Many people have different non-residential real estate properties that are not used for any purpose. The best option is their rental, as under such conditions a constant and high income is provided. For this, the landlord can act as an individual, individual entrepreneur or business owner. The procedure for renting non-residential premises should be carried out competently, for which official tenders are drawn up with tenants. The need to pay taxes on income received is taken into account.

Rules for providing objects for rent

Many property owners use this kind of activity. Leasing non-residential premises allows you to get a high passive income. In this case, the lessor may be:

- an individual who is the direct owner of the property, therefore, he must have official documents for this property;

- An individual entrepreneur specially registered with the Federal Tax Service to conduct this activity, moreover, it is usually chosen by the employers of the STS, PSN or UTII to pay taxes, since using the simplified modes it will not be difficult to calculate and pay tax, as well as submit a declaration;

- a company represented by a legal entity, and enterprises can, like individual entrepreneurs, use simplified tax calculation systems.

When drafting a contract by any of the above owners, various nuances are taken into account. If the rental of non-residential premises is carried out without formalizing and registering income with the Federal Tax Service, this is an illegal activity for which the owners of the premises are held liable.

Rules for leasing objects by individuals

Private citizens can own different real estate. They are used for various purposes, such as:

- office creation;

- warehouse organization;

- formation of a manufacturing enterprise;

- creation of shops.

A citizen may act as a party to a lease. People should be the direct owners of the objects, so they are required to have the relevant title documents and an extract from the USRN. The features of the lease of non-residential premises by an individual include the following:

- Citizens must make an entry in Rosreestr in advance that the existing premises are non-residential, with additional technical and cadastral parameters to be indicated;

- if the premises are not registered with the cadastre or are unaccounted for, then it is not allowed to officially transfer it for use to other persons;

- the commissioning of the property to companies or other citizens is a property transaction, therefore, without fail, it concludes a civil contract with the owner;

- so that the documentation is formalized and competent, the agreement is drawn up exclusively in writing, after which it is certified by a notary and registered with the Federal Registration Service.

Often an agreement is drawn up for a period not exceeding one year. Under such conditions, it is not required to register the document with the Federal Registration Service.

What documents are required from an individual to conclude a transaction?

If the leasing of non-residential premises by an individual is realized, then the citizen must prepare certain documentation in advance. It includes such papers:

- passport of the citizen who owns the premises;

- certificate of ownership, which can be replaced by a new extract from the USRN, which indicates the direct owner of the object;

- technical certificate;

- other technical documents issued to the owner by BTI employees;

- extract from Rosreestr, confirming that the facility does not have any encumbrances represented by arrest, bail or other restrictions.

It is allowed to involve a representative in the transaction, but he must have a notarized power of attorney.

Are taxes paid by individuals?

Quite often, citizens who own real estate use this type of activity to earn money. Renting non-residential premises brings people a fairly significant passive income.

If the registration of the contract is carried out in Rosreestr, then information from this institution is sent to the nearest branch of the Federal Tax Service to record citizens' income. Therefore, the lease of physical. non-residential premises requires the calculation and payment of income tax.

For this, it is required to annually submit to the Federal Tax Service a 3-NDFL declaration, which indicates all the citizen's income from leasing the property. Additionally, this document provides the correct size of personal income tax. Therefore, 13% will have to be paid from the amounts received. Due to such a high tax burden, citizens often prefer to register an IP or open a company in order to significantly reduce the amount of the fee, since when using simplified regimes, the tax amount can be reduced to 6% of all income.

Nuances for IE

Many citizens who are owners of real estate, which they prefer to lease, specially open IP for these purposes. In this case, they can use simplified modes when calculating the amount of tax. Leasing of non-residential premises to the IP occurs taking into account the nuances:

- the conclusion of the contract with the tenants is officially recorded by an official agreement, which sets out the duration of the contract, features of the property, rental price and other important features;

- if the term of the agreement exceeds a year, then the contract is registered with the Federal Register;

- IP taxes are certainly paid for the income received, for which the entrepreneur can choose the patent system, STS or UTII;

- direct transfer of funds should be recorded, for which receipts are drawn up, but the most often transfer money to a current account, so you can prove the receipt of money using bank statements.

Through the use of simplified tax systems, citizens are able to avoid paying a significant tax. Most often, when renting non-residential premises, SPs choose UTII, because when using this tax the same amount is paid quarterly. The tax in this case depends on the size of the premises, so the rental price does not affect it.

Be sure to officially lease non-residential premises IP. Taxation depends on the chosen regime, but it is important not only to correctly calculate and pay taxes in a timely manner, but also to prepare declarations necessary for employees of the Federal Tax Service.

What documents are required from SP?

If the owner of non-residential real estate is an entrepreneur, then in order to draw up a contract with a tenant, the following documents should be prepared:

- certificate of registration and registration;

- passport of a citizen;

- title documents for the property;

- technical papers on the facility.

A correctly drawn up contract is by all means transferred to the Federal Tax Service together with the declaration, since it serves as confirmation of the conduct of a specific activity.

The specifics of the rental of premises by companies

Often, various non-residential objects do not belong to private individuals, but to enterprises. Firms often make the decision to lease non-residential premises. The procedure in this case has the following features:

- the company may not be the owner of the object, as it may act as an intermediary;

- a civil contract is drawn up with tenants, to which different documentation from the company is attached;

- the organization with the income received must pay tax calculated on the basis of the applicable tax regime, and companies can combine several systems at once in order to save money on fees.

If the company is not the direct owner of the object, then it can sublet it. Under such conditions, it is required to obtain permission for this activity from the owner.

What documents are required from the company?

If the company acts as the lessor, then for the preparation of the contract it is required to prepare the documentation for the company:

- certificate from the register;

- constituent documentation of the enterprise;

- title papers on the object confirming that the company really has rights to lease this premises;

- if the object is subleased, the company must have permission from the owner for such activities;

- the founder, who is the owner of the business, can draw up a power of attorney for his employee, as a result of which he has the appropriate authority to carry out the transaction.

Most often, firms with significant areas rent them out because they do not use them independently for any purpose. Leasing of non-residential premises provides a significant passive income, therefore, many firms resort to this method of earning money. When drawing up an agreement with a company, you should definitely register it with Rosreestr.

Rental of facilities by the municipality

The administration of any city owns many different real estate objects, which can be residential or non-residential. In this case, the city authorities may decide on the need to lease these objects to direct users. Funds received from such activities will be directed to the local budget.

Under such conditions, it is required to observe the correct order of delivery of objects. For this, the nuances are taken into account:

- official tendering is certainly held to determine the tenant;

- a lease is concluded with the tenderer that offers the highest rent;

- tenders are held in the form of an auction, and individuals, individuals or organizations can take part in it;

- To participate in the tender, you must submit a special application on the website of the regional administration;

- only after registration, all participants are invited to auction;

- All applicants pay a security deposit represented by an entrance fee, and usually it is 10% of the value of the property;

- rental price is calculated based on the cadastral price of real estate;

- if an application is submitted by only one bidder, then bidding is not held, so the applicant draws up a lease without an auction.

The administration may provide an opportunity to issue a contract for a long period exceeding 10 years.

Rules for drawing up a contract

Regardless of who the landlord is, it is important to correctly draw up a lease. It is with its help that a competent registration of a property transaction is carried out. The lease agreement for non-residential premises must contain the following information:

- indicate the place and date of its compilation;

- parties involved in the transaction are registered;

- if participants are individuals, then their F. I. O., dates of birth and information from passports are registered;

- if the lessee or lessor is a company, then its details are indicated;

- The technical features of the property, as well as the address of its location;

- lists the conditions on the basis of which real estate can be used;

- The lease term and cost are indicated;

- it is allowed to include a clause on the basis of which in the future the tenant will have the opportunity to buy property;

- the rights and obligations of each participant in the transaction are given;

- the responsibility of the parties is indicated, since if for various reasons they violate the clauses of the contract, different sanctions or other measures of influence will be applied to them;

- conditions are given on the basis of which a contract can be terminated ahead of schedule;

- lists situations when you have to go to court to resolve various conflict issues;

- various force majeure circumstances are entered in which the participants in the transaction must behave in a specific way.

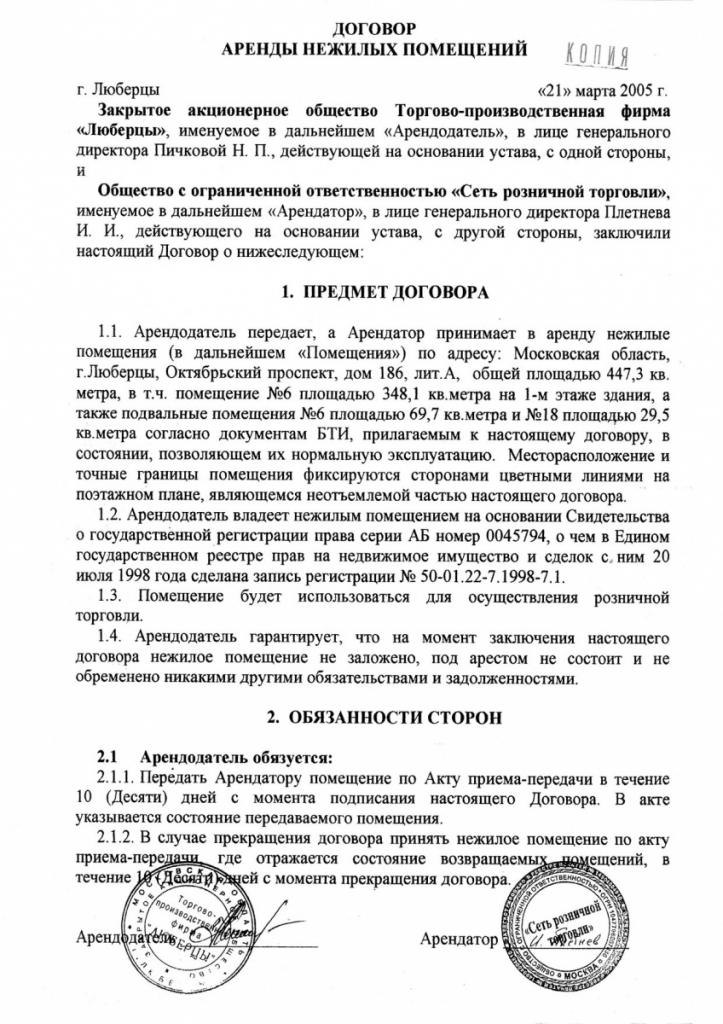

This documentation is not required to be certified by a notary. With the help of this official document, the procedure for renting residential and non-residential premises is regulated. The documentation is drawn up in triplicate, since one remains with the lessor, the second is transferred to the lessee, and the third is used for registration at the Federal Register. The contract comes into force only after registration. It is allowed, if there is an agreement between the parties, the extension of the contract. A sample contract is presented below.

Rules for drawing up the act of acceptance

As soon as an agreement is drawn up, on the basis of which the non-residential premises are leased by an individual entrepreneur, private person or company, it is required to transfer the object to the lessee.

The transfer is carried out directly within the time specified in the contract. For this, it is advisable to draw up an act of reception and transmission. A document is formed in the presence of third parties confirming that the parties to the transaction are conscientious and competent.

The document lists all the parameters of the existing property, which include:

- condition of floor and wall coverings;

- the availability of plumbing fixtures;

- location and technical features of communications.

If the room has furniture, then it should be listed, and also indicate in what condition it is.

What tax regimes are used by the lessor?

Property owners who rent real estate receive a certain income from this process, from which tax is required to be paid. Individuals pay 13% of all income. Due to such a high tax burden, landlords prefer to open an individual entrepreneur or company. For calculations, different tax regimes can be selected:

- STS Under this regime, 6% of all cash receipts or 15% of net profit is paid. Local authorities may increase rates for office or retail real estate. The tax base is income for a year of work or profit from activities. For small businesses, some regions introduce incentives. Additionally, due to tax transfers, the amount paid by entrepreneurs for themselves to the PF and other funds is reduced.

- Patent for leasing of non-residential premises. Such a tax system is considered the most beneficial for many entrepreneurs. Only IP patent can be applied. Renting a non-residential premises under such conditions does not require the preparation and submission of various reports to the Federal Tax Service. Therefore, it is enough just to initially acquire a patent for an optimal price for a specific period of time. They can acquire IP patent for different periods. Renting a non-residential premises using this mode is considered a profitable process.

- BASIC. Rarely is this system chosen for renting out properties, as you have to pay a large number of taxes and do accounting. Typically, this mode is used by firms that do not want to combine multiple systems.

- UTII. The lease of non-residential premises in this mode is usually chosen only if there is a small-sized object. If the room has a significant area, then it is more advisable to choose a simplified tax system or a patent. When calculating UTII, the physical indicator represented by the area of real estate is taken into account.Therefore, it is optimal to choose this mode if the object in size does not exceed 30 square meters. m

The choice of a specific system depends on the immediate tenants. Some firms and individual entrepreneurs prefer to combine several regimes at all, which makes it possible to reduce the tax burden.

Conclusion

Renting various non-residential premises for rent is considered a profitable process. It can be carried out by private individuals, individual entrepreneurs or companies. Firms may not be owners of objects at all, therefore they act only as intermediaries.

The procedure for providing real estate for rent involves the competent execution of a transaction, for which purpose an official contract is compiled between the participants, registered in Rosreestr.