One of the guarantees of compliance with the terms of the transaction is surety. Commitmentarising from the agreement must be repaid in a certain period. To protect themselves, the lender (the credential) establishes an additional condition for the debtor - the involvement of a third party as a guarantor.

The concept of guarantee

As a way to ensure the fulfillment of obligations, it was used in Roman law. Guy gave his definition at Institutes. Surety as a way to ensure fulfillment of obligations represents a transaction in accordance with which a third-party entity assumes responsibility for the debt in the interests of the lender. A similar approach to the interpretation is used today.

Relevance of use

Securing obligations by guarantee quite common now. The use of this legal instrument is regulated by 361 articles of the Civil Code. Currently, a third party can vouch for the lender for the debtor for the entire obligation or part thereof. This action increases the likelihood of debt repayment. The fact is that in the event of delay or failure to fulfill the terms of the transaction, the lender has the right to present claims to this third party. Let's consider in more detail features of the guarantee as a way to ensure the fulfillment of obligations.

Nuances

Contract of guarantee of an individual involves individual liability of the subject, due to the property of which the requirements of the lender can be satisfied in case of violation of the terms of the transaction by the main debtor. One important conclusion follows from this. The effectiveness of the guarantee will depend on the personal qualities of the third-party entity, as well as on its property status. It should be said that a third-party entity can accept limited liability by establishing term of guarantee.

Specificity

In relation to it, three parties participate: the debtor, the lender and the third-party entity. Along with this, if you analyze the sample guarantee, you can find that this is a bilateral transaction. The lender and a third party act as its participants. The validity of their agreement will not depend on the absence / availability of the consent of the principal debtor to the transaction. His request can only serve as a prerequisite, a motive for concluding an agreement, but not as its legal element. A guarantee is an obligation that is based on a contract. Accordingly, for its occurrence and validity it is necessary to have all the conditions provided for by the general rules governing the appearance and legality of debt. Surety as a way to ensure fulfillment of obligations can be used by both citizens and organizations.

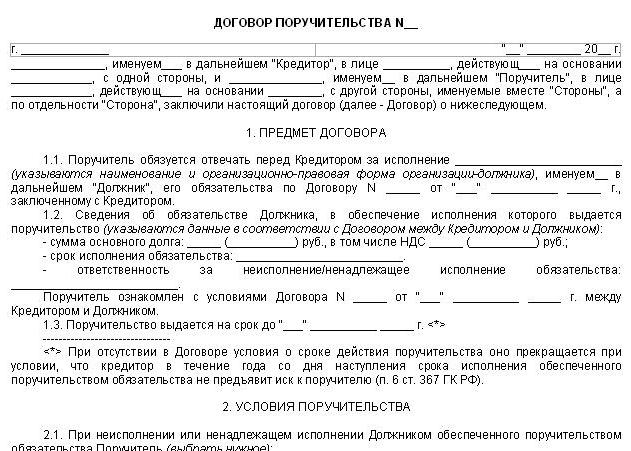

Agreement form

Lawyers pay special attention to execution of a guarantee. The legislation establishes a mandatory written form for such an agreement. In case of non-compliance loan guarantee or any other debt will be declared invalid. The corresponding requirement contains 362 articles of the Civil Code. If the guarantee is not executed by an agreement signed by the two parties, then a written message from the verifier on acceptance of the offer of the third party may act as evidence of such a transaction.If there is no such notice, then a reference to the guarantee in the original contract can serve as confirmation. If it is also absent in the text, then the corresponding relations are recognized as unstated.

Sample Surety

The agreement must contain all the essential terms of the transaction. These include:

- A description of the obligation that is provided by the guarantee.

- Scope and nature of liability indicating the amount. The agreement should clearly indicate whether the third party acts as a guarantor of repayment of the entire debt or only a certain part of it.

- The conditions under which performance of a guarantee obligation.

- The number of third parties. If there are several, then indicate the share in which they are responsible for the debt.

- Type of responsibility. It may be subsidiary or joint.

Of course, the agreement should contain information about the time, place of its conclusion, details of the parties, their signatures.

Limitations

Surety as a way to ensure fulfillment of obligations can be used in various transactions. For the believer, the identity of the guarantor, his reputation, authority is important. However, the key criterion is its solvency. The current legislation enshrines several restrictions for entities that cannot act as guarantors. A guarantee as a way to ensure fulfillment of obligations cannot be used:

- Budget organizations and state enterprises. It is in particular about those institutions to which the property was transferred to operational management.

- Representative offices and branches that do not act as legal entities.

Controversial situations

It should be noted that surety as a way to ensure fulfillment of obligations may relate to “future” debt. The corresponding assumption is provided for in article 361 of the Civil Code, in part 2. At the same time, legislation establishes a prerequisite for concluding such a transaction. In particular, it is necessary that at the time of its fulfillment the description of the obligation would be as concrete as if it already existed. The specificity of such an agreement is that the occurrence of the guarantor's liability depends not only on the fact of non-compliance with the main transaction. It is important that there is a conclusion of the original contract.

For example, consider a case from practice. The bank appealed to the arbitration with a request to the guarantor and the debtor to recover the main debt by agreement, penalties and interest for delay. The court satisfied the claim in full. At the same time, debt repayment was assigned to the borrower. The court stated that guarantee of an individual cannot be considered valid, since the corresponding agreement was signed prior to the issuance of the loan. At the same time, it indicated the amount in excess of arrears. Meanwhile, as indicated in article 361 of the Code, loan guarantee may apply to future loans. The conditions present in the text of the agreement made it possible to establish for what particular debt it was concluded. In addition, the loan amount was not greater than the one for which the security was provided. There were no other agreements under this guarantee. Given these circumstances, the appellate court overturned the earlier decision. On the basis of Article 363 of the Civil Code, the court imputed the repayment of the obligation to the borrower and guarantor jointly and severally. Please note that a guarantee can be issued for any debt that is not exclusively personal in nature.

Implementation of the terms of the agreement

Execution of Surety occurs if the main debtor assumes violations of the conditions of the original transaction. The essence of the guarantee is clearly articulated by applicable law. The surety accepts the obligation to answer to the principal for repayment of the debt partially or in full.This entity acquires legal certainty by indicating that if the principal debtor violates the conditions, he and his guarantor are jointly and severally liable if the law does not establish a different procedure (subsidiary). In addition, the rules stipulate that the guarantor has the same amount of obligations. It, among other things, includes repayment of interest, compensation of court costs and other losses of the creditor that arose as a result of improper fulfillment or non-fulfillment of the terms of the main transaction, unless otherwise provided by the guarantee itself.

Subsidiary liability

It may be provided for by a contract or legislation in the event of default or improper fulfillment of obligations by the debtor. The corresponding provision is enshrined in article 363 of the Civil Code in paragraph 1. For example, under Art. 134 of the Federal Law No. 127 (“On Bankruptcy”), in the event of the introduction of external administration of an arbitration court under a guarantee given by the Russian Federation, its constituent entity, Moscow Region represented by the competent authorities, the guarantor is subsidiary responsible for the obligations of the debtor. The implementation of this provision is carried out in accordance with the rules 399 of the Civil Code. If a surety as a way of ensuring the fulfillment of obligations involves joint liability, then the credential, guided solely by his own benefit, has the right to choose which of the two entities he will present his demands. If it is subsidiary, then the lender first of all addresses the main debtor. If he refuses to repay the obligation, including due to a lack of necessary funds, or within a reasonable period he has not responded to the notification, the penalty may be levied on the guarantor's property.

Important point

At present, it is indisputable to talk about the full fulfillment by the guarantor of the main obligation only if it ensures the repayment of monetary debt. At the same time, taking into account the dispositiveness of paragraph 2 363 of the Civil Code article, it is theoretically possible to admit the conclusion of an agreement under which the guarantor will satisfy claims of a non-monetary nature. In this case, the performance will be presented in kind. For example, it may be the delivery of a product.

Joint responsibility

As indicated by paragraph 1 363 of the Code, the order of execution of the guarantor will depend on the terms of the contract. But according to the general rule provided by the Civil Code, joint liability of the guarantor and the main debtor is established. It should be noted the peculiarity of the mechanism of its occurrence. The guarantee acts as an auxiliary obligation. In this regard, the guarantor, although it is jointly and severally liable with the debtor, but not unconditionally, but only in case of the occurrence of the relevant grounds - the failure of the latter to fulfill the terms of the transaction. From this it follows that the rules of articles 322-325 of the Civil Code can be applied to the relevant agreements only after the occurrence of circumstances in an amount that does not contradict the essence of the legal relationship and the provisions of special legislative norms. The joint nature of the guarantor’s impending liability is considered the basis for classifying it as a kind of intercession - accepting someone else's debt to oneself.

findings

Considering the above, according to Article 323 of the Civil Code, unless otherwise provided in the contract, the credential has the right to present a claim for liability to the surety and the debtor jointly or to any of these entities, either in a certain part or in full. If he did not receive satisfaction from any of them or did not receive enough, he can send complaints to the second party to the transaction. The surety, in turn, may send in reply to the creditor's claims all objections that the principal debtor could express. The guarantor does not lose this right even if the latter refused them or recognized the debt. The corresponding provision is enshrined in article 364 of the Civil Code.This norm indicates that the right of the guarantor is connected with the secured obligation, and not with the actions of the debtor.

Transaction Cancellation

Termination of Surety, except for the presence of circumstances common to all agreements, it occurs in cases enshrined in article 367 of the Civil Code. These include the following situations:

- Termination of the primary obligation secured by the guarantor. In this case, the basis on which this happened will not matter. Surety period may coincide with the period of validity of the main agreement. Accordingly, at the end of the last period, the warranty is void.

- A change in the original obligation without obtaining consent from the guarantor, if this entailed an increase in liability or other adverse consequences. Any adjustments to the terms of the main transaction affect the economic condition of the debtor. Changes can lead to very unexpected consequences, as they involve new risks. Of course, assigning them to a guarantor is unfair. In this regard, it is necessary to be guided by the presumption that any adjustment to the terms of the main transaction has adverse consequences for the guarantor. The guarantor himself can refute it through his consent.

- Transfer of the main debt, if the surety refused to ensure the fulfillment of the obligation by the new entity. This rule is due to the personal nature of the relationship between the guarantor and the debtor.

- Witness refusal to accept proper performance of an obligation. At the same time, both the guarantor and the debtor can offer it.

- Skip creditor deadline for filing a claim.

Tax area

Surety is not limited to civilian circulation. Often, participants in tax legal relations resort to this tool. The Tax Code provides for several ways to ensure obligations to pay budget payments, including surety. It is enshrined in article 74 of the Code. When creating this rule, the legislator was guided by the general rules provided by the Civil Code. However, although the formula for guaranteeing tax obligations is borrowed from the provisions of private law, its implementation is carried out in the framework of financial relations. This is indicated by the specifics of regulatory regulation of the use of this tool.

General rules for applying the guarantee: Tax Code

By agreement, the entity is warranted that it will fulfill the obligation of the taxpayer if the period stipulated for the payment of taxes changes, or upon the occurrence of other circumstances specified in the Code. Such a transaction is concluded between the guarantor and the tax office. The payer himself acts as its initiator. In case of failure to fulfill his obligation to deduct taxes secured by the guarantor, he and the guarantor are jointly and severally liable. The enforcement of budget payments, as well as interest, is carried out by the Federal Tax Service in a judicial proceeding. Since the responsibility is joint and several, the supervisory authority can send a demand for repayment of the obligation immediately to the guarantor, without notifying the main debtor about it. If the guarantor pays all the amounts imputed to him, he has the right to reimburse all costs incurred by him, in recourse. The guarantor, in particular, may demand not only compensation for taxes deducted by him, but also interest on them, as well as other losses.

Additional measures

The possibility of their application is provided for in Article 101 of the Tax Code. Paragraph 10 of the norm states that after a decision has been made to hold a subject liable for violation of tax laws or refusal to do so, the head of the control body may use additional measures. They guarantee the possibility of implementing this decision, if there is reason to believe that their non-acceptance may make it impossible or difficult to enforce it or recover fines, penalties, arrears.As interim measures, a ban on pledging, alienation of the payer's property without the consent of the tax inspectorate, and blocking operations on accounts in a banking organization in accordance with the rules enshrined in Article 76 of the Tax Code may be used. At the same time, as indicated by paragraph 11 101 of the Code, at the request of the subject, in whose relations these restrictions were adopted, they can be replaced by a surety of a third-party citizen, drawn up in accordance with Art. 74.

Conclusion

When executing a guarantee, in addition to the relationship between the guarantor and the creditor, interactions arise between the first and the debtor. As a rule, they are regulated by agreement. It establishes the conditions by which the amount of payment for the provision of the guarantee is determined, the calculation rules, the procedure for presenting claims to the debtor in case the guarantor fulfills his obligations, etc. In some cases, this agreement is missing. In such situations, after fulfillment of the obligation, the guarantor may present claims to the debtor, being guided by the provisions of the law (Article 365 of the Civil Code). In particular, the guarantor can count on the reimbursement of the amount of debt paid and interest on it. If the debtor has fulfilled the obligation, then in any case it is necessary for him to notify the guarantor about this. For non-compliance with this requirement, the entity is liable on general grounds.