Civil law of the Russian Federation provides for such types of security for the fulfillment of obligations, such as suretys, forfeits, independent guarantees, deposits, etc.

Due to the fact that changes are constantly taking place in the legislation, an increasing interest has begun to show towards an independent guarantee. Let us consider in more detail what this concept includes and how it differs from other provisions.

Definition

An independent guarantee in civil law implies a written agreement between the parties, where one of the parties (guarantor) undertakes, at the request of the other party (principal), to pay a third party (beneficiary) a certain monetary reward, according to those obligations that the guarantor gave. Moreover, this fact does not depend on the validity of the guarantee guarantee.

Drawing up a document in writing allows you to establish the accuracy of the terms of the agreement and to verify the veracity of its issuance by a specific person. But it is important that failure to comply with the written form of the agreement does not indicate an unreliability of the agreement.

The main features of the guarantee:

- Independence, independence from the obligation provided by it.

- Irrevocability (the ability to revoke a guarantee arises only when indicated in the agreement).

- Retribution (the provider pays money to issue a guarantee).

- A high degree of formalization of relations.

- Inexpressibility of rights.

Issue of a document

An independent guarantee, as mentioned earlier, is issued in writing. This document can be issued:

- banks and other credit organizations;

- other commercial organizations.

The issuance of a guarantee is a one-way transaction, since the desire of one party (guarantor) is sufficient for its implementation. At the same time, such a transaction legally binds a financial institution with the possibility of a customer submitting requirements for fulfilling obligations.

The main symptom

An independent guarantee as a way to ensure the fulfillment of obligations has the main jurisprudence - this is the absence of accessibility. This means that the agreement:

- Does not expire with the termination of the main obligation, and also does not change with its change;

- cannot be considered invalid if the underlying secured obligation is invalid;

- does not give the guarantor the right to invoke objections related to the secured obligation if the beneficiary makes certain demands;

- does not make the validity of the guarantor's obligation to the beneficiary dependent on the requirements of the principal, which are based on his relationship with the beneficiary or the guarantor;

- argues that the guarantor’s liability for the payment of money must be fulfilled at the secondary request of the beneficiary even when the secured obligation is fulfilled, terminated or is invalid.

Subjects

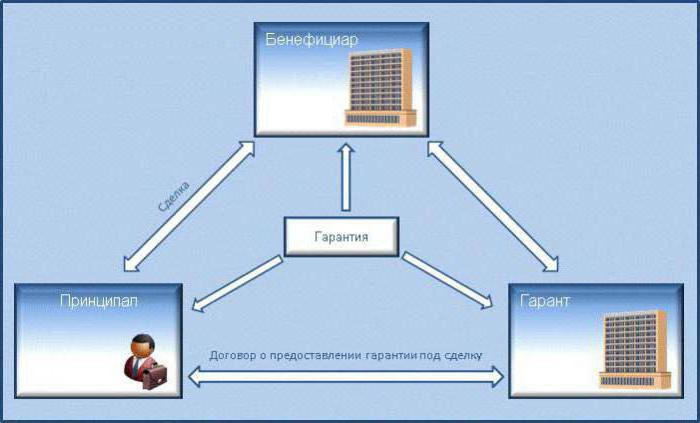

An independent bank guarantee is presented by three subjects of legal relations:

- Guarantor. In this case, these are banks and other credit organizations, as well as commercial organizations, which are entitled to issue a written agreement that includes an obligation to pay money if the creditor submits a written request for payment, drawn up according to the terms of the bank guarantee.

- Principal. This is a person acting as a provider of services (goods). In case of default, the principal is obliged to pay a certain amount of money.

- BeneficiaryThis is a person who is a customer receiving either a service (product) or cash for failure to fulfill prescribed obligations.

Ground for issuing

An independent guarantee as a method of security can be issued based on the request of the principal, which is determined by agreement of the financial organization and the principal on the procedure and principles for issuing guarantees.

But the legislation does not establish the obligation to conclude a written agreement between the bank and the service provider, and its absence does not entail the fictitious nature of the guarantee obligation of the financial organization to the customer.

But if a written agreement is drawn up between the principal and the guarantor, then it becomes the main basis that determines:

- guarantee issuance system;

- mutual settlements of the parties;

- the right of recourse of the financial organization to the debtor, its quantity and implementation procedure.

Moreover, the latter is determined solely by agreement of the bank and the debtor and cannot be unconditional. This is necessary in order to prevent possible abuse by the bank.

Content

An independent warranty agreement must contain the following conditions:

- the maximum amount payable by a financial institution;

- the period for which the warranty is issued, or an indication of a legal fact in which the termination of the warranty occurs;

- basic rules for making payments;

- a list of conditions under which the amount of the guarantee payment may be reduced;

- the possibility or lack thereof of the transfer by the creditor of the right to demand money to a third party.

The number of conditions and their details must comply with the requirements contained in the agreement between the bank and the debtor to issue a guarantee. The following must be indicated in the text:

- name of financial institution;

- guarantee amount;

- warranty period.

The amount of the bank’s obligations under the guarantee is limited to paying the amount for which the guarantee was issued. The procedure and methods for calculating the guarantee amount may be different and include the conditions for calculating interest.

But the bank’s liability to the customer for failure to fulfill obligations under the guarantee agreement is not limited only to the amount for which the guarantee was issued, unless otherwise specified in the agreement. That is, a financial institution may be liable to the creditor on a common basis. Bank violations can be expressed in various aspects: delayed payment, unjustified refusal to pay, etc.

Since the guarantee obligations are of a financial nature, in case of delay the guarantor may be held responsible for failure to fulfill the monetary obligation.

Kinds

The types of independent warranty may be as follows:

Depending on the form of obligation:

- tender guarantee;

- executive guarantee;

- refund guarantee;

Depending on the ability of the guarantor to revoke the issued guarantee:

- revocable;

- irrevocable;

Depending on the customer’s right to transfer to another person, require the bank to fulfill the obligation:

- transmitted;

- inexpressible.

According to general rules, a correctly issued guarantee cannot be revoked unless otherwise provided by agreement. Also, according to general rules, the beneficiary cannot transfer his rights to demand the performance of an obligation to a third party, unless otherwise provided by agreement.

Form requirements

An independent guarantee agreement must contain a list of basic details, without which the document will be considered invalid. These include:

- date of issue;

- name of the guarantor;

- name (details) of the principal;

- name (details) of the beneficiary;

- obligation guaranteed by the guarantee;

- Amount payable

- validity;

- circumstances under which the warranty comes.

At the same time, a certain rule is established for the guarantee form. The guarantee form should allow to determine its conditions and ascertain the truth of its issuance.

Bank Responsibility to Principal

A principal is a service provider or product obligated to fulfill certain requirements. The guarantor is a financial institution that provides an independent guarantee as a way to fulfill obligations.

A financial institution is required to:

- Provide a guarantee on a general basis and issue it in writing.

- Inform the principal about the requirements of the beneficiary and give a copy of these requirements.

- Inform the principal about the suspension of the guarantee (if this fact exists).

- Notify of termination of warranty.

Beneficiary Responsibility to Principal

Recall that the beneficiary is the customer who receives either the service (product) or monetary compensation for failure to fulfill the obligations. An independent bank guarantee also imposes certain obligations on the beneficiary to the service provider. They mainly include the obligation to pay compensation due to damage arising under the following circumstances:

- Submission by the beneficiary of doubtful documents.

- Illegal demand by the customer of funds from the bank.

Judicial practice remembers cases when the customer tried to receive money under the guarantee, despite the fact that the principal fulfilled his obligations in full. The beneficiary had as his goal personal enrichment, which is considered fraud.

Responsibility of the supplier to the bank and the customer

An independent guarantee is the unity of obligations of all parties to each other. The supplier and customer are bound by the obligation to supply services or goods, and the guarantor is considered an intermediary between them. The responsibility of the supplier to the bank is as follows:

- The supplier is a legal entity established on the basis of legal norms, licensed to operate.

- All documentation must be submitted on time and be signed by the supplier (if the signature is from a third party, then he must have authority for this).

- Only true information can be provided.

- The supplier must pay cash for the warranty.

- Cash compensation varies from the amount of security.

- The supplier must reimburse the guarantee payments made due to default.

- The current account must be provided with the necessary amount of funds for settlement with the bank.

- All financial transactions are made through the supplier’s account.

- Submission of all necessary documentation, if required by the guarantor.

- Preservation of confidentiality of information, if provided for by agreement.

The supplier has obligations to the beneficiary:

- Proper implementation of the terms of the agreement.

- Warranty

According to the terms of the agreement, if the debtor is a bank, then he must not fulfill the obligations of the principal. That is, a financial institution should only pay monetary compensation.

Presentation

The agreement provides for a specific procedure for the customer to submit cash claims:

- substantiation by the customer of his requirements in writing with all the indicated documents attached;

- an indication of the circumstances that caused the customer to turn to the guarantor for the provision of guarantee payments.

In turn, a financial institution should:

- send a copy of such a request to the supplier;

- within five days to consider the customer's request and make a decision.

If the result is positive, the beneficiary receives guarantee payments. If the outcome of the case is negative, the guarantor must provide reasonable arguments. These include:

- Submission of a claim later than the deadline.

- Recognition of the requirement as inappropriate.

The refusal is made in writing. In addition, the payment can be suspended for up to seven days in the following situations:

- Documents provided by the customer are fictitious;

- the circumstances specified in the guarantee agreement did not arise;

- primary obligation is not valid;

- performance under the main obligation is accepted without contradiction.

Termination

An independent guarantee as a way of securing obligations shall terminate in the following cases:

- The customer received guarantee money for which a guarantee was issued.

- The agreement for which it was signed has expired.

- The customer waives his rights set forth in the agreement.

- Customer and financial institution accept agreement to terminate the warranty.

Among other things, the guarantor must immediately inform the supplier of the termination of the agreement. The guarantee should also include information on how the supplier will refund the money paid to the beneficiary to the bank.