PIT is the main type of direct taxes. It is calculated as a percentage of the total income of an individual after deduction of actually confirmed expenses. Next, we consider aspects related to personal income tax: what is the object of taxation of personal income tax, how is tax calculated, types of rates, and so on.

reference

The decryption of personal income tax in different sources may differ, but the interpretation “personal income tax” is most often found. In the Russian Legislation, the personal income tax payment system is regulated by the Tax Code. This amount is withheld from all individuals receiving official income from personal income tax objects, the following categories are recognized by them:

- Wage.

- Prizes.

- Income from the sale of property.

- Compensation for intellectual activity.

- Winning the lottery and other gifts.

- Payment on temporary disability sheets.

It is worth noting that the tax on the mentioned income is not paid by individuals themselves, but by the institutions from which it was received. The only exception is income received in kind.

Interesting! Any citizen can independently find out the amount of the tax by requesting a certificate from the employer in the form of 2-personal income tax.

Tax payers

The Tax Code of the Russian Federation stipulates that all individuals are divided into two categories of personal income tax payers:

- Residents of the Russian Federation.

- Non-residents of the Russian Federation who profit from sources registered in Russia.

These statuses used in taxation are not associated with the presence of citizenship in a person or his continuous residence, but with the duration of the actual stay in the Russian Federation for 12 months in succession. In other words, even the citizens of our state may not fall under the definition of a resident if, during the last 12 months following each other, they have been in their homeland for less than 183 days. While foreigners, by contrast, can become tax residents if they spent 183 days or more in Russia in a row over the past 12 months. But in this case, it is important to take into account the norms of international protocols in order to exclude double taxation.

Taxpayer status

The letter of the Ministry of Finance No. 03.05.01.04 / 120 dated May 3, 2005 indicates that the status of a tax resident of the Russian Federation is assigned regardless of the citizenship of the individual and the circumstances by which he resides in the territory of our state.

The confirmation of the tax status of the payer is carried out in the following cases:

- At the end of the tenure of a foreign citizen or a person who does not have Russian citizenship in the current year.

- For a period of time starting after 183 days of stay in the territory of Russia of a foreign or Russian citizen, as well as a person who does not have citizenship.

- On the day of the departure of a Russian citizen to a permanent residence located abroad in the current calendar year.

A foreigner temporarily staying in the territory of Russia is a person who is staying in the country on a issued Visa or in a manner that does not involve obtaining it, a citizen who has not received a residence permit, as well as a decision on temporary residence.

The main document determining the status of a foreigner temporarily in Russia is a migration card, which stores all personal information about him, in addition, it controls the duration of his stay. Foreigners permanently residing in Russia are considered persons who received a residence permit.

What is required to confirm the status

You can obtain confirmation of the status of personal income tax payer exclusively at the Office of International Partnership and Information Exchange of the Federal Tax Service of the Russian Federation, documents are accepted on a “single window” basis. So, consider what documents are required for this:

1. An application written in free form with the following information:

- The time period for which it is necessary to obtain confirmation of the status of a tax resident of the Russian Federation.

- Name of the country where the Tax Service is located, which requires this confirmation.

- The applicant's initials and addresses of his residence in both countries.

- Telephone number for communication.

- Description of the attached documents.

2. Photocopies of documents arguing that the taxpayer is making personal income tax on a taxable item located in another country. These include:

- Agreement / contract.

- Resolution of the general shareholders meeting on the payment of dividends.

- Invitation and other available documents.

- Photocopies of all pages of Russian and foreign passports.

- The calculation table of the temporary period of stay on Russian soil (in free form).

- Additionally, for stateless individuals - a copy of a document confirming the fact of registration at the place of residence in the Russian Federation.

- Additionally, for an individual entrepreneur - a photocopy of a document on registration with the Tax Authority certified by a notary (the document is considered valid for 3 months), a photocopy of a certificate of entering data in the state register of entrepreneurs.

A document confirming the status of a tax resident of the Russian Federation can be executed as follows:

- Help in the established form.

- By certifying the appropriate form approved by the legislation of a foreign state.

In our country, the tax regime for the income of an individual depends solely on the tax status of a citizen, or rather, he is a tax resident of the Russian Federation or not. As we found out earlier, this factor is not determined by citizenship or nationality. This division is accepted all over the world, because it allows you to set different taxation procedures for residents and non-residents.

Object of taxation

The object of taxation of personal income tax is considered to be profit that was received by an individual during the reporting period, that is, a calendar year in both monetary and unconditional forms, including material gain. For residents, this is all income derived both in Russia and outside the state. For persons who are not residents of the object of personal income tax, only profit received from sources registered in Russia is considered.

A clear list of income received from Russian and foreign sources is prescribed in article 208 of the Tax Code, which also spells out all the criteria reflecting the types of these incomes. Income includes all charges for the implementation of work and other activities, profits from the sale, as well as other use of property (for example, renting a house or apartment), insurance payments, dividends, etc.

The tax base

The tax base for personal income tax is a reflection of the taxpayer’s profit in cash. When calculating the tax base, all the income of the personal income tax payer is taken into account both in material and in kind. In simple words, this is the salary before withholding the amount of personal income tax (the decryption is given at the beginning).

In addition, material benefits are included in the tax base. Only those amounts that are deducted by decision of the court or other competent authorities from the personal income tax payer for the object of taxation are not included there, the tax base in this case is reduced by the amount of such deductions.

The amount of tax depends on the rate, expressed as a percentage. The basic value is 13%, but before making the calculations, it is necessary to establish the type of income and the corresponding rate for it. So what are the interest rates on taxes?

- Nine percent - this rate is accepted for such types of profit as dividends (until 2015), interest on bonds with mortgage compensation issued before the beginning of 2007, profits of the founders of trust regulation with mortgage coverage, acquired on the basis of mortgage certificates (provided that they were received before the beginning of 2017). The codes in the personal income tax certificate are the following: 1010, 1011, and 1110.

- Thirteen percent - at this rate, tax is calculated on income received by a tax resident in labor activities from sources located both in Russia and abroad.

- Fifteen percent - is used to calculate tax on personal income from dividends received by tax non-residents of sources registered in Russia.

- Thirty percent - at this rate the tax on income of non-residents is calculated, with the exception of certain objects of personal income tax: dividends from equity participation in the work of Russian companies, payments for activities carried out under the patent, wages of foreign highly qualified specialists, payments for the refugee’s labor activity and persons who received temporary asylum in Russia.

- Thirty-five percent is the tax rate used to calculate the amount of withholding from lottery prizes and prizes, from interest income on deposits with financial institutions, from amounts saved on interest on loans, from fees for using funds of participants in credit consumer cooperatives, as well as from interest on loans issued to agricultural cooperatives.

What tax is not paid

The tax on personal income is not subject to only certain accruals:

- Benefits issued from the state.

- Pension accruals paid by the state to persons who have reached retirement age.

- Legislative compensation payments.

- Alimony.

- Financial assistance in the event of the birth of a child up to 50 thousand rubles, the tax is deducted from the amount above this and transferred.

- Income from the sale of property owned for more than three years.

- Income received in the form of inheritance. Income received as a gift from the nearest relatives or family member.

- Other types of income prescribed in chapter 23 of the Tax Code.

How to calculate personal income tax

Before proceeding with the calculation of the amount of personal income tax, you should look into the Tax Code. Article No. 225 describes this process in detail with all the existing nuances. It says that tax is calculated as a percentage of the tax base that is appropriate to the tax rate. So, how to calculate personal income tax on the amount? The formula is as follows:

Personal income tax = tax base * rate for this type of tax.

Here is a sample calculation of personal income tax on salary:

The employee’s income for the last month amounted to 54 thousand rubles, no deductions are provided for him. We calculate the tax at a rate approved by the Legislation of 13%, that is, it turns out that the accountant will accrue personal income tax for the total amount of income.

Personal income tax = 54,000 * 13% = 7,020 rubles.

This amount will be deducted from the employee's salary.

Calculation procedure and terms of payment of personal income tax

The tax calculation procedure is as follows:

- Define all income for the last year for which tax is provided. Suppose this is the salary before personal income tax.

- Define the established tax rate for each type of income.

- Determine the tax base for personal income tax for a calendar year.

- Calculate personal income tax.

- Calculate personal income tax.

In some cases, organizations calculate personal income tax from the "reverse", that is, they know exactly how much the employee should receive in their hands, and are based on it. And from the same amount they determine what wages to indicate in the labor agreement. This can only be done if the employee does not have any deductions.To calculate the tax on personal income from the “reverse” use the following formula:

Personal income tax = income of the employee received by him * tax rate / 100%.

This scheme is also called the formula for calculating personal income tax on the amount at hand.

Tax Terms

According to the established rules, it is necessary to transfer the tax on the same day when the calculation of the individual was made, the maximum for the next day. The specific deadline for the payment of personal income tax depends on the type of income, you can familiarize yourself with these data below.

- One of the most common questions when to transfer personal income tax from a salary? Transfer should be made the day after settlement.

- The tax on the receipt of material benefits is also transferred the next day after the payment of the next cash income.

- Income in kind.

- The amount of personal income tax is transferred the next day.

- The income of the seconded employee. The tax is paid on the 1st of the next month in which the expense report was approved upon the employee’s return.

- Benefits and vacation pay. Personal income tax is transferred on the last day of this month when the employee received the payment.

If the tax payment day falls on a calendar weekend or holiday, it is transferred to the priority working day.

Important! For late tax payment penalties are charged. Be careful with the designation of the status of the payer when paying a fine on personal income tax.

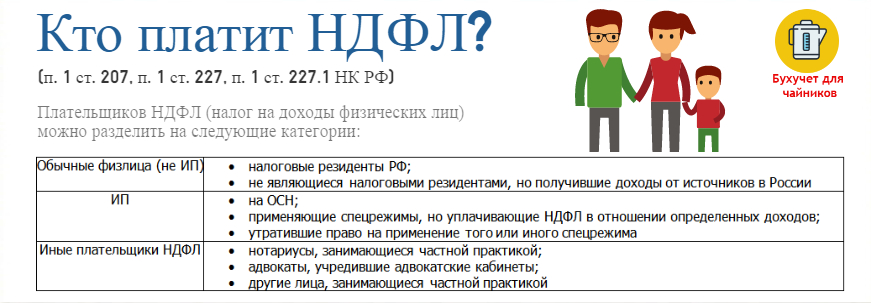

Who should pay tax

One of the main questions of individuals is: “Who should calculate and list personal income tax?”.

In most cases, the tax agent is fully involved in this issue, but this applies only to officially employed citizens. Who arrives for them as a tax agent? These are enterprises and individual entrepreneurs who pay their employees wages and other accruals.

The remaining categories of personal income tax payers pay taxes themselves, they include:

- Individual entrepreneurs.

- Lawyers, notaries and other individuals engaged in private practice.

- Citizens who received remuneration not from tax agents.

- Individuals who profit after the sale of property.

- Residents of the Russian Federation receiving income from sources issued outside the borders of the Russian Federation.

- Citizens from whose income the tax agent could not deduct personal income tax.

- Persons who win the lottery and other risky games.

- Heirs of authors and inventors, receiving income in the form of remuneration.

- Individuals who have received profits by donation.

Tax return

The categories of citizens listed above must rigorously declare their own income. This is done by filling out and submitting a tax return in the form of 3-NDFL.

Reporting in the form of 3-NDFL (see below for how to fill out) is necessary to the Tax Service branch at the place of residence or place of stay within the time frame approved by the Legislation, or rather, no later than April 30, 2018.

The procedure for filing a 3-personal income tax return in 2018

According to the Legislation, reporting in the form of 3-NDFL can be completed in two ways:

- On paper.

- Electronic.

There are several options for sending documents to the tax office:

- Hand over in person or through an authorized person to the tax office at the place of registration.

- Send by mail with delivery receipt and inventory.

- Send via telecommunication channels.

When filling out a document by hand, you can use only black and blue ink, the presence of corrections and blots in the declaration is unacceptable.

How to fill out 3-personal income tax: changes

In 2018, the declaration form has undergone some changes, the new edition sets out the following:

- Chapter 2 - Calculation of the tax base and the amount of tax on profits taxed at a rate of 001%.

- Page "B" - Profit from sources registered abroad, taxed at a rate of 001%.

- Page "D2" - Calculation of property tax withholdings on income from the sale of property.

- Page "E1" - Calculation of standard and social tax deductions.

- Page "E2" ”- Calculation of social tax deductions.

- Page "G" - Calculation of professional tax deductions.

As you can see, there have been no fundamental changes in the document - some pages have been swapped or combined into one, a paragraph has been added that helps the tax inspector understand that the applicant is a pensioner and more.

To which budget is personal income tax paid

And the last question asked by both employees of the financial department and individuals themselves, in which budget to transfer personal income tax, that is, is it a regional or federal tax?

In article 13 of the Tax Code of the Russian Federation is a closed register of federal taxes and fees, where the personal income tax is indicated. Accordingly, personal income tax is considered federal.