A statement of cash flows is a document that clearly reflects the structure of cash flow receipts and expenditures. These data allow you to monitor the development of the enterprise and visualize its future potential. This is made possible through the demonstration of capital in a document in three directions - current activities, investments and investments. Next, we will discuss how to fill out a cash flow statement.

General information

The form of the document was adopted in 2010 by order No. 66 of the Ministry of Finance. Almost all enterprises engaged in commercial activities are required to fill it, with the exception of:

- Government organizations.

- Insurance companies.

- Credit companies.

The information recorded in the document is of great importance both for the management of the enterprise, and for other involved entities. These include: co-owners, investors, creditors and other persons. Analysis of the cash flow statement in form 4 makes it possible to examine in detail the movement of cash flows of the company.

The report is generated annually and submitted to the control authorities.

Document structure

The entire amount of information in the document is divided into several blocks by type of activity:

- The main one.

- Investment.

- Financial.

Using this method allows you to demonstrate the true financial picture in each of the areas. Separation of each of them in a separate block allows eliminating the situation with concealing the loss ratio for one of the types of activities by summarizing the total cash flow. These areas of analysis create a structure from which a cash flow statement form is subsequently generated.

Primary activity

This section includes all actions leading to income from the implementation of the main activities of the institution. It includes:

- Net profit and loss associated with the mainstream activities.

- Management expenses.

- Payment of wages.

- Costs of commission, interest and income tax.

- Dividends in the statement of cash flows and more.

Investment activities

This includes all long-term operations entailing long-term benefits. Including investments in assets in several areas are taken into account:

- Purchase and / or sale of subsidiaries.

- Acquisition of real estate in order to derive long-term benefits.

- Purchase / sale of non-current assets and funds for the production process.

Financial activities

This chapter of the statement of cash flows contains information on those affecting changes in the volume and structure of a company's net asset and borrowed funds:

- Issue of any type of shares and redemption from their holders.

- Dividends paid.

- Income from the sale of debts.

The posted structure should be regarded as an example of a cash flow statement. Each institution independently describes the level of detail and composition of the report within the framework of the adopted structure. Some items are subject to change. Be careful!

Report Creation Techniques

Not sure how to fill out a cash flow statement? In practice, there are two types of detailed report generation. Each of these methods for creating a document on the movement of the organization’s funds and the procedure for filling out the form are based on the specified structure.

Features of the direct method

Reporting involves the provision of various kinds of information on revenues and expenses that are directly related to the implementation of the main tasks of the enterprise. Information is taken from the following sources:

- Information on profit and loss of the organization and balance sheet.

- Company accounts

The first option is the most common and simple. The second one is rarely used in practice because of its complexity. For this, it is necessary to classify and analyze a very large amount of information.

The process of generating a cash flow statement form for internal accounting is not an easy task. In addition, the process is complicated by restricting access to certain information. This does not allow interested parties to fully evaluate all important aspects.

The disadvantage of this method is the inability to trace the relationship between changes in the total amount of available funds and the monetary result for the desired period.

Before deciding how to fill out a cash flow statement, it is recommended that you understand the nuances of each method. This method has the following advantages:

- An opportunity to trace where the cash flow comes from and where it goes.

- A good understanding of how available funds cover current liabilities.

- Linking the report to the current budget of revenues and expenses.

- Track the relationship between expenses and income.

The material included in the statement of cash flows (an example can be seen in the photo below) is necessary to assess the liquidity of the organization in the context of a long-term analysis. This opportunity opens up through a detailed examination of the movement of funds in three main areas.

Indirect method

This reporting method involves the use of documentation related to the core business.

Thinking about how to fill out a cash flow statement? The principle of constructing a report by an indirect method is the opposite of the previous one. The work consists of the following steps:

- Determination of the size of profit in pure form on the basis of relevant documents

- Addition of net profit and expenses that do not affect the movement of funds.

- Summation and calculation of changes in expenses on current payments, with the exception of the “financial payments” section.

- Compilation and calculation of data on transactions involving short-term obligations that do not involve interest payments.

The information contained in the report shows:

- The relationship between the various areas and activities of the company.

- The relationship between net profit and working capital.

Report Filling Walkthrough

In the financial statements, the cash flow statement, as noted earlier, it is customary to classify all financial movements into three categories: current, cash and investment. Information is entered on the basis of balance sheet data into the subgroup to which each specific transaction belongs.

Current activities

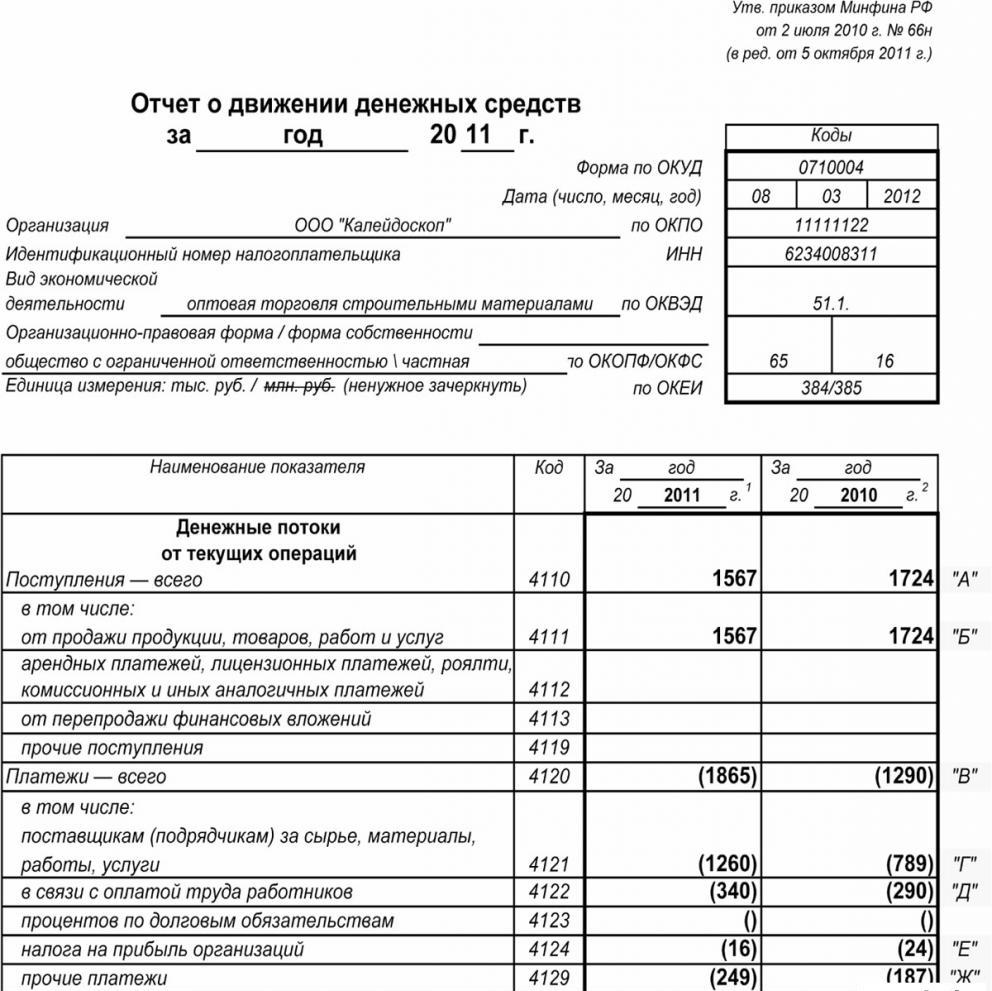

The “cash income from current operations” part includes data responsible for the receipt and expenditure of funds associated with the main activity of the institution. Let's analyze the cash flow statement line by line:

Income:

- rental payments, royalties, fees, commissions and other payments of a similar nature;

- interest on receivables of customers and consumers;

- resale of material investments and so on (including the total balance of value added tax).

Calculations:

- salaries to employees;

- income tax;

- commission on credit and loan obligations (with the exception of those related to the value of investment assets);

- other expenses directly associated with the implementation of the current activities of the institution.

Balance of financial receipts from current activities (profit minus payments).

Parish on current operations.

This indicator in the statement of cash flows is calculated as the result of adding points from 4111 to 4119.

- Paragraph 4110 - Total receipts for a specified period of time.

- Paragraph 4111 - the general accruals of received funds from current operations are entered in this column.

Information is taken from the following debit accounting registers:

- Fiftieth - “Cashier”.

- Fifty-first - "Current Accounts".

- Fifty-second - "Currency accounts."

- Fifty-eighth - Investments.

- Seventy-sixth - “Payments to debtors and creditors”.

These indicators are reflected in the statement of cash flows minus indirect taxes, amounts received by agents, intermediaries, commission agents and transfers received as compensation payments (utility bills, road expenses, and much more).

- Paragraph 4112 - rent, licenses, commissions, royalties.

- Paragraph 4113 - resale of tangible assets.

- Items 4114 through 4118 are optional. In them, the financier can reflect amounts that cannot be clearly classified. These indicators are reproduced according to the same principle that was used in line 4111.

- Paragraph 4119 - other types of income from entrepreneurial activities.

These include the following:

- benefits received from the acquisition / sale of foreign currency;

- a positive balance of VAT settlements;

- repayable funds;

- interest on receivables from customers and customers;

- profit from the sale of other property not directly related to funds placed on the balance sheet of the company.

These figures are reflected similarly to those in line 4111. Indirect taxes received by the enterprise from the budget (for example, reimbursement of value added tax) are entered in the “collapsed” column.

Filling the section on current payments

These components of the cash flow statement are calculated as a set of items from 4121 to 4129. The data for these periods are enclosed in parentheses.

- Paragraph 4120 - General expenses.

- Clause 4121 - Settlement with suppliers.

Information is reflected in the accounting registers for credit of the following accounts:

- Fiftieth - “Cashier”.

- Fifty-first - "Current Accounts".

- Fifty-second - "Currency accounts."

- Fifty-eighth - Investments.

- Seventy-sixth - “Payments to debtors and creditors”.

It is necessary to reproduce this information in the documentation with deduction of indirect taxes, payments to agents, committees and intermediaries, as well as reimbursable expenses for utility bills and transportation.

- Paragraph 4122 - transfer of wages to employees. Information is provided on the same principle as in paragraph 4121.

- Paragraph 4123 - interest on credit and loan agreements.

- Paragraph 4124 - income tax.

- Paragraph 4125 to 4128 - additional columns. At this point, the accountant can indicate values that are difficult to type into other sections of the document. The amounts of these payments are paid in the same way as payments to suppliers and contractors, that is, as specified in paragraph 4121.

- Clause 4129 - the amount of other types of payments associated with the implementation of entrepreneurial activity.

These include:

- damage from the acquisition / sale of currency;

- losses incurred in exchanging banknotes;

- the estimated balance of value added tax with a minus indicator / debt obligations to government bodies;

- penalties paid by the company, penalties and other payments of this kind, under contracts with counterparties.

Do you think that in this block the procedure for compiling a cash flow statement changes? No, all these figures are displayed by the same analogy as the amounts of payments to suppliers and contractors, that is, as in paragraph 4121.

The amount of indirect tax transferred by the enterprise to the budget (for example, value added tax) under this item is displayed in the “collapsed” line.

- Paragraph 4100 - cash flow from current operations. This fits the difference between revenues and expenses from the main activity.Indicator 4110 = paragraph 4110 - paragraph 4120. Upon receipt of a number with a negative indicator, it must be enclosed in parentheses.

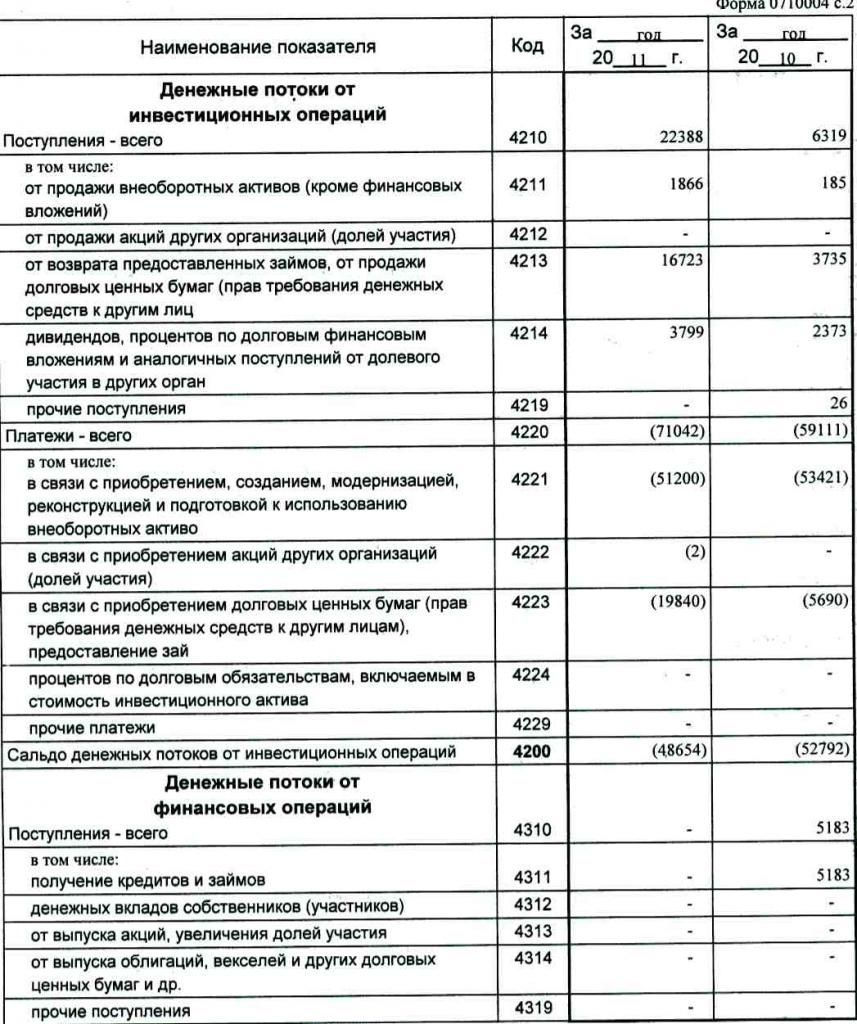

Investment profit

The size of the proceeds from investment operations consists of the indicators reflected in paragraphs 4211 through 4219 of the cash flow statement. Explanation of paragraph 4210 denotes a common parish.

- Paragraph 4211 - non-current assets (other than tangible investments).

This type of parish includes:

- fixed assets of the institution;

- non-financial assets;

- serious investments in non-current assets (for example, unfinished construction);

- R&D results.

Information is contained in the accounting registers for debit of the following accounts: fiftieth - “Cashier”, fifty-first - “Settlement accounts”, fifty-second - “Currency accounts”, fifty-eighth - “Investments”, seventy-sixth - “Payments to debtors and creditors”.

This data should be reflected in the documentation minus indirect taxes, funds paid to agents, committees and intermediaries, as well as reimbursable utility costs and transportation costs.

- Paragraph 4212 - income from the sale of shares or shares in other companies.

- Paragraph 4213 - repayment of interest loans issued earlier, sale of debt receipts and bonds (the amount of interest received is not recorded in the report).

- Paragraph 4214 - interest on debt financial investments and similar proceeds from equity participation in other projects.

- Paragraph 4219 - other transfers that relate to investment activities.

Payment operations for investment projects

The size of payments for investment operations is made up of indicators from paragraph 4221 to 4229. All figures are indicated in rounded brackets.

- Paragraph 4220 is the total amount related to investment payments.

- Paragraph 4221 - purchase, formation, restoration, improvement or preparation for the use of fixed assets. Not sure which accounts are shown in the cash flow statement?

Information is entered in the accounting registers for credit of the following accounts:

- Fiftieth - “Cashier”.

- Fifty-first - "Current Accounts".

- Fifty-second - "Currency accounts."

- Fifty-eighth - Investments.

- Seventy-sixth - “Payments to debtors and creditors”.

It is necessary to reflect this data in the documentation minus indirect taxes, funds transferred to agents, committees and intermediaries, as well as reimbursable expenses for utility and transportation expenses.

- Paragraph 4222 - The acquisition of shares or interests in other companies.

- Paragraph 4223 - the purchase of debt receipts (the right to claim funds from third parties), the issuance of loan loans to other persons.

- Paragraph 4224 - payment of interest on loan obligations included in the amount of an investment asset.

- Paragraph 4229 - other payments.

These include:

- investment income tax;

- amounts invested in joint ventures;

- other payments related to investment activities.

Paragraph 4200 - balance of financial income from investment projects. This column contains the value of the amount that is obtained after deducting expenses from income from investment operations. That is, you must specify the difference.

Wondering how to check a cash flow statement? The seventh indicator on this list is very easy to check: paragraph 4200 = paragraph 4210 - paragraph 4220.

Upon receipt of a negative result, the value must be enclosed in brackets.

Cash transactions

This section of the cash flow statement shows the amounts that were received due to raising funds from financing on a debt or equity basis. Actions of this kind are accompanied by a change in size and structure:

- The material condition of the enterprise.

- Borrowed funds company.

Filling in the income section

The total amount of this value is obtained by adding the columns from 4311 to 4319.

- Paragraph 4310 is a general indicator.

- Paragraph 4311 - obtaining credit or borrowed funds.

- Paragraph 4312 - owners' cash investments.

- Paragraph 4313 - the receipt of funds from the issue of shares or the increase in equity interests.

- Paragraph 4314 - cash flow from promissory notes issued by the company, bond issues and debt receipts.

- Paragraph 4319 - other income.

Cash Transaction Payments

The total amount is calculated as the total indicator from the addition of the values in points 4321 to 4329. All data should be indicated in brackets.

- Paragraph 4320 is a general meaning.

- Clause 4321 - payments to owners upon redemption of their shares or company shares, or due to their withdrawal from the founders.

- Paragraph 4322 - dividends and other payments to owners related to the distribution of profits.

- Paragraph 4323 - repayment / redemption of bills and promissory notes, payments on loans and credit agreements.

- Paragraph 4329 - other payments associated with cash transactions.

- Paragraph 4300 - cash flow from financial transactions. It is calculated according to the following scheme: paragraph 4300 = paragraph 4310 - paragraph 4320. When receiving a result with a minus sign, parentheses should be put.

Conclusion

The preparation and analysis of a cash flow statement in form 4, which presents a detailed picture of the cash flow, in combination with other types of reporting, has a significant role in understanding the real situation of the company. The information contained in the document makes it possible to analyze the current state of affairs, predict future prospects and think about measures to improve efficiency. The choice of reporting method depends on the degree of availability of the required data.