In the process of the existence of any LLC, a situation may happen when some participant decides to finally leave the business. Moreover, he has every right to sell his own share or simply to withdraw the founder from the LLC by simply leaving the membership. However, one must have an idea of what the main differences between these concepts are.

What is the difference?

There are two main differences between what constitutes a sale of a share and an exit of a founder from an LLC:

- After the exit, the purchase and sale of his share is not carried out, but a certain compensation is paid, which is equal to its actual value, while the share itself is transferred to the company.

- During the sale, not even the entire share can be sold, but only a certain part of it, while in case of exit, the company immediately transfers absolutely all of the assets that belong to this participant.

In addition to the fact that the founder may voluntarily withdraw from the LLC, his share may also be transferred to the community as a result of his exclusion or death. It is for this reason that you need to correctly understand the features of each of these options.

Voluntary exit

A member of the company may voluntarily leave him only if this possibility is provided for by the charter compiled earlier. At the same time, it is worth noting the fact that in this situation the founder leaves the LLC without the need for prior approval of this step with other participants. If the charter does not include such a provision, then in this case it will not work out voluntarily.

Also, the participant is not allowed to leave the company in that situation if he is the only entity or, together with him, they want to leave the LLC and other members. The reasons for this are very clear, because such an organization cannot exist if not a single person is in it.

How is the procedure performed?

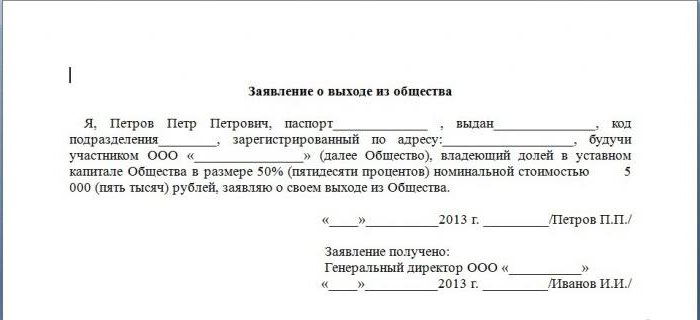

If all the necessary conditions are met, which include the charter of the LLC and the current legislation, then in this case, the participant leaving the company must provide an appropriate application. It is worth noting that this document can be written in free form, but it is compiled in the name of the Director General. You also need to pre-certify it with a notary.

The text of this document should include detailed information about the participant himself, namely:

- passport data, as well as place of residence and name, if the participant is an individual;

- registration data of the organization, if the participant is a legal entity.

Among other things, this statement should include a clearly expressed desire to leave society and at the same time receive the value of the share on hand.

From the moment a statement is submitted on the withdrawal of one of the participants, and at the same time this opportunity includes the charter of the LLC, its share is automatically transferred to the benefit of the company, as a result of which the statement must be transmitted in such a way that this date is fixed with the corresponding mark left on the document , or a separate delivery receipt.

What then?

The company has approximately one month to amend all necessary registration documents. In this case, the tax office, which is engaged in accounting for this LLC, filed an application drawn up in the form of P14001.It must be notarized. This statement includes a document provided by the participant leaving the company, as well as a protocol on his withdrawal.

After the number of founders was reduced due to the withdrawal of one of the participants, he should be fully paid the real value of the share provided within three months from the moment he submitted the corresponding application. The value of the share must be paid in cash. However, by agreement, payment can also be made by various assets.

What happens to a share?

After a person leaves the company, his share replenishes the general authorized capital of the LLC, and over the next year its fate should be determined in one of the following ways:

- it is sold to one or several participants;

- distributed among all other participants in accordance with what their share contains the authorized capital of the LLC;

- sold to a specific person who is not a participant (if this is not prohibited by the established charter).

A message about the sale or distribution of the share of the retirement is valid for a month after the relevant decision is made. In this case, a notarized statement in the form P14001 is sent to the tax inspectorate, as well as a special protocol on carrying out this procedure, a contract of sale of a part, as well as a document that confirms its payment (the last two documents should be submitted only if the part retired participant is for sale).

If the decision to sell or distribute the share is made within less than one month after the withdrawal application has been received, then in this case the documentation package can be submitted only once. At the same time, in the application Р14001 it should be noted that one of the participants left the composition of the founders, and part of it was distributed or sold. If the buyer of this share is another company, and the acquired part is more than 20% of the total authorized capital, then this fact should be noted in the “State Registration Bulletin”, where the corresponding publication should be submitted.

If the participant who leaves the founders of the LLC is the general director, then in this case, even after he leaves the company, he will not cease to be its leader. The thing is that the director’s relationship with the LLC is drawn up by the relevant labor agreement. If such a need arises, you must first terminate any labor relations by officially formalizing the dismissal of this head.

If the share of the withdrawn participant in the specified period has not been sold or distributed, it must be repaid, while the total amount of the authorized capital must be reduced by the total amount of the nominal value of this part, which was received after the founders were changed. It should be noted that the repayment of debt to the tax office must be reported on the application form P13001. In addition, the documentation package includes the following:

- the minutes of the meeting of the founders, including a decision on the repayment of the share;

- a new edition of the charter or various amendments to it;

- a document stating that the company paid the corresponding state duty, which amounts to 800 rubles.

An exception

If, however, any serious conflicts arose among the participants, as a result of which the company cannot continue to engage in normal economic activity, then in this case the exclusion of a certain participant is quite normal. At the same time, one must correctly understand that this is the last response measure, and unlike the way out of the founders of the LLC, the step-by-step instruction is completely different, since the issue is decided exclusively in court.

It is rather difficult to show that a given participant by certain actions or, conversely, inaction causes significant harm to the activities of society. It is worth noting that the possibility of exclusion is peremptory norm. That is, you can resort to it even if the corresponding rule is absent in the charter.

When can I exclude?

What can be officially considered a good reason for the protocol of the meeting of founders to include a decision on the exclusion of a certain site? In accordance with the current legislation, this right appears if one of the founders shows gross violations of his duties, by his actions makes normal activities impossible or creates significant difficulties.

Case studies

There are some of the most common situations that constitute reasons for participants to exit by exclusion by other founders:

- counterfeiting minutes of the general meeting, on the basis of which the appointment of a new director was carried out, conducting all kinds of transactions without the knowledge of the other participants;

- providing counterparties with false information on the liquidation of the company, followed by a proposal to conclude similar agreements with competitors;

- conducting transactions for the sale of various property of this LLC at a lower cost by the General Director;

- deliberate avoidance of participation in various general meetings, as a result of which the society was not able to make important decisions affecting its activities.

There are a fairly large number of such examples, but you can list them all for a long time.

How is an exception made?

Only those participants whose share in the authorized capital is more than 10% can submit an application to the arbitration court on the exclusion of a certain founder. If, in the end, a final court decision is made in favor of the plaintiff, it will constitute sufficient reason for the party to be completely expelled from society. After carrying out such a procedure, a court decision that has entered into force, as well as a statement in the form of P14001 is submitted to the tax office in order to make the corresponding changes to the USRLE.

After a certain LLC participant is expelled, the actual value of the share must be paid to him in exactly the same manner as in the case of a voluntary exit. In addition, the company may also file a claim to compensate for the harm caused by the participant during his stay in the company. But in this situation, it is also necessary to provide sufficiently strong evidence.

Transition of a share after death

If the participant dies, who was an individual at the same time, then in this case part of it is transferred to the heirs along with the rest of the property. In accordance with the current legislation, the adoption of the heritage can be carried out for six months after the participant dies.

In the overwhelming majority of cases, the transfer of the share to the heir is carried out without any restrictions, that is, he enters into the inheritance, as a result of which he becomes a full-fledged participant in the LLC. After the corresponding certificate of inheritance is obtained, several documents must be submitted to the Federal Tax Service:

- an application drawn up in the form of Р14001, in which the necessary information about the new participant will be present;

- copies of the death certificate, as well as a certificate of inheritance (all documents must be notarized);

- protocol of the meeting of participants that a new member has entered the company by right of inheritance of the share.

If necessary, the company may introduce a clause in the charter that other participants must give their consent to transfer the share to the heir, so that subsequently it is possible to more easily regulate the composition of the LLC. If such a condition is present, then in this case the heir will not be able to automatically join the company if he does not have the consent of the other participants.Also, the charter may contain a complete prohibition on the transfer of the share to the heir.

If there is such a clause, or if there is no consent for the share to be transferred in favor of the heir, its actual value must be paid, while the part itself is distributed or sold in the same way as if the founder is withdrawn from LTD. A sample statement of how this procedure can be carried out, you can see above.

What if the heirs did not show up?

If during the six-month period the heirs did not appear or did not want to enter into inheritance rights, then in this case the share of this participant becomes escheated property, that is, becomes the property of the state. After that, the fate of the share already depends on whether the charter stipulated that the part was transferred to the heirs only with the consent of other participants.

If such a condition still exists, and the board of founders does not agree that the state should participate in the company, then in this case the actual value of the allocated share should be paid in favor of the Federal Property Management Agency, otherwise a meeting of participants will be convened to ensure that the LLC adopted a new member in the person of the Russian Federation.

Thus, you need to correctly understand the situation and take into account the characteristics of changes in the composition of the LLC participants. Depending on the way in which the member left the company, various options for the distribution of property left by him are used. Therefore, all these features must be taken into account in the implementation of the allocated share. At the same time, it is necessary to act extremely competently and quickly, because, as mentioned above, in certain situations, the share can simply go to the benefit of the state.