Every year, the global economy is becoming more and more consolidated. Even at times a difficult political situation is not able to restrain this economic process. In recent years, many enterprises representing foreign holdings have appeared on the territory of Russia. Their number is growing. To simplify accounting in such enterprises, the possibilities of simplified economic integration are used and IFRS standards. Gradually they supplant PBUs familiar to Russian specialists.

What is IFRS

IFRS is a set of accounting standards developed by a special international council.

The number of countries that have adopted these standards in various forms (for some countries - as recommendations, for some - legislatively) has long exceeded a hundred. Obviously, the use of common standards greatly simplifies the interaction between organizations of different countries. Transparency, predictability, clear certainty of financial results favorably affect the investment climate of different countries. The transfer of information, the exchange of it is also simplified.

IFRS reporting: forms and basis for their formation

International standards cover almost all areas of accounting. Regulated and the process of tax assessment, and cash flows, and accounting for fixed assets and much more. IFRS reporting forms are also diverse.

All types of forms that are included in the IFRS reporting kit are governed by the very first standard - “Financial Reporting”. According to the eighth paragraph of this standard, this kit includes:

- Firstly, balance sheet is the main form of financial statements in IFRS, as, indeed, in Russian accounting.

- Profit and loss statement IFRS. What could be more important for an organization than financial performance? This form just analyzes the profit or loss of the organization.

- A report that reflects the movement of equity.

- Report on financial flows.

- A brief analysis of accounting policies.

Some of these forms are governed by separate standards. Reporting periods can be both long (364 days) and short (quarter). In preparing IFRS financial statements, the principles of completeness, truthfulness, and timeliness play an important role. One of the most important reports is the profit and loss statement of IFRS, there is no separate standard for it, therefore, information on its preparation has to be collected from several standards.

IFRS Financial Results Report: General Description

The income statement IFRS characterizes these indicators in more detail than its Russian counterpart.

According to standards, the report form should fully disclose the following information:

- income from sales of the enterprise (as well as other income directly related to the main activity of the enterprise);

- results of current activities of the organization;

- the percentage of financial indicators that are associated with the main activity, as well as from the business in which the company participates through equity participation;

- income tax amount;

- economic indicators of the enterprise from the main business;

- direct economic results of the organization.

The items listed above do not exhaust all the information that must be indicated in the income statement of IFRS. It can be said that this is the bulk of the information.

How to make a report

An accountant whose task is to generate a statement of profit and loss in accordance with IFRS should clearly determine the algorithm of actions, something like this:

- First of all, it is necessary to collect comprehensive information about all expenses and income of the organization for the analyzed period. Here the 1C program comes to the rescue. The analyzed period should be closed.

- The second step in the preparation of the report is the division of income and expenses into groups. The developers partially leave the classification of income and expenses to the choice of an accountant, since in practice it is impossible to draw up one classification for all types of activities. For income, the grouping may include: income from the main business, other, differences in exchange rates and other large income groups. Groups of expenses, for example: expenses related to the prime cost (materials, salaries, transportation and procurement expenses, etc.), investments, expenses for taxes, other, and so on.

- To analyze the correctness of the reflection of information in the program 1C, adjust the wiring in the presence of errors.

- Make a profit and loss statement in IFRS, calculating the necessary indicators from the source data.

Report Submission Form

Strictly speaking, the profit and loss account form does not exist in IFRS. Standards govern only the general requirements for the report, which form the main fields of the form. The indispensable assistant for this is the Excel program. As a basis for the development of this form, you can take the profit and loss statement form approved by order of the Ministry of Finance. It should be remembered that in accordance with IFRS, the income statement contains more information. The simplest form of financial results looks like this:

The form is basic, it is desirable to detail the costs depending on the specifics of the enterprise.

Examples of detailing expenses in the form of financial results

If you need more detail, you can disclose the cost of sales by indicating direct and indirect costs. You can go further into detailing by expanding direct costs into expense items. In this case, the line "cost of sales" will be replaced, for example, with the following lines:

- salaries of employees;

- social deductions from wages;

- material costs;

- transportation and procurement costs;

- indirect costs.

If you detail the indirect costs, the corresponding line will expand into several:

- travel expenses;

- depreciation;

- taxes attributable to cost of sales;

- security expenses;

- expenses for cash settlement services;

- advertising costs.

Financing costs can also be described in more detail. For example, such articles:

- commission for servicing a current account;

- interest on the use of loans;

- difference in exchange rates (negative).

As can be seen from the example, the compilation of the profit and loss statement form IFRS is an individual case of each enterprise. Consider an example.

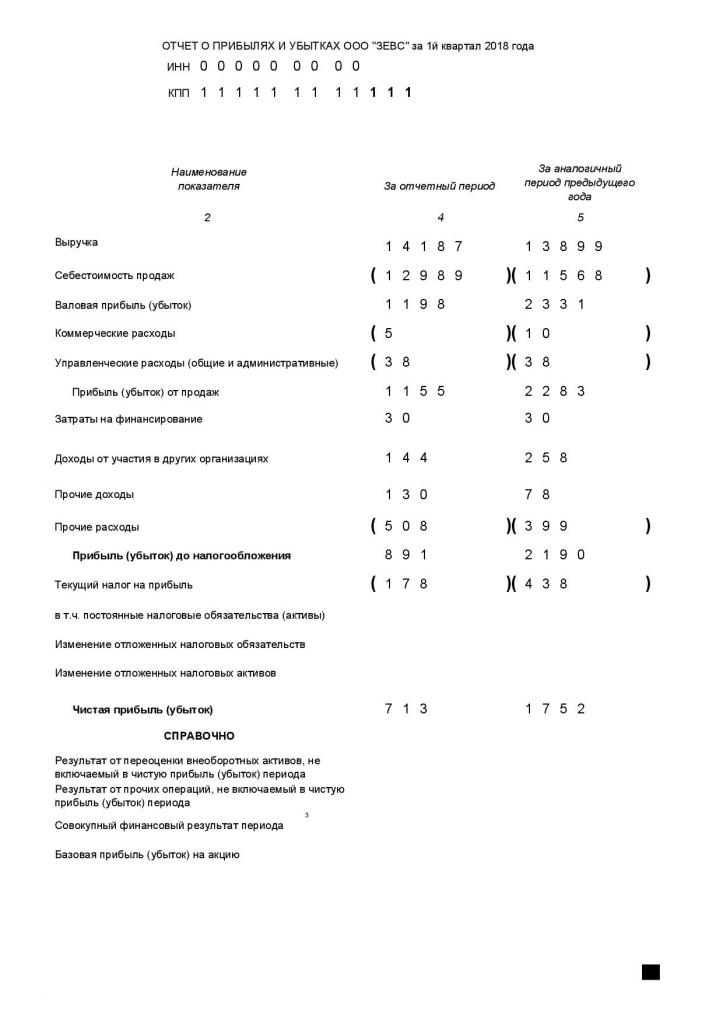

Profit and loss statement example IFRS

The need for global analysis based on the profit and loss statement is seen in the example:

It is clearly seen that ZEVS LLC in the first quarter of the reporting year worked worse than in the same period of the previous year. If you detail the costs according to the principle above, the enterprise management will identify items of expenses that require close attention and adjustment.

Differences between RAS and IFRS

In Russia, accounting is largely regulated by the PBU - accounting provisions. IFRS and RAS are for slightly different purposes. The former regulates reporting, the latter - accounting.

However, when applied to one area of accounting, some fundamental differences become apparent:

- in PBU there is no such thing as “professional judgment”, in IFRS it is very common;

- Tough PBU is tied to the documentary justification of facts of economic activity, IFRS takes into account primarily their economic content;

- differences in accounting approaches to RAS and IFRS;

- other differences.

At the state level, the differences are trying to smooth out.

The development of IFRS in Russia

All developed countries are interested in consolidating the accounting report. The Russian Federation is no exception. The decision to improve Russian accounting was made at the government level in the last century, and more precisely in 1998. However, only since 2010, the process has intensified. Using the orders of the Ministry of Finance, federal laws, the introduction of new PBUs, the government in every way encourages managers of organizations to comply with IFRS standards in accounting. Such efforts are yielding results: today, about eighty percent of organizations in Russia use international standards in their activities. The orderliness, clarity, transparency brought about by the use of standards undoubtedly leads to an increase in the profits of companies.

If you compile the profit and loss statement of IFRS correctly and reliably, it will become one of the starting points for conducting an economic analysis of the enterprise’s activities by management. The analysis, in turn, will help to correctly identify leverage on the organization with the goal of changing the financial results of the enterprise in a more favorable direction.