Those who at least once took a loan from a bank know that this is a complex process. Bank employees carefully check the documentation and solvency of each client. At the same time, when applying for a loan or a loan, Sberbank customers are invited to issue an insurance policy. When you make small consumer loans, the size of insurance from the total amount can be up to 30%, increasing it quite a lot. Moreover, not everyone knows that insurance is a voluntary matter, and they do not always draw up a refusal of insurance after receiving a loan.

All the benefits of insurance

First of all, insurance is necessary for the bank itself, which insures its risks that may arise if the borrower loses its working capacity.

Different types of loans have been developed with different insurance policies. For example, consumer loans insure against loss of life, health, work. Mortgage: health, loss of work, property, title, life. Car loans: life, health, hull insurance, job loss. For example, if a client obtained a consumer loan and died, or lost working capacity, or fell under a job cut, the insurance company repays the rest of the loan. The amount of payments depends on the designed program. As a rule, the insurance company fully repays the remaining amount, sometimes a partial payment is made. If lending was made on the security of property, then in case of systematic defaults, the bank withdraws a car or an apartment from the borrower (which was on the security). In order to maintain the market value of the property (after an accident or accident, insurance covers the repair of an apartment or car) and maintain the property in its original form, an insurance policy is issued.

Is insurance required when taking a loan?

The issuance of a loan, weighed down by some type of insurance, is considered illegal. It is strictly forbidden to provide one service, while imposing another. Thus, refusal of insurance after receiving a loan does not contradict the law.

If the borrower nevertheless concluded such an agreement, he has the right to terminate this agreement by paying the expenses incurred by the bank.

Article 935 of the Civil Code of Russia contains similar provisions, and it is illegal to force a borrower to insure.

Is the insurance service legal?

It is very important to remember that insurance is an illegal service. And each lender can apply for a waiver of insurance after receiving a loan.

The existing legislation governing the provision of financial services does not require obligatory insurance of borrowers. However, banks that provide lending services prefer to remain silent about this.

An exception to this rule is mortgage lending. And the borrower's responsibilities include compulsory insurance at his own expense for collateral against various damages, this provision is enshrined in the law on mortgages.

How is insurance imposed on the contract?

Sberbank, like other banks, imposes voluntary insurance on a loan agreement by the following methods:

- Between a bank and one of the insurance companies, as a rule, an agreement is concluded on collective voluntary insurance of borrowers. If, upon signing the loan agreement, the borrower signs this collective insurance agreement, he automatically joins it. In this case, a copy of the insurance policy is issued to him.

- Since the loan agreement does not contain requirements for compulsory insurance, bank employees offer to conclude a separate insurance agreement proposed by one of the insurance companies.

Criteria for imposing a service

Based on judicial practice, in one of its reviews the Supreme Court of the Russian Federation outlined clear criteria for the imposed service. A service will be considered imposed under the following conditions:

- If the loan agreement contains clauses obliging the borrower to insure, then this is a condition for obtaining a loan.

- The bank's requirements in the contract that are presented to the borrower for insurance with the insurance company indicated by the bank in compliance with the conditions also proposed by the bank.

In other cases, the client can give up insurance after receiving a loan from Sberbank. It is very common practice when the borrower is not given the insurance contract and insurance conditions in his hands, they offer, without studying it, to sign in the column on familiarization with the insurance program. In this case, the chance to challenge the imposed contract in court is minimal. Therefore, we strongly recommend that you study the terms of the contracts before signing anything and require a certified copy.

How to refuse insurance?

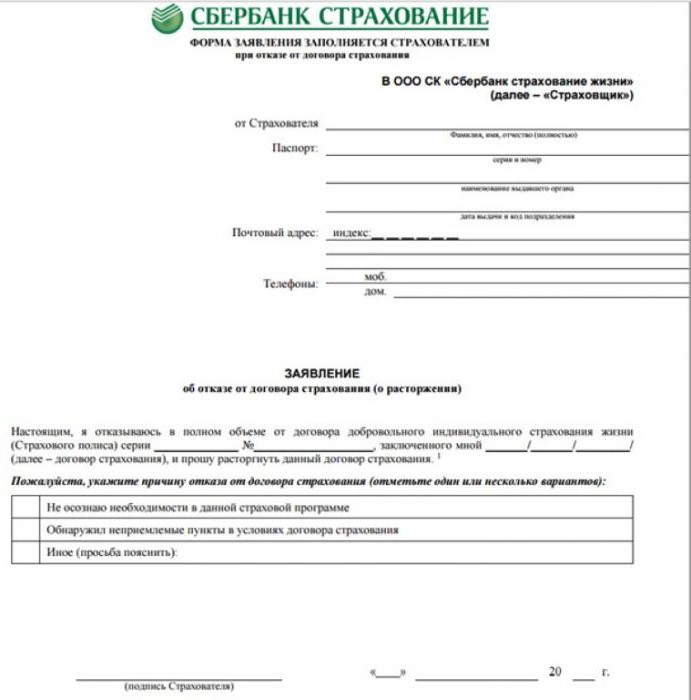

Since the insurance amount is quite substantial, the borrower does not have the funds to pay it, Sberbank offers to issue them also on credit, thereby increasing the loan amount. The result is a significant increase in loan payments, and in addition, the borrower pays interest to the bank for the funds paid for insurance. If the borrower refuses insurance, the bank must provide a sample of refusal of insurance after receiving a loan.

Refusal to conclude a contract

The conclusion of a loan agreement, as well as insurance, is voluntary. The borrower always has a choice. Whether to conclude an agreement with Sberbank or another bank that does not require insurance, or choose an alternative lending program. By the way, such programs have higher interest rates.

It is worth weighing the pros and cons, applying for a cancellation of insurance after receiving a loan from Sberbank, and drawing up a contract at a higher rate. Or still get an insurance policy.

Return insurance after a loan paid

Fearing that Sberbank or another bank will refuse to issue a loan, the borrower often agrees to insurance. It should be recalled that in this case, the borrower has the right to issue a refusal after he received a loan. It is also possible to return funds for insurance after the loan has been repaid.

Since insurance is the same product as other services, a citizen who has concluded an agreement has the right to terminate it ahead of schedule without giving any reason within 30 days from the date of its conclusion. To do this, you need to fill out an application to refuse insurance after receiving a loan.

Sberbank is the most democratic in this matter, allowing its customers to fully return money for insurance for up to 30 days after lending. After a month, the borrower will be able to return only part of the funds that went to insurance, or rather, about half, since the bank will retain the amount of its expenses from this amount.

Based on the current legislation of the Russian Federation and taking into account the conditions of most insurance programs for Sberbank borrowers, the borrower has the right to refuse insurance after receiving a loan from Sberbank. To this end, he must, within a month (30 days) in the name of the head of the department in which the loan was issued, write a request in arbitrary form with a request to terminate the voluntary insurance contract.

The borrower will be able to count on the return of 50% of the amount of the contribution for participation in voluntary insurance after 30 days, but no later than 90 days.The remaining amount will be used to reimburse the bank for the amounts spent on connecting the client to the insurance program and paying taxes by the bank.

I must say that giving customers the opportunity to understand in detail, calculate and think through all insurance conditions, and if necessary, freely return the money spent on it (it is granted to refuse bank insurance after receiving a loan for 5 days), Sberbank significantly increases its confidence, increasing the chance that the client, after weighing and calculating all the risks, will leave the insurance contract in effect.

Those who decide to return insurance should carefully study their loan agreement. In the event that it does not provide for the possibility to return the insurance amount, a claim should be submitted to the bank. However, in most cases this will have to go to court.

Loan repayment ahead of schedule

Some bona fide borrowers are trying to quickly pay off the loan, and taking it, for example, for a year, repay it ahead of schedule, paying for six months. After trying to return unused insurance. However, a person must know that he is not entitled to demand a refund of the insurance premium paid. Article 958 of the Civil Code of the Russian Federation provides for borrowers who repayed a loan ahead of schedule, early cancellation of the insurance contract. However, there are limitations.

Important! In the case when the loan is repaid ahead of schedule and a refusal is made out of life insurance after receiving a loan, insurance premiums are not returned.

Analyzing the results of lawsuits on this topic, we conclude that the courts consider insurance contracts as an independent service that does not stop after the policyholder fulfills obligations under the loan agreement. His cancellation of the contract in connection with the repayment of the loan does not indicate the termination of insurance risks. So the courts find no reason to pay insurance premiums paid at the conclusion of the contract.

Going to court

In the event that the bank does not meet you, and the terms of the contract do not provide for the return of insurance, which, as you are sure, was illegally imposed on you, you should contact the court. The imposition by banks of additional services, such as insurance, is a violation of consumer rights, Rospotrebnadzor and FAS have repeatedly spoken about this. In case of refusal of bank insurance after receiving a loan, you should be sure that the court will stand up for you and the funds spent on insurance will be returned to you.

If the borrower did not have the right to choose when signing the contract, this will give the bank an advantage. To be sure of your chances, before applying to the court, you should conduct a legal examination of the loan agreement to assess the risks of the consumer and thoroughly work out the evidence base.

Including it is worth getting a refusal from the bank in writing about the return of insurance.

How important is insurance, is it worth giving up on it?

The mentality of Russian citizens is based on the Russian “maybe” in matters of health, property, life insurance, etc. Acquiring insurance, our citizens consider it an expensive pleasure, rarely thinking about the possible risks and consequences that come with them.

Our life is unpredictable, and no one is given to know what could happen to you or your relatives in a year. But if force majeure or an insured event does occur, the insurance company will pay the due amount. And with this she will provide you and your relatives with substantial financial assistance. Nevertheless, the number of refusals from insurance after receiving a loan in 2016 increased.

Arbitrage practice

You should not be afraid that banks with large sums of money will close your lawsuit without trial. In approximately 80% of cases, courts decide on payments in favor of borrowers by ordering the borrower's bank to terminate the insurance contract and recalculate the cost of the loan.Another 20% of cases relate to those when the client was given the choice to either conclude an insurance contract or agree to a higher interest rate.

For example, Bank Z offers its customers two cash lending programs:

- 1 program - at 22% per annum, an additional insurance service is provided.

- 2 program - interest rate of 25% per annum, insurance is not provided.

Initially, the borrower agreed to 1 program, considering it more profitable. After a while and having recounted all the expenses, I came to the conclusion that I was mistaken, saving 3% at the annual rate, but paying 10% of the amount of the loan for the insurance policy. Having decided in this way to return his money, he switched to program 2.

Most likely, the court will refuse such a claim, since the insurance service was rendered to the client with his consent. In this case, you can win against a credit company.

However, most often the court tries to protect the rights of consumers and acts in their interests.

Tips for applying for a loan and insurance

Each borrower has the right to issue a waiver of insurance after receiving a loan from Sberbank, if this service was imposed on illegal grounds. We recommend filing applications and filling out paper for a loan with the included recorder in order to provide yourself with further evidence that this service was illegally imposed and have the opportunity to prove it in court.

Be careful when concluding a loan agreement, be sure to read all the sheets, let it take a little longer, but you will be sure that you will not be imposed additional services and conditions.

Thus, when applying for a loan at the bank, it is necessary to carefully study the documents, carefully read the terms of the loan and the amount of monthly payment.

This article shows that each borrower should be knowledgeable in the field of lending and insurance. If you do not want to insure yourself voluntarily, then simply fill out a sample application in Sberbank to refuse insurance after receiving a loan.