By the nature of our activity or as a result of unexpected life circumstances, each of us has at least once encountered such a concept as credit. However, few people thought about the very meaning of the loan. What is he like? And what are the principles of lending?

A small sketch about the loan

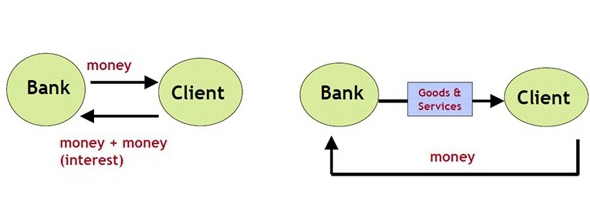

Consider the concept of credit in more detail. So, it is interpreted as a special system of relations, providing for the transfer of finance, securities and things, objects represented in intangible, monetary and commodity form, from one person to another. At the same time, the transfer of valuables, objects and money occurs within the framework of the current legislation, has its own terms, and also involves the repayment and payment of a certain amount for use.

The interaction that occurs between the two above persons is called a credit relationship. In turn, an entity that participates in credit relations and provides objects in monetary, commodity or intangible form is called a creditor. Accordingly, the person who received the loan is called the borrower. An agreement on mutually beneficial cooperation between the lender and the borrower is transferred to paper and has the form of an agreement between the parties. About what principles of lending exist at present, we will describe further.

What is a loan agreement?

A loan agreement is a document that refers to the rights and obligations of the parties. It also refers to the date and reason for concluding the agreement (in this case, receiving the nth amount from one person to another), the transferred amount, the quantity of goods, etc.

The contract indicates the terms for the monthly payment of the loan, the repayment amount, and also provides a schedule on the basis of which the borrower is obliged to fulfill his obligations. For example, the loaned person should repay the loan on the 10th day of each month. What are the terms of the loan, we say further.

The contract also mentions the service fee charged to the borrower during the process of applying for a loan, as well as when making monthly payments through reception points, cash desks, terminals, etc.

On what conditions can I get a loan?

If we talk about the conditions for obtaining loans, then they most often depend on the policies of the lender. Simply put, each financial institution has its own credit products (programs). They also prescribe the conditions of credit. That is, the following points are stipulated:

- minimum and maximum loan limits;

- loan terms (from and to);

- initial and final (or only one of them) interest rate;

- list of documents for registration;

- requirements for potential borrowers (age, length of service, salary size);

- the presence or absence of a collateral, a down payment;

- whether guarantors are needed;

- the possibility of early repayment, etc.

For example, Dil-Bank offers everyone who wants to get a consumer loan for absolutely any purpose up to 500,000 rubles for a period of up to 2 years. This lending program does not require collateral from the borrower, does not provide additional fees. However, when applying for this loan you will need to prepare an income statement. The rate on such a loan is 20%. Application review time - up to 3 days.

Who can provide a loan?

According to the law, banks, MFIs, pawnshops, private individuals, as well as other credit and non-banking organizations can provide loans. In this case, the most common option is a loan at the bank.

What is the credit system?

The credit system is a certain set of diverse credit and financial institutions whose activities are aimed at mobilizing and accumulating funds. For example, in almost every country at the head of the system is the Central Bank, which acts as a regulator. It is he who controls the activities of all financial institutions, issues and revokes licenses, controls the legality of their actions, etc.

Next are large state and commercial banks, MFIs and other organizations.

The financial communication between the participants of the system is carried out in the framework of interbank, partnership, correspondent relations. What lending principles exist, read our article.

What forms and types of loans are there?

Loans are different. In total, they can be conditionally divided into eight types:

- mortgage;

- consumer;

- usurious;

- banking;

- commercial;

- international;

- state;

- pawnshop.

In turn, these types of loans are divided into the following forms:

- forfaiting;

- leasing

- factoring.

A usurious type of loan provides for a private loan provided on bail and at a large percentage of 100-500%. Commercial loans, as a rule, have a commodity form and involve the provision of products from one party to the transaction to another with a certain delay in payment.

Naturally, such a provision of goods as well as a cash loan is issued at interest. Consumer loans - loans issued for specific purposes or without them. With their help, you can take on credit household appliances, furniture, clothes and other valuables.

Bank loans are issued to borrowers on the basis of concluded loan agreements. These types of lending involve the provision of a certain amount at interest and sometimes on bail. Bank loans can be issued to individuals and legal entities, private investors, credit organizations, corporate clients, etc.

Mortgage loans are loans issued for the purchase of finished or under construction housing. They can be both with a down payment and a pledge (in this case, credit real estate acts as a pledge), and without them.

State loans - loans that are organized to compensate for the deficit of the state budget. International loans - loans taken by borrowers of one country from lenders of another. Despite the common features of these types of loans, loan conditions will vary.

Types of loans for purpose

Depending on the purpose of the appointment, loans can be targeted and non-targeted. The first borrower draws up for a specific purpose, for example, to pay for tuition at a university or a wedding. The second are drawn up for any personal needs without specifying a specific purpose.

Specialized Loans

Depending on the type of activity the borrower is engaged in, loans can be:

- agricultural;

- industrial;

- to open and develop a business;

- trade and others.

Also for the purchase of vehicles there are special programs for car loans.

How are loans differentiated by maturity?

If we talk about the terms of lending, then loans are:

- short-term (minimum 1, maximum 360 days);

- medium-term (minimum 360 and maximum 1800 days);

- long-term (more than 1800 days).

Basic principles of lending

Among the principles of lending, we can distinguish such as urgency, payment and repayment. What is meant?

- In this case, urgency involves the return by the borrower of the amount issued by the creditor at a strictly agreed time.

- Paid means that the issuance of a loan by the lender is carried out for a certain monetary reward. In addition, often before issuing a loan necessary for a client, the lender charges a certain amount, called the first installment.

- Repayment, respectively, indicates that the borrower needs to return the amount that he previously received from the lender on time.These are the approximate principles of bank lending.

An additional principle of lending is targeted. It is she who makes it clear for what purposes the borrower plans to spend borrowed funds. In this case, loans issued to certain events with real profit are considered the most reliable.

In other words, it is the principles of lending that allow both parties to the loan agreement to evaluate one degree or another of their responsibility.

What is a loan interest?

For the borrower to use credit funds or objects, a certain fee is charged in the form of interest. In them, as a rule, the refinancing rate set by the Central Bank and the small payoff of the lender, which depends on the organization’s policies and risks, are laid down. You can calculate the amount of interest on the loan yourself, using a bank employee or online calculator.

What are loan risks?

Each lender providing a loan to a borrower experiences certain lending risks. That is, during the entire credit period, the payer may refuse to repay the loan, delay the payment, go missing (for example, having left for permanent residence in another country and not having paid the loan), lose his job and as a result become insolvent, lose his health and limbs in the event of an accident production, die at the hands of an attacker, etc.

In a word, no matter what the reasons for the non-payment of the loan the borrower may have, the lender is not any easier. Therefore, no one will repay the debt. And if the lender has not one, but tens or even hundreds of such clients? In this case, the risks are laid in the interest rate. And also borrowers are invited to provide collateral, guarantors or to pay additional insurance.

What should be the security for a loan?

Collateral for a loan may be any valuable property owned by the borrower. For example, when receiving a consumer loan for the purchase of a mobile phone, this particular product will play the role of collateral in front of the bank. Accordingly, a similar situation is observed both with a mortgage (where credit housing is used as collateral) and with car loans (the car goes on bail).

In addition, securities, valuables, motor and agricultural equipment, production and cooling equipment, equipment and other things of value to the lender can be secured.

If the borrower fails to pay the bills, the pledged item, according to the bank regulations, is sold under the hammer. And the proceeds go to pay off the debt. Observing all these principles of bank lending, you can become a bona fide borrower with a good reputation!