Entrepreneurs can independently choose which taxation regime they will apply during their work. If necessary, they can change the system, which requires notification of the Federal Tax Service. Quite often, a transition from USN to UTII is required, and often, on the contrary, individual entrepreneurs want to use a simplified system instead of an imputation. The process must be carried out while taking into account numerous rules. For this, the entrepreneur’s activity itself must meet the requirements of the selected regime.

The nuances of the modes

USN and UTII are simplified special modes used by entrepreneurs working in different fields. Using any of the above systems is possible immediately after the registration of the business or from the beginning of the new year.

To work in special modes, it is required that the entrepreneur himself and the chosen field of work meet certain requirements. The transition to any system should be official, therefore SPs are obliged to transmit relevant notifications to the Federal Tax Service. The document is transmitted within 5 days from the moment when work begins under the new regime.

UTII specifics

This mode is considered unique and easy to use. It can be used only by entrepreneurs working in certain areas of activity, which include household services, road transport or other standard work.

When calculating the tax, the physical indicator and the potential profitability of the business are taken into account. When using this system, it is not necessary to calculate and pay other taxes.

Features of USN

This tax system is also considered quite in demand. It is presented in two forms, so the tax can be calculated from net profit or total income. In the first case, 15% is charged from the difference between income and expenses. If all the cash proceeds from the business act as the tax base, then only 6% is charged from them.

According to this system, it is required to annually submit a declaration, as well as pay advance tax payments during the year.

When can I switch from UTII to the STS?

Entrepreneurs can independently decide which mode they will use, therefore, employees of the Federal Tax Service cannot force them to work on any system. The transition from UTII to the STS in 2018 is subject to the requirements of:

- if he voluntarily wants to complete this IP process, then the transition is allowed only from the beginning of next year, for which it is necessary to submit a notification to the Federal Tax Service by the end of December;

- if the activity ceases to comply with the requirements of UTII, or the ability to use this system is canceled in the region, then the transition from the beginning of the next month is allowed;

- some entrepreneurs combine modes, therefore, if the physical indicator for UTII was exceeded during the year, therefore it is impossible to use this mode further, then the activity switches automatically to the simplified tax system, and it is not required to send a notification to the Federal Tax Service.

If the requirements of the transition are violated, then the entrepreneur will be held administratively liable. Additionally, employees of the Federal Tax Service will recalculate and charge a penalty. The conditions for the transition from UTII to the STS are standard and enshrined in law, but local authorities can independently make certain adjustments to this process.

What documents are needed to switch to the simplified tax system?

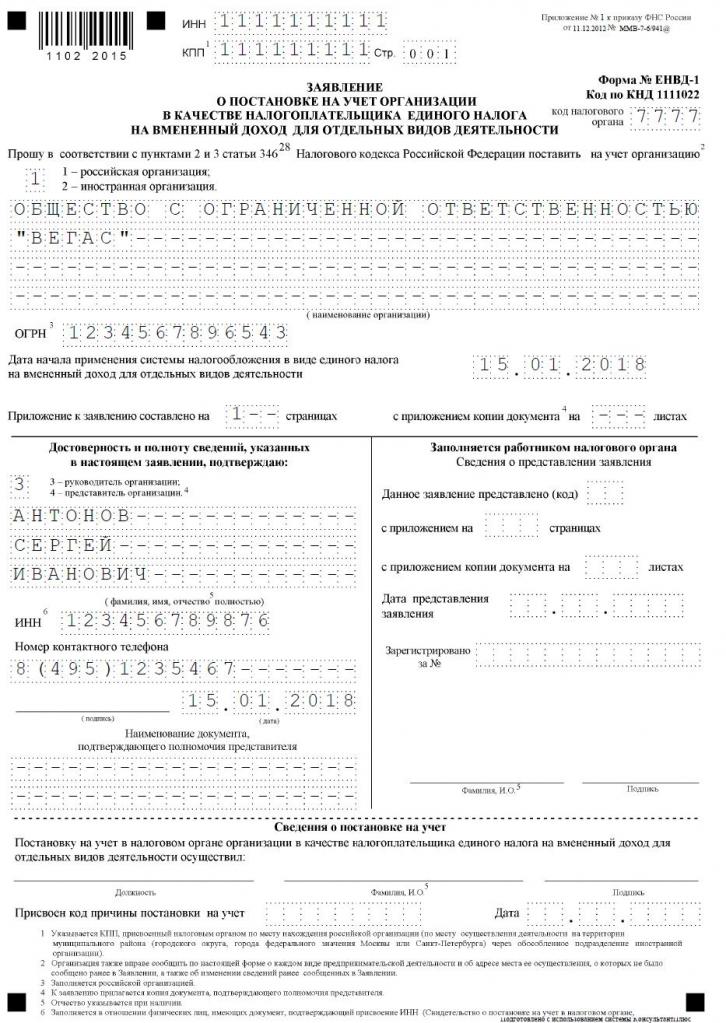

If you decide to work on the simplified tax system, then some documents will be required to switch from UTII to the simplified tax system.These include papers:

- direct notification of the transition to the simplified tax system in form No. 26.2-1;

- a statement on the basis of which the entrepreneur is deregistered as a taxpayer for the imputed income according to UTII-3 form.

Compose these documents is not difficult. A sample application for the transition from UTII to the STS is located below.

When do I need to transfer documents on the transition to the simplified tax system?

The procedure is performed only after the preparation of the necessary documents. The terms for the transition from UTII to the STS are standard, therefore, the following rules are considered by taxpayers:

- if a voluntary transition is planned, then the notification to the Federal Tax Service is transmitted until December 31 of the current year, which allows the use of a simplified system when calculating taxes from the beginning of next year;

- the transfer application must be submitted during the voluntary transition within 5 days, therefore, by January 5, the document must be submitted to the Federal Tax Service;

- if the transition is forced, because the UTII was canceled in the region or physical indicators do not meet the requirements of the regime, then the notification is transmitted within the next month, but the application must be submitted to the Federal Tax Service within 5 days from the moment when the IP ceased to be imputed tax payer.

Violation of these requirements is an administrative offense. Therefore, if the timing of the transition from UTII to the STS is not met, then the entrepreneur will have to pay a significant fine.

Where is the documentation sent?

If you plan to change the tax regime, then this process should be carried out officially. The transition of IP from UTII to the STS requires the transfer of an application and notification to the department of the Federal Tax Service, where the entrepreneur is registered.

If, when working on UTII, the size of the commercial premises was taken into account, then the Federal Tax Service Department at the location of this real estate property is selected to submit documents.

Rules for the transition to UTII

The transition from UTII to the STS is not always required. Many entrepreneurs do not know how and do not want to take into account the costs of their activities, so the use of imputed income is considered more beneficial for them. Therefore, often there is a need to start work on UTII, but for this the selected activity should be suitable for this mode.

The transition from STS to UTII is considered a standard process, but some rules are taken into account:

- it will not be possible to complete this process within one year for one type of activity, therefore, the procedure can be performed only from the next year, for which it is necessary to file an application for the transfer to imputed income until January 15;

- if an entrepreneur opens up a new area of work in which he prefers to calculate tax on the basis of UTII, he can apply for this regime at any time of the year, after which he will simply combine the two systems;

- if an individual entrepreneur is a taxpayer under the basic taxation system, he can submit an application for switching to imputed income at any time, since the law does not contain any prohibitions on this process.

Often, entrepreneurs need to combine several modes at once. Under such conditions, you should correctly understand what expenses relate to a particular type of activity.

How to apply for the transition to UTII?

To use this tax system, initially an entrepreneur needs to know a few points:

- whether work on imputed income is allowed in the specific region where the individual resides and works;

- whether the chosen direction in the business is suitable for the permitted activities on imputation;

- whether the entrepreneur has officially arranged more than 100 employees.

If these conditions are met, then the correct procedure for the transition from the STS to UTII can be implemented. For this, it is important to draw up an application for deregistration as a payer of the simplified tax system. A notification is pinned to him that the individual entrepreneur is starting to work as a payer of imputed income.

Documents are submitted at the place of direct activity. Often, an entrepreneur is officially registered in one city, and works in another region. Under such conditions, it is necessary to submit documentation to the department of the Federal Tax Service, where entrepreneurial activity is carried out. An exception will be trade, which is delivery or delivery, and also includes road transport or advertising on different modes of transport. Under such conditions, it is necessary to submit documents at the place of registration of the IP.

Within 5 days after the transfer of the application, you can get a notice from the Federal Tax Service that the individual entrepreneur was registered as a payer of imputed income. It is advisable to require this document so that the entrepreneur has evidence of official work in the selected regime. The document indicates the date on which the transition was made.

Is it possible to combine modes?

The transition from STS to UTII is not always required, since if an entrepreneur works on several types of activities, then he can combine several systems. This is not prohibited by law.

Imputed income can be applied only to certain types of activities. A simplified mode can be applied to other directions. It is important with this combination to correctly maintain separate accounting. To determine the tax base for the simplified tax system, it is not allowed to use the income received from activities for which the imputed income is calculated.

How is imputed tax calculated?

If there is a transition from the simplified tax system to the UTII, then the entrepreneur must carefully understand how the tax is calculated and paid correctly. For this, different indicators are taken into account:

- imputed income represented by potential profitability from the chosen direction of work, and this indicator is determined by the authorities;

- a physical indicator is taken into account, which can be represented by the area of the trading floor or the number of passenger seats in a car or bus;

- the deflator coefficient and the correction factor are included in the form, and these values are determined by each city separately, for which the economic condition of the region and other factors are taken into account;

- interest rate equal to 15%.

The main indicators can be obtained from the Federal Tax Service, so the entrepreneur only makes a physical indicator of his activity in the formula.

Is it possible to reduce the amount of tax?

When choosing UTII or STS, entrepreneurs can rely on a reduction in the tax base due to insurance premiums.

If an individual entrepreneur does not have officially employed workers, then he can reduce the tax base by 100% of the listed contributions for himself to various state funds. If there are hired specialists, then the base is reduced only by 50% of the paid contributions.

Tax Terms

If UTII is chosen, then payments under this regime must be paid quarterly by the 25th day of the month following the end of the quarter. Additionally, until the 20th of these months, you will have to submit each quarter of the declaration.

According to the simplified tax system, advance payments are made every quarter. Funds must be transferred before the 25th day of the month following the end of the quarter. At the end of the year, FEs must pay the final tax until April 30 of the following year. For enterprises, the deadline for paying tax and submitting a declaration is March 31. According to the simplified tax system, a declaration is submitted once a year by entrepreneurs until April 30.

Pros and cons of UTII

The transition to the impute is required by many entrepreneurs, since this mode has many advantages:

- tax burden is reduced, since it is not required to pay a lot of fees;

- the payment does not depend on the income received, so often it is really low with high profitability of the business;

- it is possible to reduce the tax base due to insurance premiums;

- in some regions, reduction factors are used to reduce the tax burden on taxpayers.

But this system has some disadvantages, due to which entrepreneurs often choose the simplified tax system. The submission of documents for the transition from UTII is required due to the fact that if there is no activity for some time, the imputed tax is still paid, since it is impossible to submit a zero return. Even if an individual entrepreneur receives a loss from operations, he will not be able to reduce the payment.

Therefore, each entrepreneur independently evaluates which mode is beneficial for the chosen direction of work.

Conclusion

The transition from one regime to another should be carried out officially. To this end, the Federal Tax Service must transmit relevant statements and notifications.

Most often, entrepreneurs choose between imputed tax or simplified tax treatment. Each system has pros and cons. The transition is possible within a year or from the beginning of the next year, for which it is taken into account whether the process is voluntary or mandatory. Entrepreneurs are allowed to combine these modes, for which it is necessary to correctly maintain separate records.