty thousand, the material assistance of the employee is not taxed.

In turn, the father of the child wrote a statement and attached a copy of the birth certificate. He did not require any other documents. He was charged four thousand rubles, as it was indicated in the Collective Agreement for this period. Its payment was also not taxed at a rate of 13 percent.

In total, nine thousand rubles were received per child, which are not subject to taxation, since this amount is less than indicated in the legislation.

Material assistance for burial: personal income tax

Is financial assistance to a PIT person taxed if he asks for it in connection with a mournful event? The funeral of a loved one is just such. It is worth noting that the accrual of such payments can only be approved if a really close person died and the relationship is documented. These include parents, children, sisters or brothers. Cousins or other relatives or spouses do not fit this category, no matter how close the relationship.

It is worth noting that financial assistance for burial or funeral, as well as payments to victims of any natural disasters, are not taxed. The entire amount will not be taxed. However, it is worth returning to the Tax Code and once again recalling that the payment should be one-time. If an employee once received assistance in the amount of ten thousand, then it is not taxed. However, if he will be awarded assistance every month during the quarter, then it is worth taxing it as a general rule, that is, until it reaches four thousand.

Material assistance and 2-personal income tax

Material assistance is also separately reflected in this type of certificate. Therefore, the employee will easily see her in this document.

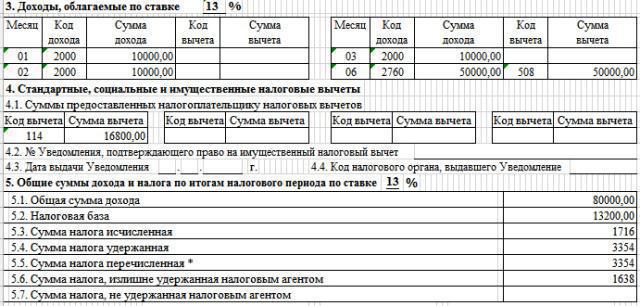

It is worth noting that material assistance up to 4000 in 2-personal income tax is clearly visible. After that, it is no longer allocated, but is in total payments. Material assistance itself comes with a deduction code of 503. This means that this amount is tax deductible at the standard rate.

In this case, the material assistance code in personal income tax is of digital significance. If we are talking about assistance in connection with the birth of a child, then this is also associated with a deduction code under number 508. In general, material assistance has an accrual code of 2760 and is paired with a deduction code.

Form 6 personal income tax. What should not be indicated in the document?

The report on the 6-personal income tax form often raises many questions. Filling it regarding the payment of material assistance also requires clarification.

It is immediately worth noting that you should not specify those types that are paid at one time and the amounts are not fully taxed. These include payments in connection with a natural disaster, victims of terrorist acts or those who wrote a statement for financial assistance in connection with the death of loved ones.

If you specify such payments in this form on line 020, then the main equality of this formula will be violated and the report simply will not converge.

That is, if a certain employee received material assistance for the burial of a spouse in the amount of five thousand rubles, then should material assistance be included in 6-personal income tax? The answer is no.

What should be included in the 6-personal income tax form?

However, is it worth entering the other types of payments that are stimulating? Yes. Those benefits that should be included in this form include those types of assistance that are already fully taxed. They fit into the line "Amount of accrued income", it also has the number 020.

Also, those types of material assistance that are partially taxed. They are also entered in the line with the number 020, but the part that is not subject to taxation is shown in the column “Tax deduction amount”. This may include payments that have not yet reached four thousand per year or partially reached it.And also everything that relies on the birth of a child.

Material assistance to employees is a way to show that the company cares about its employees and supports them. In addition, the Tax Code clearly spells out many points that could cause the accountant doubts. Therefore, you just need to carefully study the regulatory documents, as well as competently fill out the appropriate reporting forms. This will help to avoid problems with the tax service.