In the process of conducting any entrepreneurial activity, two large categories of costs arise. These are direct and indirect costs. They have different effects on the cost of the final product, and their analysis allows us to judge the effectiveness of the actions taken. We will understand this difficult question.

Direct costs

When calculating the cost of production, any accountant will separate the costs that the enterprise took to produce goods from unclaimed ones. For example, the cost of wood for a sofa will be decisive in determining the final price, but the amount of renting a room cannot be completely transferred to it alone. In this way, direct and indirect costs are determined.

Direct - these are the costs on which the cost of the final product completely depends. They cannot be carried forward or broken down into parts. If flour, water, sugar, cottage cheese and eggs are needed to make a curd cake, then the price of each component will be necessarily included in the calculation.

The same category includes the salary costs of personnel who are directly responsible for the output and depreciation of production equipment.

Indirect costs

Opposite to direct costs are indirect. They are also included in the cost of production, but not completely, but only in certain parts. In fact, the final price also depends on them, but the enterprise does not spend money on them in the manufacture of one unit of goods.

Indirect costs, in turn, may be constants and variables. Permanent practically do not depend on the quantity of products sold, shipped or stored. For example, this is the cost of paying administrative staff or renting a production room. Variables are subject to change. For example, if you need to ship more products, you will need additional transport, gasoline, etc.

Analysis of direct costs of raw materials

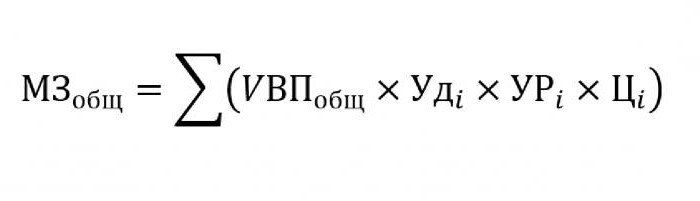

As a rule, indirect costs occupy an insignificant share in the cost of production, while the purchase of raw materials and materials for further processing is estimated at approximately 70% of the price of future finished products. It is very important in this matter to estimate the total amount of costs, which directly depends on the volume of output.

To substitute in the above formula, the following data will be required:

- UVP - the volume of products;

- Oudi - the proportion in the total volume of a single material;

- Uri - mass of consumed materials per unit of output;

- Tsi - the cost of this material.

If you need to calculate the amount of material costs for the production of a certain type of product, then you need to use the same formula, with the exception of the specific gravity of a single material.

Indirect cost analysis

The calculation of various indicators related to indirect costs is very important for the analysis of the effectiveness of the organization. As a rule, data for five, six and even ten years are taken and compared with current indicators. This approach allows us to evaluate in which direction the company is moving - development or extinction.

Indirect are the costs that are included in one of the following groups:

- Costs associated with the operation and use of equipment not occupied in the main technological process.

- General business expenses.

- Costs associated with business or productivity improvements.

Indirect costs for the maintenance and operation of equipment

In this category, indirect costs are those that include depreciation, repair and upgrade costs of all machines and technological equipment, which in one way or another affect the creation of the final product.

Some units during their operation are designed for long-term use, regardless of the amount of work on them. Costs of this type are called conditionally constant. Other equipment wears out depending on how many parts will be made on it. The costs of such machines will be classified as conditionally variable.

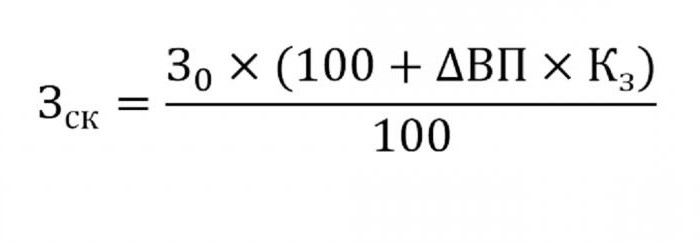

Determining the indirect costs of maintaining equipment will be included in the cost of production. To do this, use the formula below.

- where wck - adjusted costs;

- 30 - the planned amount of costs;

- VP - change in output;

- TOs - coefficient calculated by the correlation method, indicating the dependence of costs on the volume of output.

Other parameters for analysis

If you need to find out in which articles there is too much overspending or saving, the following parameters are used.

First of all, they look at depreciation costs. They increase in several cases:

- too frequent equipment repairs;

- recent machine updates;

- revaluation in connection with inflationary processes.

As practice shows, depreciation is rarely reduced.

Another parameter is the specific depreciation calculated per unit of output. This indicator directly depends on the volume of manufactured goods. The more of them, the smaller the amount of depreciation costs accounted for the unit price.

The amount of expenses for the internal movement of goods increases with the release of new lots, more expensive fuel or worn-out cars.

The amount of depreciation of the inventory involved in the production process is calculated as the product of the number of manufactured products and the consumption level that falls on one product.

Analysis of general expenses

In the process of analyzing various general business expenses use the data of the accounting report for various periods. Let's say you need to find out how the salary of the personnel officer has changed over the past year. To do this, subtract from the last amount that falls at the beginning of the study period. The difference in numbers is analyzed and the reasons for the increase or decrease are found out.

To assess the impact of these costs on the cost of production takes into account their specific gravity in each unit of goods.

Business Cost Analysis

First of all, this includes the cost of shipping the goods to the buyer, market research, advertising, marketing program and so on. Logistics is usually the cost of delivering goods — a science devoted to how to save money when moving goods from a producer to a consumer. This includes everything: the cost of maintaining warehouses, the distance to the user, the most rational types of fuel, etc.

The analysis of direct and indirect costs has one main task: to calculate the reserves and the possibility of their reduction to reduce the cost of production or increase the reserve fund, the funds from which will be used to improve production.