The concept of discount rate is used in order to bring the present value to the future. The discount rate is the interest rate used to recalculate future financial flows to the same amount of current value.

The calculation of the discount rate coefficient is carried out in different ways, depending on what the task is. And the heads of companies or individual divisions in modern business are faced with completely different tasks:

- the implementation of investment analysis;

- business planning;

- business valuation.

For all these areas, the basis is the discount rate (calculation of it), since the definition of this indicator directly affects decision-making regarding investment, valuation of a company or certain types of business.

The discount rate from an economic point of view

Discounting determines the cash flow (its value), which relates to future periods (that is, future future income). In order to correctly assess future earnings, you must have information about the forecasts of the following indicators:

- investments;

- costs;

- revenue

- capital structure;

- residual value of property;

- discount rate.

The main purpose of the discount rate indicator is to evaluate the effectiveness of investments. This indicator implies a rate of return of 1 ruble. invested capital.

The discount rate, the calculation of which determines the necessary amount of investments for future income, is a key indicator when choosing investment projects.

The discount rate reflects the value of money, taking into account temporary factors and risks. If we talk about the specifics, then this rate, rather, reflects an individual assessment.

An example of the choice of investment projects using a discount rate coefficient

For consideration, two projects A and C are proposed. In both projects, at the initial stage, it is required to invest 1,000 rubles. There is no need for other costs. If you invest in project A, then annually you can earn an income of 1,000 rubles. If you implement project C, then at the end of the first and second years, the income will be 600 rubles, and at the end of the third - 2200 rubles. You must choose a project, 20% per annum - the estimated discount rate.

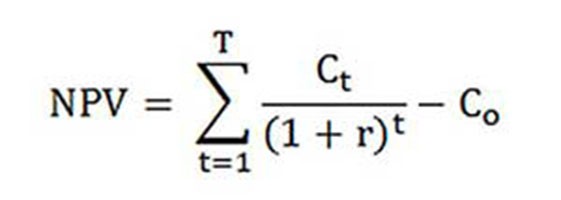

The calculation of NPV (current value of projects A and C) is carried out according to the formula.

Ct - cash flows for the period from the first to the T-th years;

Co - initial investment - 1000 rubles;

r - discount rate - 20%.

NPVBUT = [1000 : (1 + 0,20)1 + 1000 : (1 + 0,20)2 + 1000 : (1 + 0,20)3] - 1000 = 1106 rubles .;

NPVWITH = [600 : (1 + 0,20)1 + 600 : (1 + 0,20)2 + 2200 : (1 + + 0,20)3] - 1000 = 1190 rubles.

So, it turns out that it is more profitable for an investor to choose project C. However, if the current discount rate were 30%, then the cost of the projects would be almost the same - 816 and 818 rubles.

This example demonstrates that the decision of the investor is fully dependent on the discount rate.

Various methods of calculating the discount rate are proposed for consideration. In this article, they will be examined for objectivity in descending order.

Weighted average cost of capital

Most often, when making an investment calculation, the discount rate is determined as the weighted average cost of capital, taking into account the cost indicators of equity (equity) capital and loans. This is the most objective way to calculate the discount rate of financial flows. Its only drawback is that practically not all companies can use it.

In order to conduct a valuation equity The Long-Term Asset Valuation (CAPM) model is used.

At the end of the twentieth century, American economists John Graham and Campbell Harvey interviewed 392 directors and finance directors of enterprises in various fields of activity to determine how they make decisions, what they pay attention to first of all. As a result of the survey, it was revealed that academic theory is most used, or rather, most firms calculate their own capital according to the CAPM model.

Cost of equity (formula for calculation)

In calculating the cost of equity, the discount rate is otherwise considered.

Re - rate of return, or, otherwise, the discount rate of equity, is calculated as follows:

Re = rf +? (Rm - rf).

Where are the components of the discount rate:

- rf - risk-free rate of income;

- ? - a coefficient that determines how the price of stocks of a company changes in comparison with changes in stock prices for all firms in a given market segment;

- rm is the average market rate of return on the stock market;

- (rm - rf) - market risk premium.

Different countries take different approaches to the definition of the components of the model. Much of the choice depends on the general state attitude to the calculation. It is important to study and understand each of these indicators separately, in which way cash flow can be determined. Therefore, the elements of the “Valuation of Long-term Assets” model will be considered in more detail below. And also the objectivity of each component is estimated and the discount rate is estimated.

Component Models

The rf indicator is the rate of return on investment in risk-free assets. Riskless assets are called those when invested in which the risk is zero. These mainly include government securities. The calculation of the risks of the discount rate in different countries is done differently. So, in the USA, for example, Treasury bills are classified as risk-free assets. In our country, for example, such assets are Russia-30 (Russian Eurobonds), the maturity of which is 30 years. Information on the yield of these securities is presented in most economic and financial print media, such as the newspaper Vedomosti, Kommersant, The Moscow Times.

Under the coefficient with a sign, the question in the model refers to the sensitivity to changes in the systematic market risk of indicators of the yield of securities of a particular company. So, if the indicator is equal to one, then the changes in the value of the shares of this company fully coincide with the changes in the market. If the? -Coefficient = 1.3, then it is expected that with a general rise in the market, the stock price of this company will grow 30% faster than the market. And accordingly the opposite.

In countries where the stock market is developed, the? -Coefficient is considered by specialized information and analytical agencies, investment and consulting companies and this information is published in specialized periodicals that analyze stock markets and financial directories.

The rm - rf indicator, which is a market risk premium, is the amount by which the average market rate of return on the stock market has long exceeded the rate of return on risk-free securities. Its calculation is based on statistical data on market premiums for a long period.

Weighted average cost of capital

If, when financing a project, not only their own, but also borrowed funds, then the income received from this project should compensate not only for the risks associated with the investment of own funds, but also the funds spent on obtaining borrowed capital. To account for the value of both equity and borrowed capital, the weighted average cost of capital is used, the formula for calculating below.

To calculate the discount rate, the CAPM model is used. Re is the rate of return on equity.

D is the market value of borrowed capital. Almost represents the amount of loans of the company according to the financial statements. If such data are not available, then use the standard ratio of own and borrowed funds of similar firms.

E is the market value of equity (equity). Obtained by multiplying the total number of shares of an ordinary type company by the price of one share.

Rd represents the rate of return on the borrowed capital of the firm. Such costs include information on bank interest on loans and bonds of a corporate type company. In addition, the valuation of borrowed capital is adjusted, taking into account the income tax rate. Interest on loans and borrowings under tax law is attributed to the cost of goods, thus reducing the tax base.

Tc - income tax.

WACC Model: Calculation Example

Using the WACC model, the discount rate for company X is indicated.

The calculation formula (an example was given when calculating the weighted average cost of capital) requires the following input indicators.

- Rf = 10%;

- ? = 0,90;

- (Rm - Rf) = 8.76%.

So, equity (its profitability) is equal to:

Re = 10% + 0.90 x 8.76% = 17.88%.

E / V = 80% - the share occupied by the market value of share capital in the total cost of capital of company X.

Rd = 12% - the average cost level for borrowing for company X.

D / V = 20% - the share of borrowed funds of the company in the total amount of the cost of capital.

tc = 25% - indicator of income tax.

Thus, WACC = 80% x 17.88% + 20% x 12% x (1 - 0.25) = 14.32%.

As noted above, certain methods of calculating the discount rate are not suitable for all companies. And this technique is just this case.

Firms are better off choosing other methods of calculating the discount rate if the company is not an open joint stock company and its shares are not sold on the stock exchange. Or if the company does not have enough statistics to determine the? -Coefficient and it is impossible to find similar companies.

Cumulative assessment methodology

The most common and most often used in practice method is the cumulative method, with the help of which the discount rate is also estimated. The calculation according to this technique involves the following conclusions:

- if investments did not involve risk, then investors would require risk-free return on their capital (the rate of return would correspond to the rate of return on investment in assets without risk);

- the higher the investor assesses the risk of the project, the higher the requirements for their profitability.

Therefore, when the discount rate is calculated, the so-called risk premium must be taken into account. Accordingly, the discount rate will be calculated as follows:

R = Rf + R1 + ... + Rt,

where R is the discount rate;

Rf - risk-free rate of return;

R1 + ... + Rt - risk premiums for various risk factors.

It is practically possible to determine one or another risk factor, as well as the significance of each of the risk premiums, only by expert means.

Evaluation Recommendations

When the effectiveness of investment projects is determined, the cumulative method of calculating the discount rate recommends taking into account 3 types of risk:

- risk arising from dishonesty of project players;

- risk arising from non-receipt of planned income;

- country risk.

The value of country risk is indicated in various ratings compiled by special rating firms and consulting companies (for example, BERI). The fact that the project participants are unreliable is compensated by a risk premium; a maximum of 5% is recommended.The risk arising from non-receipt of planned revenues is established in accordance with the objectives of the project. There is a special calculation table.

Discount rates estimated using this method are rather subjective (they are too dependent on expert risk assessment). They are also much less accurate than the calculation methodology based on the “Estimation of long-term assets” model.

Expert assessment and other calculation methods

The easiest way to calculate the discount rate and quite popular in real life is to set it by an expert method, with reference to the requirements of investors.

It is clear that for private investors calculation based on formulas cannot be the only way to decide on the correctness of setting a discount rate for a project / business. Any mathematical models can only approximately evaluate the reality of the situation. Investors, relying on their own knowledge and experience, are able to determine the sufficient profitability for the project and rely on it as a discount rate, making calculations. But for an adequate experience, the investor must be very well versed in the market, have extensive experience.

However, it must be assumed that the expert methodology is the least accurate and may well distort the results of evaluating business (projects). Therefore, it is recommended that determining the discount rate by expert or cumulative methods, it is mandatory to analyze the sensitivity of the project to changes in the discount rate. In this case, the investors will be as accurate as possible.

Of course, there are alternative methods for calculating the discount rate. For example, the theory of arbitrage pricing, a dividend growth model. But these theories are very difficult to understand and rarely applied in practice.

The application of the discount rate in real life

In conclusion, I would like to note that most companies in the process of activity need to determine the discount rate. It must be understood that the most accurate indicator can be obtained using the WACC methodology, while the remaining methods have a significant error.

It is not often necessary to calculate the discount rate in the work. This is mainly due to the assessment of large and significant projects. Their implementation entails a change in the structure of capital, the stock price of the company. In such cases, the discount rate and the method of calculating it are agreed with the investor bank. They focus mainly on the risks received in similar companies and in the markets.

The application of certain methods also depends on the project. In cases where industry standards, production technology, financing are understandable and known, statistics are accumulated, the standard discount rate set at the enterprise is used. When evaluating small and medium-sized projects, refer to the calculation payback periods with a focus on the analysis of the structure and external competitive environment. In fact, methods for calculating the discount rate of real options and cash flows are combined.

Please be aware that the discount rate is only an intermediate in evaluating projects or assets. In fact, the assessment is always subjective, the main thing is that it be logical.

There is such a mistake - economic risks are taken into account twice. So, for example, two concepts are often confused - country risk and inflation. As a result, the discount rate doubles, a contradiction appears.

There is not always a need to count. There is a special table for calculating the discount rate, which is very easy to use.

Also a good indicator is the cost of a loan for a particular borrower.The basis of setting the discount rate may be the actual credit rate and the level of yield of bonds that are available on the market. After all, the profitability of the project does not exist only within its own environment; the general economic situation in the market also affects it.

However, the obtained indicators also require significant adjustments related to the risk of the business (project) itself. Currently, the real options methodology is often used, but it is very complex from a methodological point of view.

In order to take into account such risk factors as the option of project suspension, changes in technology, market losses, practices in the evaluation of projects artificially inflate discount rates (up to 50%). Moreover, there is no theory behind these figures. Similar results can easily be obtained using complex calculations, in which in any case the majority of forecast indicators would be determined subjectively.

Correctly determining the discount rate is a problem associated with the basic requirement for information content generated in financial statements and accounting. In other words, if there is reason to doubt whether the assets or liabilities are correctly valued, and whether the cash consideration is deferred, then a discount should be applied.

When choosing a discount rate, it is important to understand that it should be as close as possible to the rate received by the borrower of the creditor bank on real terms in the existing environment.

So, the discount rate for certain assets (for example, for the main ones) is equal to the rate at which the company would have to pay, attracting funds to purchase similar property.