Deferral of tax payment is the ability to pay the amount of tax debt by enterprises or individuals to later lines. Each organization can change or extend the deadline for paying tax liabilities if there are good reasons that are prescribed in tax legislation. A tax credit can be issued for one or more federal or local taxes.

Taxpayers are entitled to take advantage of such credit privileges, whose financial situation does not allow them to pay tax in a fixed period in full.

But after a certain period, the taxpayer is obliged to pay off the amount of debt and installment interest.

What laws govern the conditions for granting tax deferrals?

The right to tax loans to entrepreneurs is provided by law in the following state documents:

- Tax Code, chapter 9, articles 61-68.

- The rules and conditions for applying a tax investment loan are regulated by Art. 66 Tax Code of the Russian Federation.

- Order of the Federal Tax Service of the Russian Federation No. MMV-7-8 / 683 @, “On Approving the Procedure for Changing the Deadline for Paying Taxes, Fees, Insurance Contributions, and Penalties and Fines by Tax Authorities”.

What taxes and liabilities can I apply for by installments?

Deferral and installment payment of taxes can be made in respect of the payment of one or more federal or local fees.

This tax credit is also allowed to apply for those taxes that are paid on a preferential or simplified system.

Federal taxes, which can be paid by installments:

- Value Added Tax.

- Individual income tax for individual entrepreneurs.

- Excise payments.

- Income tax.

- State fees.

- The tax on the extraction of precious and mineral resources.

- Transit fees.

- Single social contribution.

Deferral can also be arranged for the payment of such regional taxes:

- Transport fee.

- Property tax for individuals.

- Land tax.

- Trading fees.

But at the same time, deferment and installment payment of taxes and fees cannot be drawn up for those taxes that the company pays as an agent. For example, income tax on income from wages of employees. For organizations that pay income tax at a consolidated rate, it is also impossible to apply for an installment plan.

But at the same time, deferment and installment payment of taxes and fees cannot be drawn up for those taxes that the company pays as an agent. For example, income tax on income from wages of employees. For organizations that pay income tax at a consolidated rate, it is also impossible to apply for an installment plan.

Which government bodies are authorized to accept tax installment applications?

Given the different focus of tax obligations for which organizations can apply for deferment, the right to make decisions on the provision of tax credits is the responsibility of several state bodies.

- For federal taxes, to apply for deferral of taxes and fees, you must contact the federal executive body, the Federal Tax Service.

- For taxes to the local or regional budget, you need to write a statement to the tax authorities at the location.

- For taxes that are paid for the transport or transit of goods across the state border, you must, accordingly, apply to the Federal Customs Service or customs authorities in the field.

- Deferral of state duties can be issued in the authorized bodies for control over the payment of state duties.

- Deferral and installment payment of taxes on a single social contribution are drawn up in the federal executive body.

Grounds for granting tax deferral

The list of basic conditions in connection with which a deferment may be drawn up is established by tax legislation.

The reasons are spelled out in article 64 of the Tax Code of the Russian Federation. Mostly the possibility of registering an installment plan is the prerogative of enterprises or organizations whose financial condition does not allow them to pay all tax liabilities in full in due time. Any reasons for financial difficulties cannot be considered grounds for a tax credit. The tax code quite specifically prescribes a set of prerequisites for registration of installments:

- If the company suffered damage after circumstances that are in no way dependent on the applicant: disaster, natural disaster, terrorist attack, etc.

- For state or municipal enterprises, the cause may be untimely or insufficient receipt of appropriations or budgetary payments.

- If the company risks insolvency or bankruptcy in case of timely payment of taxes in full.

- For an individual, a proven financial insolvency may be considered a sufficient basis, which implies the impossibility of paying tax liabilities at one time.

- If the activity of the enterprise is clearly seasonal.

- Also, the organization can count on a deferment of transit taxes if it provides convincing evidence, which is already described in the customs legislation.

List of seasonal industries whose enterprises can apply for tax deferment

Deferral, installment payment of taxes or investment tax credit is often preferred to draw up enterprises whose activities are seasonal in nature, including those related to the production of seasonal goods. The list of industries whose enterprises are entitled to tax credits is also specified in the Tax Code.

First of all, this kind of tax relief is provided for agricultural enterprises, namely, companies for the harvesting and production of agricultural raw materials, plant growing, animal farming, pond fish production, vegetable fat production organizations, for the canning or sugar industries, as well as meat or dairy combines.

Also, tax deferral may be granted to enterprises whose activities are in one way or another related to the extraction or processing of natural or mineral resources. These are organizations engaged in the harvesting or extraction of peat, harvesting of wood, forestry enterprises, and mining of valuable metals.

Also, in the transport sector, installment plan is provided for enterprises transporting goods or passengers to regions with limited navigation periods and for companies engaged in the transport of goods to the regions of the Far North.

What circumstances preclude the possibility of a deferral?

Providing tax deferrals to organizations is a common practice in many industries that helps enterprises to function properly and reduce tax burdens in some periods. However, the law also provides for factors that exclude the possibility of a company issuing an investment tax credit.

So, the tax debt payment period cannot be extended if, in relation to the enterprise:

- currently considering a criminal case involving a violation of tax laws;

- proceedings are initiated in the case of another administrative or state offense;

- the tax authorities have reason to suspect the taxpayer of the intention to leave the borders of the Russian Federation, to take out part of the income or to hide part of his property;

- not more than three years have passed since the taxpayer violated the terms of payments on the previous installment plan or a court decision was made to terminate the installment plan due to violation by the taxpayer of contractual obligations.

List of documents for tax installments

The package of documents that must be collected to provide a tax deferral may vary depending on the circumstances in which the taxpayer relies on it.

The package of mandatory and universal securities includes:

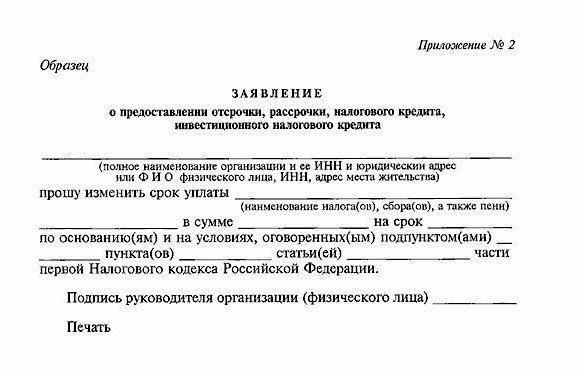

- An application for deferred payment of taxes of the corresponding form. Here you must specify the details of the enterprise, the name of the applicant, the individual tax number, the type of tax for which installments are expected, and the desired installment plan.

- Certificate from the local tax authority that the company has no arrears of tax fees, fines or penalties.

- Bank statement on cash flow for the last six months and a statement of the status of all accounts of the enterprise.

- A receipt in the obligation to comply with the installment plan and an approximate schedule of payments on tax credit.

- Copies of contracts with counterparties indicating the size of their receivables.

- Documents showing the reason for applying by installments:

- If the cause of the appeal was material damage after a natural disaster or terrorist attack, a conclusion on the fact of the occurrence of force majeure circumstances must be attached to the package of documents. It is also necessary to draw up an act of damage assessment drawn up by the executive authority or civil defense.

- If a municipal organization or a state order executor applies for an installment plan due to untimely receipt of budget funds, a statement from the financial authority on the amount of budget allocations, their non-payment or untimely payment must be attached to the list of documents.

- If the deferral or installment plan for the payment of tax is provided to a taxpayer whose financial condition does not allow him to fulfill tax obligations in full, he must attach a statement from the tax authority at the place of registration of the status of cash accounts to the application. As well as documents proving ownership of movable or immovable property.

- If the applicant requests a tax deferral due to the instability of income caused by the seasonal nature of the activity, he is obliged to provide a document from the local executive body confirming that the income from the activity that is seasonal in the structure of the income of his enterprise is at least 50%.

In some cases, tax authorities have the right to require additional documents in order to ensure tax refunds. Such securities are a bank guarantee, registration of a pledge of property. In turn, the taxpayer has the right to withdraw the application if he does not want to pledge his own property.

It is also worth noting that in recent years, requirements for providing bank guarantees or pledges of the assets of an enterprise or property of an individual have been put forward by almost every applicant. The reason for this is currency instability and an increasing number of speculations with tax credits.

What is the procedure for granting deferred or installment payment of taxes? How quickly is the issue of tax installments settled?

The procedure for obtaining a tax credit is declarative in nature. The taxpayer, having decided on the types of taxes for which he intends to receive installments, submits an application to the authorized state body.

This procedure can be carried out in person or through a surety.

To consider the application, the commission has 30 days after submitting documents. Having made the decision, she has up to three days to transfer it to the tax inspectorate at the applicant’s place of residence.

Within a month, when the tax service considers the application, it checks the condition of the taxpayer’s collateral assets, carries out their preliminary assessment. And also the administration is obliged to make sure that this taxpayer had no violations of the installment agreement in the last three years and whether criminal or civil proceedings were currently instituted against him.

A tax deferral is granted for a period of up to one year. In some cases, for enterprises of individual industries (research, design work, high-tech production), installments can be issued for up to three years. It is her most often called investment tax credit.

The refusal of the tax authority to draw up a deferral to the applicant must be reasoned. If the taxpayer does not agree with the decision to refuse, he can appeal it in court.

Tax deferral practice

Interest rates are provided for using the state tax credit of NK. Their size varies from 50% to 75% of the Bank of Russia refinancing rate.

In practice, tax installments look like a state loan at very loyal interest, which can only be spent on paying off the same taxes. If we take into account that last year the refinancing rate was 11.5%, then even if the tax authority sets the maximum interest on installments, the overpayment will not exceed 8%. And in the best case, the percentage of overpayment is 5.7%. Each company will agree that this is much less than the percentage for using a bank loan.

The development of the practice of state tax loans has reduced the amount of debt from taxpayers. At the same time, deferment of tax payment is still the prerogative of large companies, because collecting a package of documents and filling out an application requires a lot of time and organizational expenses from the management of the company.

Mutual obligations of the taxpayer and the tax authority for the provision and payment of deferrals

Tax deferral is a kind of agreement between the taxpayer and the tax administration to change the schedule and size of payments. Within five days after the decision on the installment plan is made, the administration and the applicant enter into an investment tax credit contract, which stipulates the installment period, the amount, the amount of interest, the tax under which the installment plan is valid, the mutual obligations of the parties to the contract.

The main duty of the taxpayer is the timely payment of a tax credit. If the organization does not fulfill this condition, the tax authority has the right to terminate the installment plan and request payment of obligations under the general conditions from the taxpayer. Also, the taxpayer is obliged to pay the remaining amount of debt and interest. Otherwise, the tax service begins the process of transferring collateral assets under a deferral of state ownership agreement.

But the tax service does not have the right to terminate the delay on its own if the company or individual complies with all the conditions of the contract.

In case of non-compliance with the tax credit repayment schedule, the taxpayer shall be fined or fined for each day of debt.