Entrepreneurial activity in the production of products and their sales is inevitably associated with a certain share of the costs of manufacturing goods and their promotion. Planned cost is the indicator of the estimated value of the goods that enterprises strive to reach, while maintaining a stable production process. Manufacturers inevitably encounter problems in fluctuating costs. Entrepreneurs resort to improving the technical base, establishing technological lines, selecting cheap raw materials or reducing the quality of goods at the outlet. To date, the normative or planned cost is the goal of any production. This indicator is influenced by many factors that our article talks about.

Growth of standardization of costs

The planned cost of finished goods is calculated at enterprises that are engaged in the production and further sale of goods. These industries include:

- Heavy industry enterprises: metallurgical, coal, mechanical engineering and others.

- Agricultural enterprises engaged in the cultivation of livestock, grain, etc.

- Light industry, which includes all sub-sectors involved in consumer goods.

- Food industry: canneries, meat plants, bakeries and other enterprises.

Each of the presented areas of activity has its own specifics for calculating planned production costs.

The cost of production includes costs of various types. For the correct approach to calculating the indicator per unit of production, it is necessary to take into account all the nuances of production costs.

Types of Initial Costs

All costs associated with the production of raw materials are taken into account when determining the value of the planned cost. This is an indicator that initially forms the future price of a product for an end user. Based on the received figure, a value-added tax on goods and other deductions are obtained.

There is a separation of costs based on the following types of expenses:

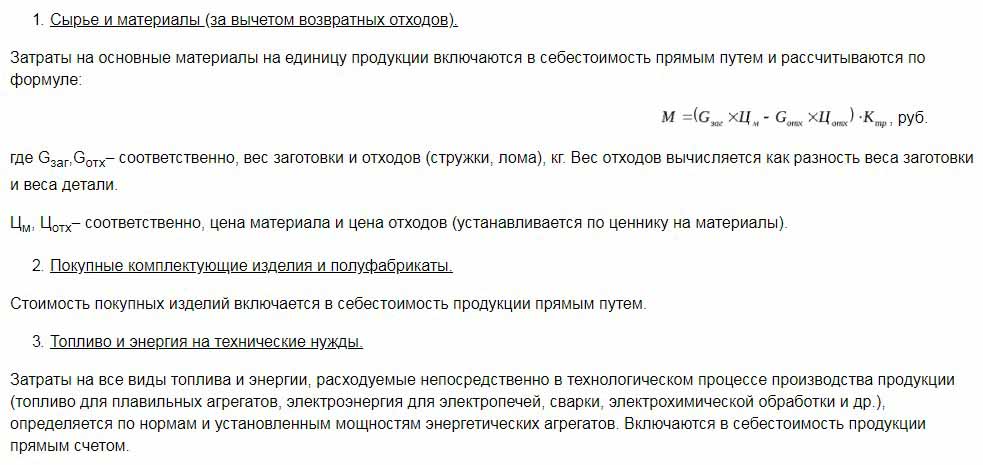

- The main ones. They are directly related to the acquisition of a raw material base for the production of a product. It is also the cost of ensuring the production process and wages for workers.

- Overhead. They are formed in direct proportion to the structure of units of management of a business entity.

According to how costs are taken into account in the cost of production, they are divided into:

- Direct - are formed based on the data of primary accounting.

- Indirect - associated with the provision of the production process.

Cost components may contain one cost element, for example, materials, or several consumables, for example, workshop. Such costs are commonly called complex.

Economic elements of costs: material, labor, social security contributions, depreciation of funds, other costs.

Planned cost

The sum of all costs of the enterprise is determined by normative indicators or directly by transferring them to products.

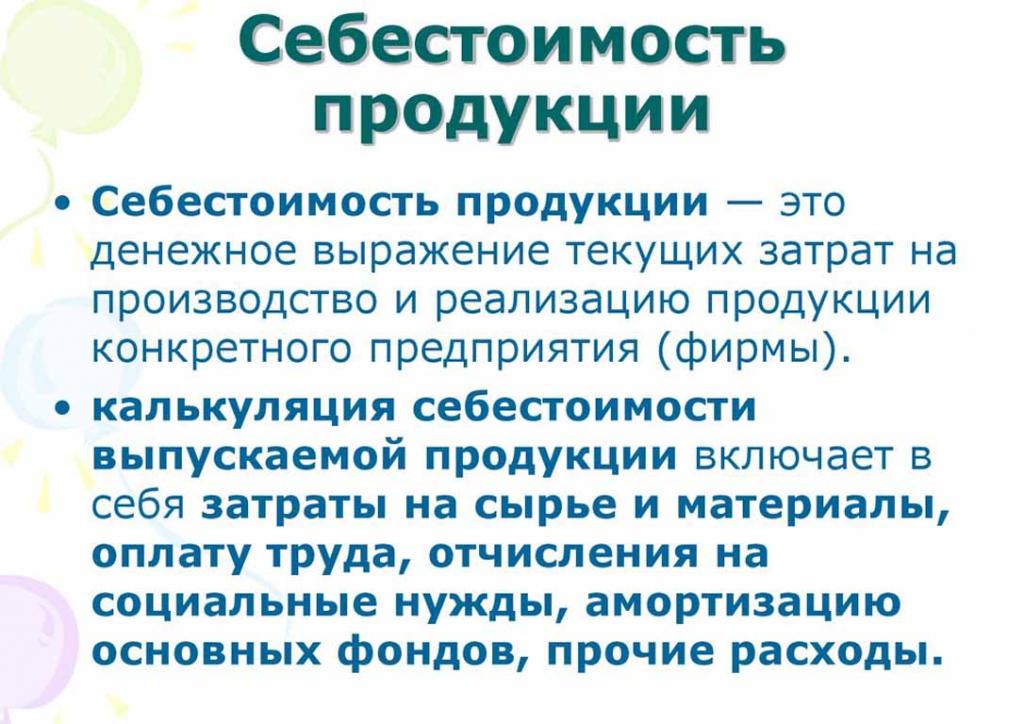

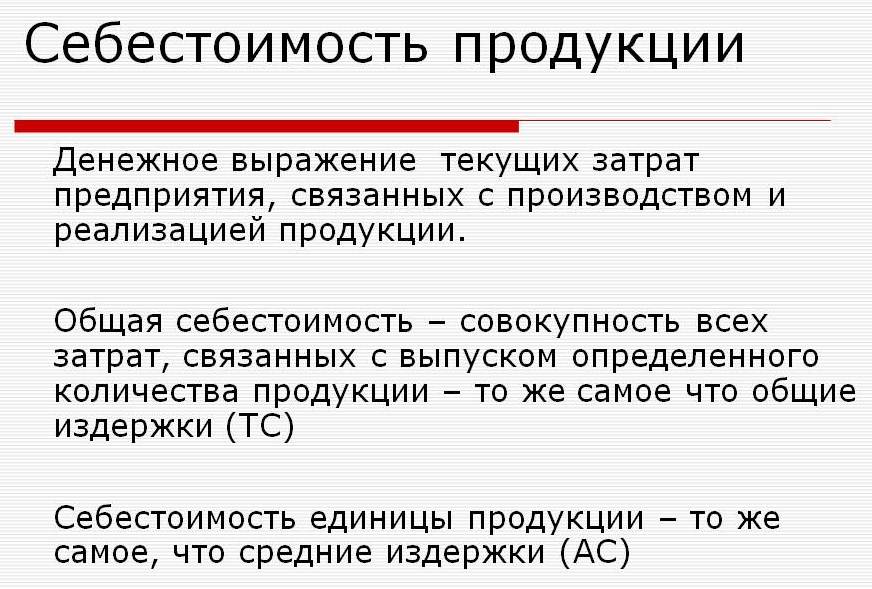

According to the definition, the planned cost is an indicator of the value of the volume of production during its production. Calculation is carried out both on the total output and on the unit of goods.

Indicators of planned cost are typical for the manufacturing industry, but they also occur in the accounting of trading enterprises.The spent part of the funds providing production processes is also included in the price of the finished product.

The planned costing of production costs is necessary to determine the feasibility of the production of goods. Based on this indicator, the enterprise management decides to change the course of activity and work with contractors.

Actual cost

The indicator characterizing the actually spent funds on the production of a unit of goods is called its actual cost. In accounting fixed material, manufacturing, financial and other costs.

The planned and actual cost are different values. Planning takes place at the beginning of an annual or quarterly period, but during the production process the amount of costs and the cost of materials may change.

The actual indicator is the sum of the costs of acquiring inventories (MPZ). Refundable taxes, such as value added (VAT), are not taken into account.

Methods for determining the cost of production

The monetary expression of the planned cost is the process of costing.

Internal planning at each enterprise has its own differences. There are three main methods of costing:

- Calculation in accordance with established standards. Based on past experience, internal rationing is determined or generally accepted industry indicators are used.

- Planned. It is based on cost planning that builds on previous total costs of production or sales.

- Reporting. It is the most accurate, since it is based on the actually spent funds for the past period.

Costing

The calculation of the planned cost starts with the preparation of cost estimates and costing. The indicator characterizes the planned average value. The basis for identifying the amount are progressive norms of costs for production, consumables, fuel, energy and others.

The planned costing starts with the collection of information on previous expenses, on the norms of expenditure of materials and raw materials. The final outcome depends on many factors:

- Waste production.

- Technical characteristics of the equipment.

- The purchase price of raw materials and additional components.

- Production time and labor costs.

Thanks to the calculation, the company's management gets a complete picture of the cost of each individual type of product.

An example of costing for total production and each type of product is presented below.

According to the presented example, the cost of 1 stool will be 1119, 45 rubles, and the cabinets - 2217 rubles.

At mass production enterprises, costing is done in stages. In each of the shops, products receive an additional margin and come out already with a certain cost. Thus, a gradual increase in the value of the goods in the production process is formed.

This way of determining the cost helps to make a reliable cost analysis. For example, in the manufacture of fabrics, the spinning mill determines the costs of making cloth, and the dyeing shop writes off its costs to the finished fabric. According to the results of the formation of the cost price of the canvas, the economists of the enterprise can identify at which point in the production costs can be optimized.

The in-line calculation method is relevant for the production of large volumes in large enterprises.

It is better to determine the planned cost of production for the estimated costing for a new type of product. The basis for the calculations are projects and norms of estimates of individual costs. Planned costing per unit of output is a short-term planning system. It is necessary so that the company can determine the stages of further development.

Reporting costs help determine the amount of the actual cost of production. It may consist of the following costs:

- Raw materials.

- Waste production.

- Energy and fuel for technical support.

- Wages of workers.

- Additional pay.

- Social contributions.

- Depreciation of equipment.

- General running costs.

- Production and non-production costs.

- Other expenses.

In factories with a large area, transportation costs may be included in the prime cost. Depending on the specifics of the industry, there may be other expenses: semi-finished products, additional units, etc.

Calculation of actual cost = Product balance at the beginning of the cycle (work in progress) + Costs incurred during the month - Costs for setting up the production process - Balance at the end of the cycle - Marriage.

Accounting for the planned cost of finished goods

The result of the production activity of the enterprise is the finished product. It includes all stages of production, packaging and transfer of goods to a storage warehouse.

Finished products are taken into account by one of two methods: at the cost of the actual and planned (at accounting prices).

The organization chooses for itself the most convenient of the calculation options and is subsequently guided by it in determining the costs of production of goods.

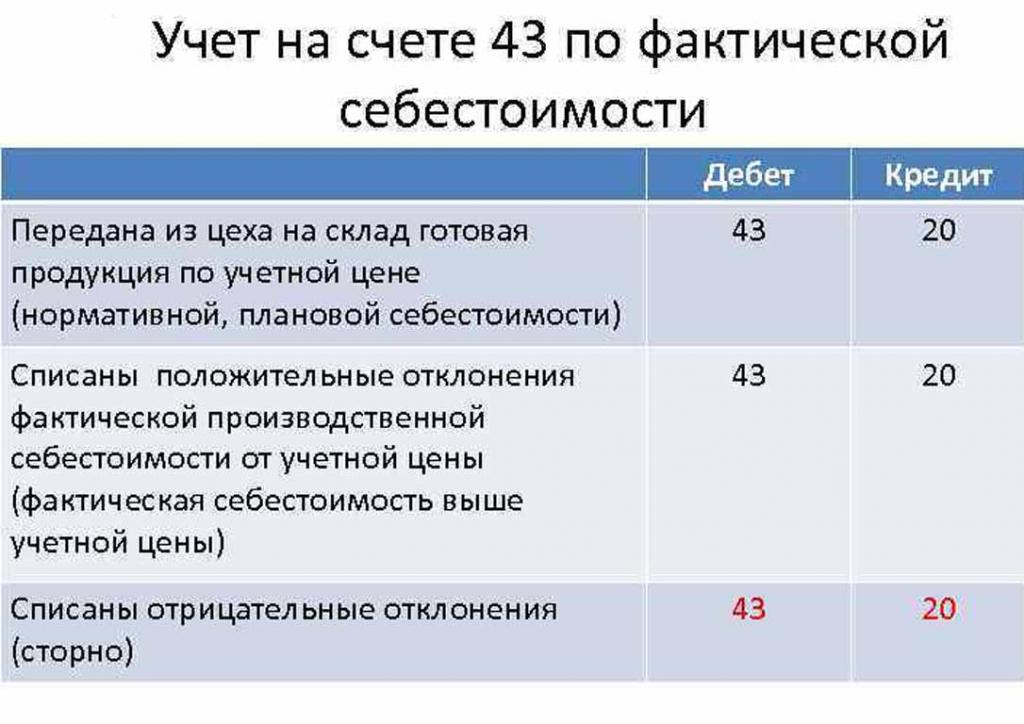

On the day the finished product is transferred to the warehouse, it is debited from account 43 "Finished products" to 20 "Inventories".

Deviations of the actual cost, positive or negative, are also posted to the indicated accounts.

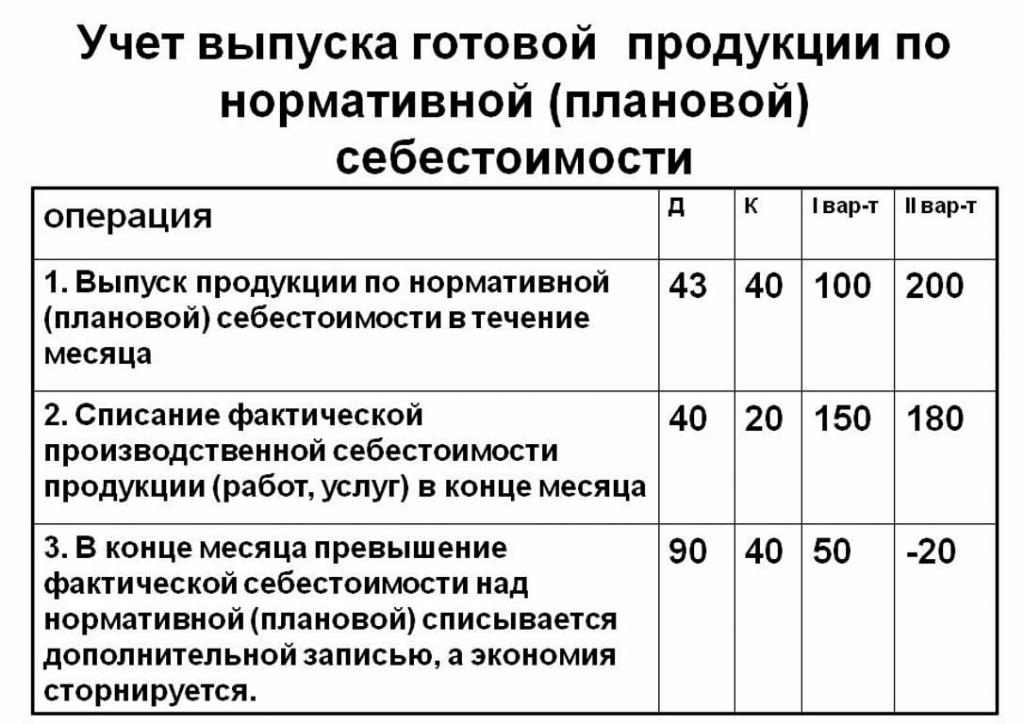

The accounting of products at the planned cost is made using account 40 "Output of products or services" or without it. Thus, the posting of products at the stated prices.

The normative planned cost without using account 40 is as follows: Dt 43 ("Finished products") Cr 20. The write-off of finished products is from account 20 ("Main production"), sometimes 23 ("Auxiliary production") or 29 ("Serving production and economy ").

At the end of the billing month, the deviation from the planned cost is written off over the actual cost.

Posting: Dt 90 ("Sales") Cr 40.

If the actual cost exceeds planned, then there is a loss. A situation in which regulatory calculations exceed actual ones leads to savings.

The reversal record Dt 90 Ct 40 writes off the credit balance (savings).

The calculation of the standard cost per unit of production

You can determine the planned cost of production based on the blanks of the product at the beginning of the production process in monetary terms, according to their estimated value. Total production includes costs:

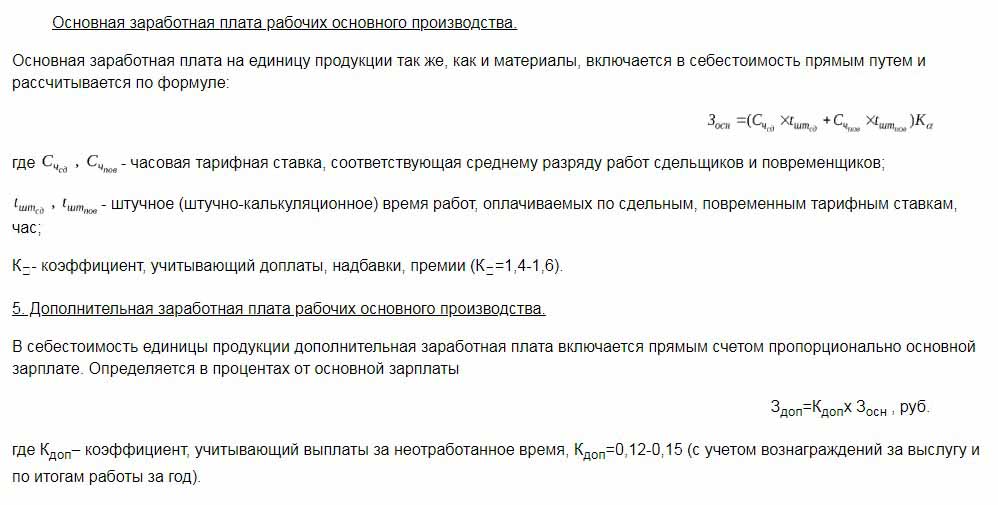

- Direct: raw materials, semi-finished products, fuel and energy, wages of production workers, additional wages, social and insurance contributions.

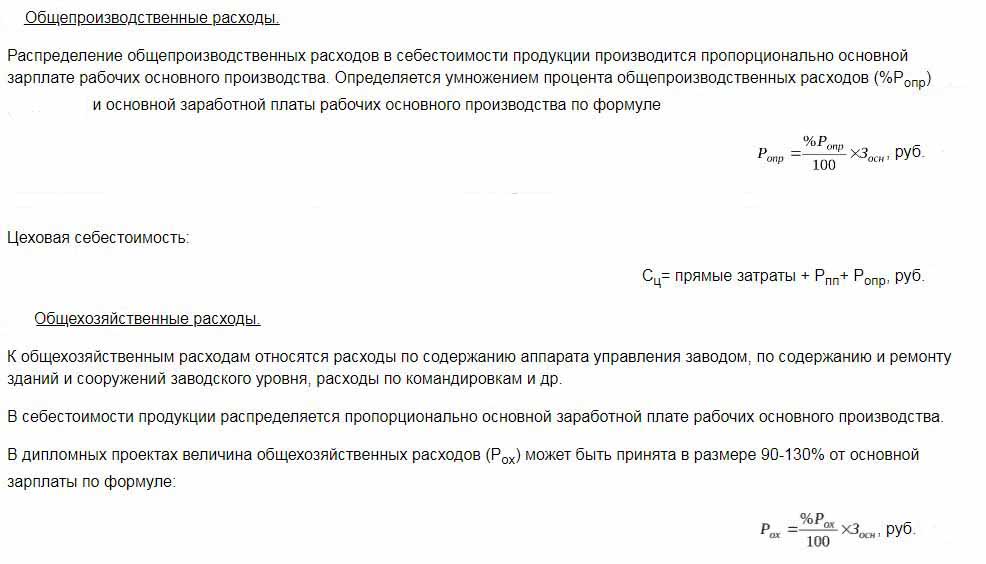

- Workshop costs include: direct costs, costs of production and preparation.

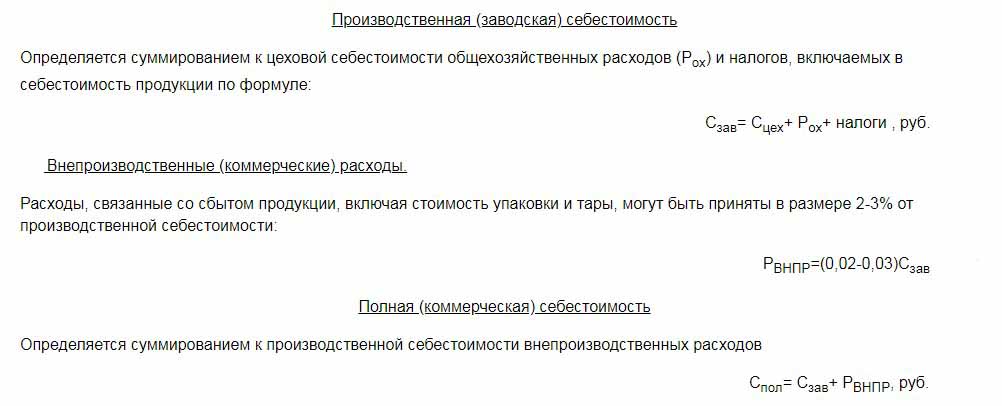

- Production costs are supplemented by general expenses and taxes, which are included in the price of the goods.

- Selling (or full) cost includes non-manufacturing costs.

Raw materials of the planned cost of a unit of production is calculated on the basis of procurement data. Purchased materials are included in the price on a straightforward basis. Consumed fuel and energy are also added to the cost of products and are calculated on the basis of indicators of the consumption of these resources.

The basic salary of workers in the production department is included in the cost of a unit of goods. At production, piece-rate wages are often applied, which depends on the volume of work performed (how many people produced products, so much received money).The planned and actual costs include the item of salary costs with the difference that the actual more often takes into account work time and piecework.

Time wages are set in separate units of production and also rests on the formed cost of output.

Additional allowances to workers' wages are calculated as a percentage of basic rates.

The costs of the development of production and adjustment of equipment are calculated on the basis of established standards.

The content of the control apparatus is also one of the expense items. General expenses are to be included in the planned cost of finished products. Overhead costs are calculated by adjusting the basic wage by a percentage of the type of costs. So, it is possible to determine the planned cost of production from the sum of workshop costs, general business expenses and deductions from the cost of finished products to public services (taxes and fees).

Deductions laid in the cost of goods:

- Land and transport tax.

- Property tax.

- Tax on environmental pollution.

The legislation of the Russian Federation establishes interest rates for each type of tax.

Planned cost is the sum of production costs and commercial support for the promotion of goods of the enterprise.

Non-manufacturing costs associated with the transportation, packaging and delivery of finished products to the wholesale buyer or end consumer. This item of expenditure includes all measures of the organization to promote its goods.

Based on the calculations, the economic department compiles a planned cost estimate. Thus, it is possible to determine all costs at different stages of their occurrence and optimize costs if necessary.

This document is the basis for the analysis of the production activities of the enterprise and allows you to consider the strengths and weaknesses of the production line.

The planned costing is compiled in a table with a listing of each type of cost. Per unit of production, costs are calculated in a simple way by dividing the amount of expenses by the number of units produced.

The reasons for the deviation of the estimated cost

During the production and sale of products at the enterprise, unforeseen situations may arise. These circumstances force the use of additional measures to eliminate the negative consequences, which entails a waste of money. These costs are covered by increasing the estimated value of the goods at the exit, that is, at the expense of the end consumer.

The main reasons for the deviation of the planned cost from the actual are:

- Increased consumption of raw materials as a result of marriage or technically obsolete equipment.

- Excessive consumption of fuel and energy.

- The time-consuming process of production of a batch of goods.

- Costs related to remuneration.

- Other factors.

As mentioned above, the planned and actual cost of production in practice have different meanings. Usually, upon production, the amounts are above the normative. This leads to losses, but the company may take measures to adjust future profit margins. In this case, the company's management makes decisions to improve marketing programs and search for new markets. Often, enterprises resort to lower prices to quickly sell and reduce stock balances. Exempted funds are used to optimize production.

Measures to reduce unplanned costs

In order to reduce costs, organizations conduct a number of activities:

- Modernization of obsolete equipment.

- Replacing full or partial lines of the production apparatus.

- Staff development at the expense of the enterprise.

- The development of a system of motivation for workers.

- Search for new suppliers.

- The acquisition of high quality raw materials, with which there is much less waste.

In practice, the main way to reduce costs is to replace raw materials. Unfortunately, often organizations purchase cheaper materials. As a result, product quality suffers.

Company policy indicates the course of activities and further development. Management makes the decision to improve the quality or increase the quantitative indicators. Orientation of the enterprise to export or import and demand for products play an important role in the direction of the company.

Negative situations stimulate the enterprise to take serious measures for further development. Quick market orientation helps the company to stabilize its activities in time and improve profitability indicators.