The closure of any organization is considered to be a difficult event, involving the liquidation of the company, for which it is necessary to properly notify various public services about the planned process, as well as to pay off debts. When performing this process, it is required to generate numerous documents. At the final stage of the liquidation of the enterprise, the final liquidation balance sheet is drawn up. It contains all the information about the assets of the company, and in addition it needs to be registered with the Federal Tax Service.

Document concept

The final liquidation balance is represented by the standard balance sheet formed by the company at the liquidation stage. The main purpose of this document is the determination of all assets available to the enterprise, which allows you to evaluate its property status.

The liquidation balance may be intermediate or final. In the second case, documentation is compiled after all debts of the company to contractors, government agencies or employees are fully repaid. It includes data on all the assets of the company that remained with the managers after paying off the debt. All these values are distributed among all participants of the company.

When drawing up such a balance sheet, it is not allowed that the size of the assets be greater than the data contained in the interim document. Otherwise, employees of the Federal Tax Service may demand clarification or refuse to close the company altogether. Only under such conditions can all unscrupulous entrepreneurs who want to close the company to avoid liability or to temporarily withdraw assets without selling them to pay off debts be identified.

Legislative regulation

The final liquidation balance sheet of an LLC or other company is required to be drawn up during the liquidation procedure based on legal requirements. The basic information about how the document is prepared and the company is closed is contained in the Federal Law No. 127 “On Bankruptcy”.

Additionally, a lot of information is available in the Civil Code and Federal Law No. 208. These legislative acts stipulate that when drawing up the final liquidation balance sheet, it is required to take into account only those assets that remain after the repayment of all debts the company has. Therefore, all requirements contained in a special register of creditors are satisfied in advance by the company.

If an intermediate balance is formed, then it includes not only all the property owned by the organization, but also the existing obligations to various creditors.

Could it be null?

Quite often, companies create a zero liquidation balance, because after the sale of assets and the repayment of debts, the company simply does not have any assets that could be distributed among all participants in the enterprise.

The law does not provide accurate information on whether such a balance is always zero, since the availability of property after repayment of debts is determined only by the number of different obligations of the organization.

Making a zero balance is easy enough, so the accountant does not have difficulties with this work. Also, it will not be necessary to decide how the remaining property will be distributed among the founders.

Moreover, the final liquidation balance sheet cannot be negative. This is due to the fact that under such conditions, debt remains to other creditors.In such a situation, the tax inspectorate cannot enter information on the liquidation of the company into the register, therefore, the bankruptcy process will have to begin.

Compilation rules

The closing procedure of any company must be carried out in the correct sequence of actions, otherwise it will not be possible to quickly liquidate the company. Therefore, employees of the tax inspectorate are initially notified that the founders of the enterprise decide to close the company for any reason. In addition, such information is published in open sources, which makes it possible to notify all creditors of the closure of the company, so they can timely submit claims to the debtor.

For the proper liquidation of the company creates a special liquidation commission, and the rules for its formation are described in Art. 61-64 GK. It is the members of this commission that are involved in the preparation of the liquidation balance sheet. It may be intermediate or final, but in any case, certain important information is included in it. These include:

- Requisites. This should include the date the document was drawn up and its name.

- Information about the company. The name of the organization and its legal address are given. The TIN and OKPO number is entered, and the main type of activity of the enterprise should also be prescribed. The working part of the balance sheet is represented by a table where information should be entered in separate rows and columns.

- Fixed assets. They are represented by fixed assets, which include various structures, equipment or other expensive and capital facilities. Additionally, this includes tangible and intangible search objects and financial investments, which are investments in securities, other companies or bonds.

- Current assets. This section contains data on receivables and inventories represented by materials or raw materials for the production of various goods. Additionally included is the money held in bank accounts. This section includes financial investments or VAT on purchased property, which may be deductible.

- Capital and reserves. This section allows you to determine the value of the share capital. Additionally included is the amount of reserve capital that each large company should have. The number of shares repurchased by the company from the founders is given. The retained earnings and other property belonging to the enterprise are assigned to this section.

- Long-term and short-term obligations. This includes various installments and payables, for which the due date can vary significantly.

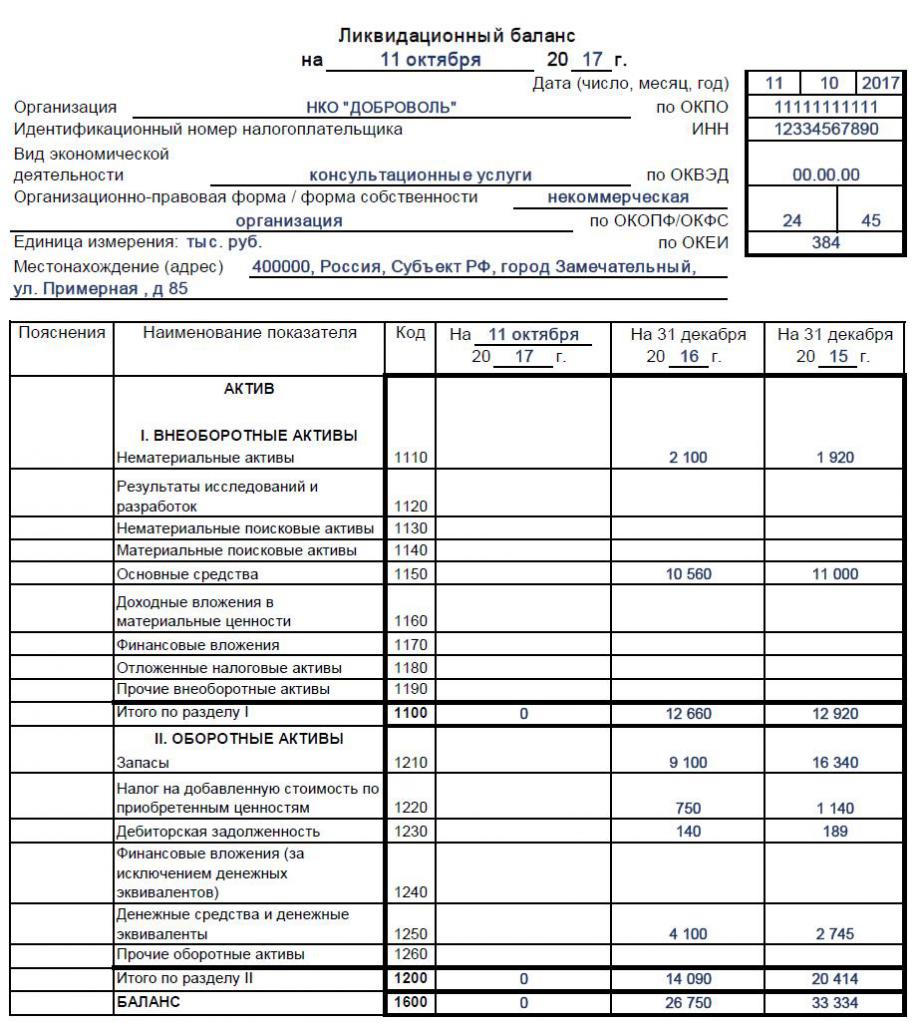

At the end of the table should be information about what is the residual value of all the property owned by the company. The result of the final liquidation balance is zero or a positive value, therefore a negative indicator is not allowed. If a final balance sheet is drawn up, then all available assets are then subject to distribution among participants. If all graphs have a zero, then a zero balance is obtained, which is very easy for an accountant to work with. A sample of filling the liquidation balance sheet can be found below.

What form is used?

It is the liquidation commission that should be involved in drawing up the final balance sheet, but in fact, the employees of the company's accounting department are actively involved in this process.

There is no specific and strictly approved form of the liquidation balance sheet; therefore, it is formed on the basis of the standard form of balance sheet No. 1. It is this form that is used in the preparation of reports for different periods of time, presented by year or quarter.

Members of the commission may add different lines or points to the form of the final liquidation balance sheet, if necessary.In this case, specialists usually adhere to the same rules that are used in the preparation of standard reporting. Be sure to include information in the final balance sheet:

- the carrying amount of assets remaining after all liabilities of the company to numerous creditors have been fully repaid;

- the period for which the document is compiled;

- actual information about the direct company;

- in the section intended for liabilities, all obligations should already be absent, as they should be paid off before reporting;

- the final part of the document should be presented with data on the chairman of the liquidation commission, and he also puts his signature here with a transcript.

If the above information is not available in the document, then it may not be accepted by the tax inspectorate, so members of the commission should be responsible for reporting. After the formation of the document, the final liquidation balance sheet is approved, and the process is carried out by the persons who initiated the liquidation of the company. Typically, the procedure is implemented by a meeting of the founders of the company. To do this, a protocol is drawn up, and the balance sheet marks its presence.

On the basis of what data is entered into the document?

For the correct balance sheet, the commission members must have up-to-date and correct information. Therefore, sequential actions should initially be performed:

- all obligations of the enterprise to creditors are repaid;

- funds are transferred to various state bodies for workers;

- enterprise taxes are paid;

- a property inventory is conducted to identify how many assets the company has;

- if necessary, various objects are sold at auction, after which the funds received from the process are sent to pay off debts;

- only after performing all the above actions is the final balance formed.

By creating this document, founders can see how many assets are left. The book value reflects the book value of assets, so you can understand how much each participant will receive. All property is distributed among the founders on the basis of their share in the company.

Is it possible to create a simplified balance?

If the company is small, and also used simplified taxation regimes during work, then it is allowed to use it with a special simplified form of balance sheet, which is prescribed in the Order of the Ministry of Finance No. 66n.

It is not allowed to use these documents to companies that are subject to a statutory audit, as they must pass a full balance to the auditors. The simplified form is not applied in a situation when it is necessary to display any specific data in the document, since the inclusion of various additional rows or columns is not provided for in the simplified version of the documentation.

Individual entrepreneurs in simplified regimes do not hand over complicated financial statements to the Federal Tax Service at all, so they do not have to draw up a liquidation balance sheet.

The simplified form contains a small number of different points, so there is a tight balance. It combines assets and liabilities, and also includes data for three years of the company. As a result, only the approximate cost of the assets available in the company is shown. Such a document is signed by the head of the organization.

How is the liquidation balance closed?

All property contained in the final balance sheet is to be distributed among the participants in the enterprise. This event should be correctly reflected by the accounting staff, for which the following transactions are used:

- D80 K75.2 - the division of all assets between the founders of the company.

- D75.2 K51 - transfer of payments to the owners of the company.

- D75.2 K01 - transfer of property to the founders.

The direct transfer of values is carried out by drawing up a special act.

Deadline

The legislation establishes the deadline for the balance sheet, and the interim form must be submitted 2 months after publication in official sources about the start of the liquidation of the company. All creditors must be notified in advance of the planned event so that they can present the requirements of the company. The publication indicates the date when the acceptance of claims will be completed.

The deadline for the completion of the balance, which is final, depends on how quickly the company can repay all existing debts. If all debts are repaid, then this documentation may be generated. At the same time, you cannot make any mistakes in the document, since under such conditions the balance sheet and the application for closing the company will not be accepted by the Federal Tax Service. Therefore, before drafting documents, one should carefully assess the property status of the company and make sure that there are no debts.

Conclusion

Before liquidation, each company must perform certain actions, represented by paying off debts and distributing the remaining property between the participants in the enterprise. For this, an intermediate and final liquidation balance sheet is formed. Company employees should be well versed in the rules for compiling this documentation.

When the company uses simplified taxation regimes, it is allowed to use a simplified form of balance sheet, which will not be difficult to compose. It is not allowed to make mistakes when filling out the document, as this may lead to refusal to close the company by the Federal Tax Service.