Dismissal is the end of an employment relationship between an employee and an employer. As a result of this action, the employee ceases to fulfill his duties in the organization, and the employer ceases to pay the labor to the resigned employee, the employment contract is terminated.

Relations and the procedure for their termination (dismissal) between the employee and the employer are defined in the Law "On Employment in the Russian Federation" and the Labor Code of the Russian Federation.

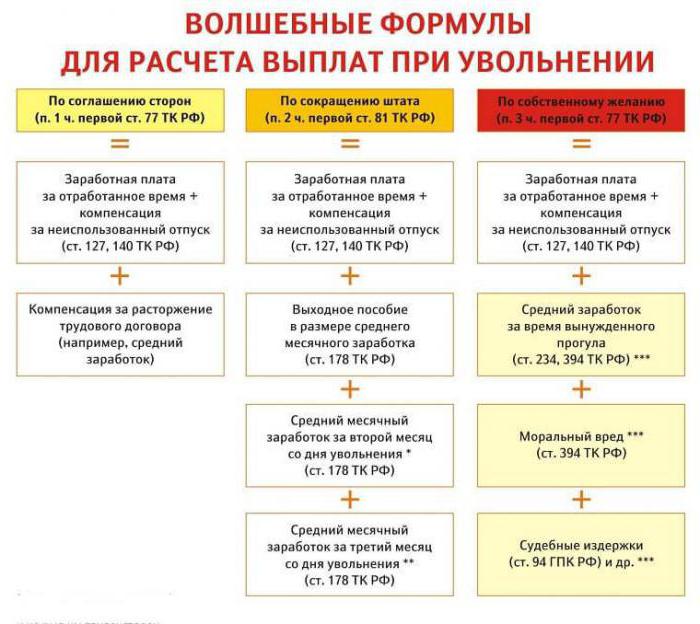

Labor legislation provides for the following main reasons for dismissal:

- The initiator is the employee (dismissal of his own free will).

- The initiator is the employer (dismissal for non-compliance with the requirements of the employer, liquidation of the enterprise, downsizing, etc.).

- By general decision of the employee and employer (by agreement of the parties).

The procedure for dismissal and the final settlement of the employee with the employer depends on the reasons for termination of the employment contract.

Dismissal: how is it made out

Termination of employment with an employee is possible only if there are documents confirming the basis for the dismissal procedure:

- Employee application (dismissal by own decision).

- The agreement between the employee and the employer, if the dismissal occurs by mutual agreement.

- Notification of termination of employment if the deadline for concluding a fixed-term contract has expired.

Further, the employer must:

- Issue an order to dismiss an employee, it must indicate the date and reason.

- To order to issue a note-calculation indicating the number of days of unused vacation and all payments due in the final calculation.

- Make the necessary entries in the workbook of the resigning employee.

- Issue a work book.

- Settle with a retiring employee.

- Issue certificates 2NDFL, 182n, SZVM-STAZH.

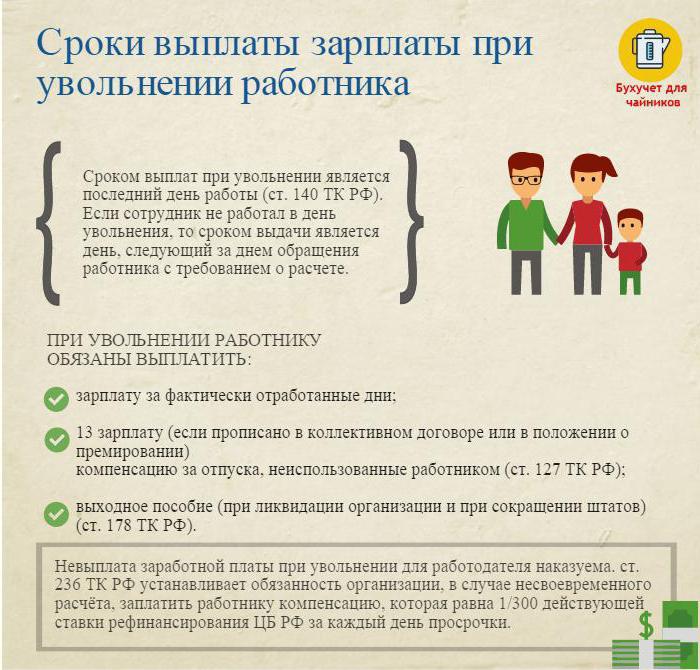

Dismissal: final settlement

On the last business day (day of dismissal), it is necessary to draw up a final payment and pay all the amounts due to the employee.

Typically, these are:

- Salary (salary, bonuses, allowances, bonuses for combining, etc.) accrued for the time worked.

- Compensation of leave upon dismissal (personal income tax is taxed).

- Compensation payments on the basis of dismissal.

Compensation payments on the basis of dismissal include:

- Severance pay reduction.

- Severance pay for retirement on disability.

- The allowance for staff reductions during the search for a new job.

- Compensation to the head, his deputies, chief accountant upon termination of the employment contract.

On the day of dismissal, it is necessary to transfer the entire accrued amount minus the income tax (calculated according to the Tax Code of the Russian Federation) to the employee’s personal account or to issue it at the cash desk of the enterprise.

The employer has no right to delay the payment (even if the bypass list is not signed).

Dismissal: personal income tax

The accountant of the company with all amounts due accrues and withholds personal income tax upon dismissal.

Personal income tax is levied on:

- Salary (bonuses, allowances, payment by tariff or salary, surcharges for substitution and the like).

- Compensation for days of unused vacation.

Attention:

- Compensations related to dismissal and provided for by a labor or collective agreement are not subject to personal income tax if they do not exceed three times the average monthly salary (for workers in the Far North and equivalent regions - six times).

- Amounts exceeding three times (six times) the amount of average monthly earnings are taxed in the prescribed manner.

- This procedure for withholding personal income tax is common to all, does not depend on the position of the resigning employee.

Important: withholding personal income tax upon dismissal must be paid to the budget no later than the day following the day of dismissal (final settlement).

Dismissal: certificate 2 personal income tax

After all the necessary calculations, a personal income tax certificate is issued upon dismissal. It reflects all the accruals of the current calendar year for months taxed by income tax. In reference 2 personal income tax upon dismissal should be taken into account the accrual of the final calculation. They are reflected as follows:

- salary with code 2000;

- Prizes with code 2002;

- compensation for unused vacation - 4800;

- compensation payments in the amount of exceeding three (six) average monthly earnings - 4800;

Certificates 2 of personal income tax on dismissed submitted to the IFTS at the end of the calendar year.

Making 6 personal income tax upon dismissal

The employer on the day of dismissal makes the final calculation with the dismissed. This event is reflected in the report in the form of 6 personal income tax as follows.

The second section of the report records:

- line 100 - the day of the final payment with the employee (ideally, the day of dismissal);

- line 110 - the date of calculation (withholding) of income tax (coincides with the date on line 100);

- line 120 is the date following the tax withholding day (the day that follows the day of dismissal).

In the report 6 personal income tax lists only the income from which income tax is levied. Compensation payments from which personal income tax is not withheld are not reflected in the report.

Example: Ivanov I.I. Dismissed on April 26th. On the day of dismissal he was charged:

30000 rub. - salary payment for days worked in April.

10,000 rub. - compensation for unused vacation.

15,000 rub. - severance pay (not subject to income tax).

The income tax withheld at the rate of 13% - (30,000 + 10,000) * 13% = 5200 rubles was withheld from the accrued amounts.

On the hands of Ivanov I.I. received (30,000 + 10,000 + 15,000) -5200 = 49,800 rubles.

In the form of 6 personal income tax is reflected as follows:

Line 100 - 04/26/2017, line 130 - 40,000 rubles.

Line 110 - 04/26/2017, line 140 - 5200 rub.

Line 120 - 04/27/2017.

Difficult cases upon dismissal

Some interesting cases from practice that cause difficulties in dismissing an employee:

1. Dismissal on the last day of the quarterly month. How to reflect it in the form of 6 personal income tax?

Example: Ivanov I.I. quits March 31 (the last day of the first quarter). On the day of dismissal, he was accrued the final payment of -30000 rubles., Withheld personal income tax - 3900 rubles.

This operation is reflected in the report of the second quarter, since the deadline for the transfer of personal income tax is April 1 (second quarter):

Line 100 - 03/31/2017, p. 130 - 30,000 rubles.

Line 110 - 03/31/2017, p. 140 - 3900 rub.

Line 120 - 04/01/2017.

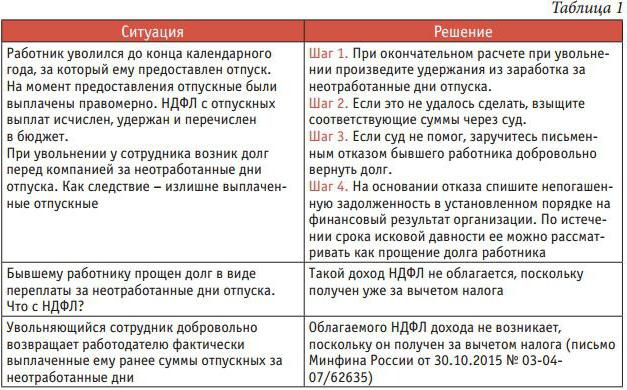

2. The employee resigned in December 2016, and in February 2017 he was late paid compensation for unused vacation. In which tax period should the amount paid be shown?

The amount of income and withholding income tax should be indicated in certificate 2 of personal income tax for 2017.

3. The employee is granted leave from 04/11/2017 with subsequent dismissal. He received the final payments on 10.04.2017. How to reflect in the form of 6 personal income tax?

April 10, 2017 vacation pay - 10,000 rubles. and wages for hours worked - 20,000 rubles. Income tax has been deducted from these amounts.

In the report 6 personal income tax for the second quarter, this operation is displayed as follows:

1. For vacation pay:

Page 100 - 04/10/2017, p. 130 - 10,000 rubles.

Page 110 - 04/10/2017, p. 140 - 1300 rub.

Page 120 - 04/30/2017.

2. For the final payroll calculation:

Page 100 - 04/10/2017, p. 130 - 20,000 rubles.

Page 110 - 04/10/2017, p. 140 - 2,600 rubles.

Page 120 - 04/11/2017.

As you can see, there are a lot of nuances when filling out Form 6 personal income tax and 2 personal income tax. Particular care must be taken when firing employees. We hope that some of the tips given in this article will facilitate the work of the accountant and personnel officer.