Entrepreneurial activity in any industry is aimed at obtaining the final result - profit. For this purpose, various forms of management are being formed. In the process, the organization solves current problems and implements financial plans, as a result of which there is a distribution of profit in the LLC between the participants. An enterprise may be organized by several founders. All investors are persons interested in business development, but may not be directly involved in the organization. The founders provide their money and property for use by the enterprise, for which they receive dividends. But investors are attracted to solve the most important issues, such as selling a business, expanding it, etc.

Form of ownership of OOO

The concept of the type of ownership or form of ownership means the legal justification for the connection of a subject or business entities with an enterprise.

To date, there are such business entities as:

- affiliate

- collective;

- state;

- municipal;

- private.

Each form is distinguished by the peculiarity of registering entrepreneurial activity in state structures, the procedure for taking profits, management and tax rates.

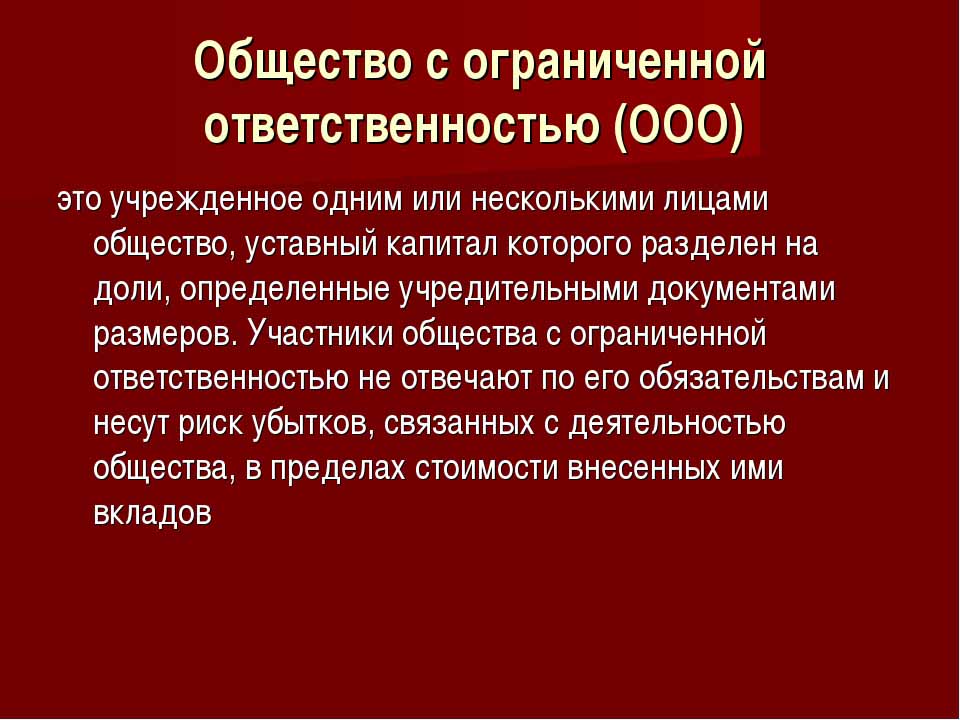

Limited liability company is the simplest form of business. Individuals and legal entities can be investors. Also, the authorized capital of an enterprise can be formed by one person.

Conditions for creating an LLC

The company is a collective or private form of ownership. This type of business organization is widespread in the Russian Federation. The owners of the object can be citizens of the country and non-residents, but not more than 50 people, also the founder of the organization can be one person.

Registration of a company implies the presence of an authorized capital in the amount of more than 10 thousand rubles, the seal of an enterprise, its Charter. The reporting form is more complicated than for an individual entrepreneur.

Features of LLC

A distinctive feature of a business entity is that its founders bear risks only in proportion to the number of contributions to the initial capital. Distribution of LLC profit between participants is carried out in accordance with their shares in the capital.

Today, society is the simplest form of ownership for collective activity. Investors are not required to directly implement the idea of managing. Usually, all matters are resolved by an authorized person. The general director or manager may not be a contributor, but is involved in doing business. The adoption of serious decisions regarding the development of the enterprise, the sale of its facilities and funds is submitted to the general meeting of the founders.

Distribution of profit in LLC between participants

The authorized capital of an enterprise is the main document that determines the shares of each of the founders in net profit, the dates of meetings and payments to depositors. Contributions to the fund may include cash, movable and immovable property, securities and other assets. Fixed assets and funds are needed to provide guarantees to creditors. When a limited liability company is opened, its participants lose ownership over their contribution, but at the same time acquire the right to receive a share of the net profit from doing business.

Limited liability of a company implies the removal of all claims against the founders and their property in the event of bankruptcy. They only lose what they invested as seed capital.

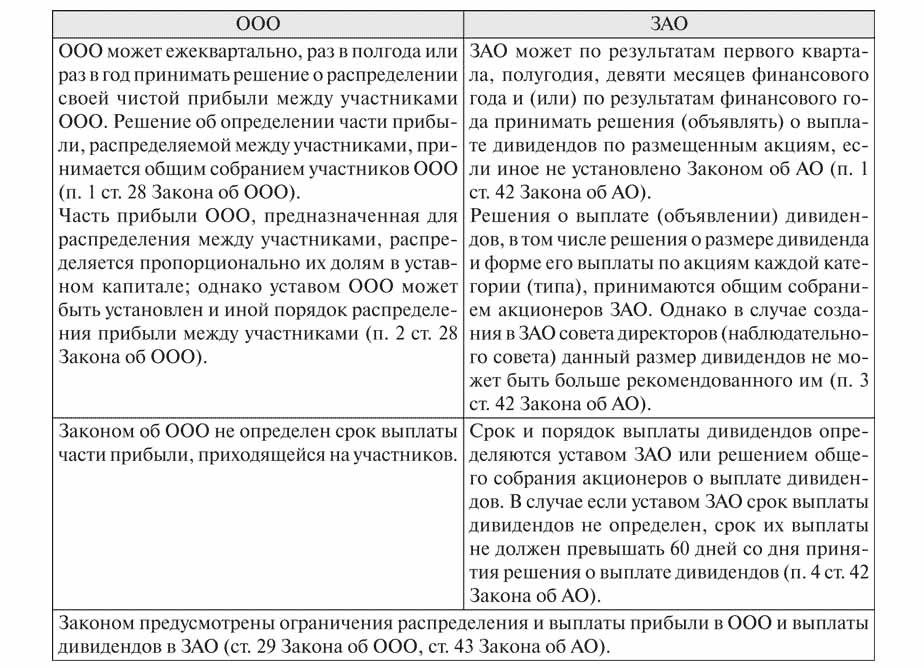

Distribution of LLC profit between participants is carried out for a period of 3, 6 and 12 months. This is the main difference between this form of ownership and stock.

The receipt of a percentage of the final economic result is preceded by a series of procedures.

Fixed capital of the enterprise, its structure

The charter of a company determines the size of its fixed capital. It is formed from the contributions of participants and for each of them has its own percentage ratio, or a fraction of the total amount invested.

For example, in monetary terms, the fixed capital of LLC Rus is 50,000 rubles. There are four participants, each of which contributed assets for a different value:

- the first - 17 000 r .;

- the second - 10 000 r .;

- the third - 11,000 p .;

- the fourth - 12,000 p.

Accordingly, the distribution of profit in the LLC between the participants occurs in fractions, or percent of the total. Based on the example, these are: 34, 20, 22 and 24%. Thus, each participant receives a percentage of the amount of net profit. During the meeting of the founders, a decision can be made only on the payment of dividends not from the full amount of net profit, but from a separate part thereof.

What is the use of net profit in LLC for?

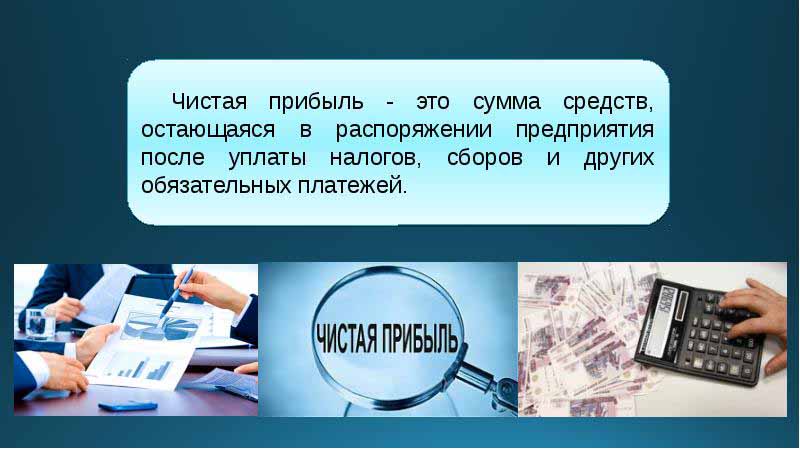

Every quarter, the founders of the enterprise can convene a meeting to make decisions regarding the income from the activities of the enterprise - net profit. According to the definition, this is the amount of funds after making contributions to the state control and taxation authorities.

According to the results of the reporting period at the meeting, the founders make a number of decisions in the direction of spending funds from profit. These assets can be divided by participants or directed to business development.

The main areas of fund transfers are:

- introduction of innovations in the production and development of the type of activity;

- deductions to the funds of the enterprise, the acquisition of buildings, structures, transport, the organization of repair of real estate, etc .;

- direction of assets to the reserve;

- deductions for the authorized capital;

- payment of social programs;

- coverage of past losses;

- dividend payment;

- payment of bonuses to employees.

Founders Meeting

At the beginning of the enterprise, a meeting of its founders should be held. It determines the size of the main fund and the share of each of the participants in it. This first meeting is basic and requires the presence of all participants. During the discussion of LLC activity plans, the frequency of the meetings of the founders is also determined. The meeting is dominated by a chairman selected from among the founders of the company.

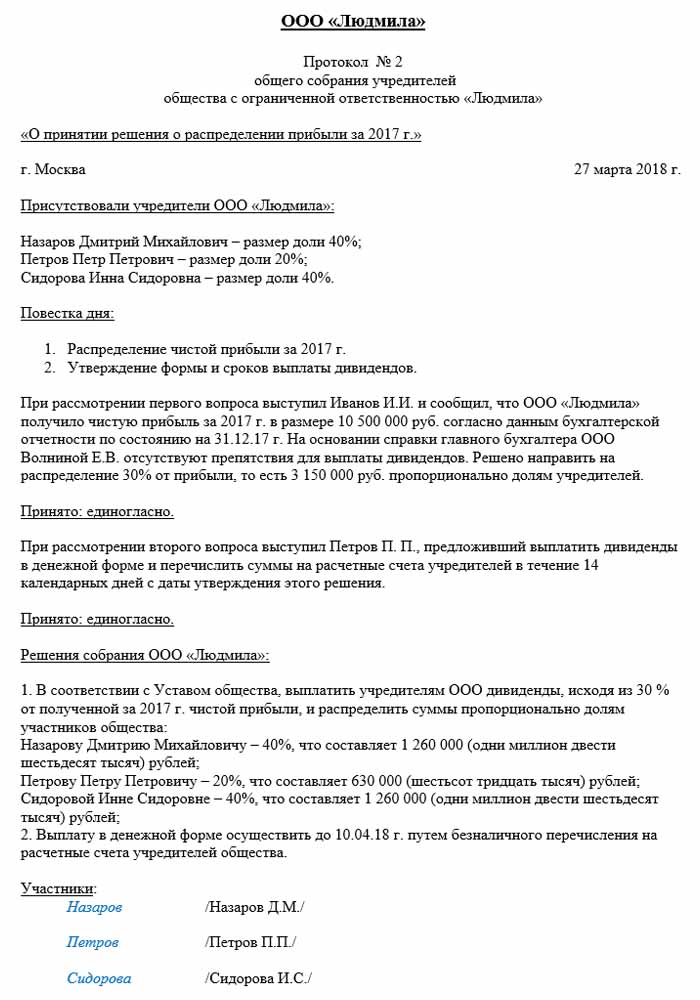

Decisions made at a meeting of LLC participants are necessarily recorded in the minutes. The charter determines the frequency of meetings. According to the legislation of the Russian Federation, a meeting must be held two months before the end of the reporting year or until the end of March of the following. For failure to comply with the deadlines prescribed by law, a company may be fined. LLC participants are informed in writing of a regular or extraordinary meeting 30 days before the event.

Distribution of profits in the LLC between the participants according to the protocol is made after the meeting of investors considered issues related to the development of the enterprise and the formation of its funds.

The order of the meeting

The federal law on limited liability companies establishes the procedure for holding meetings.

Only those of the founders who have passed preliminary registration are allowed to participate in negotiations and decision-making. Representatives of the founders may also speak at the meeting.

After the opening of the meeting, a discussion of current issues takes place. All measures and decisions taken are recorded in the protocol, after which 72 hours are allocated for its execution.This document also indicates the decision on how and at what time, with what frequency dividends are paid.

After a decade after the meeting, copies of the minutes are received by all participants in the meeting. A decision is made following the results of the meeting, the document is certified by the head of the organization.

The procedure for the distribution of profits in LLC

An important point in the payment of dividends to LLC participants is the proportionality of payments, according to the shares in the initial investment.

The charter of an enterprise may contain other methods for calculating payments. But the disproportionate distribution of profits in the LLC between the participants may entail fines from the tax authorities. Article 43 of the Tax Code of the Russian Federation provides that the income of citizens who are investors in the authorized capital of a company must be equal to the ratio of their shares in the total amount of capital. With this share of the distribution of profits in the LLC between members of personal income tax is charged in the manner prescribed by law.

The profit of the enterprise is distributed in full or in part. It is paid only in cash. Each of the founders has the right to claim its share in net profit.

Frequency of distribution of profits and terms of payment

How often participants will receive dividends from their contributions to the authorized capital of an enterprise depends on the decisions taken at the first meeting of depositors and the charter of the business entity. Typically, the shares of profit from the activities of the enterprise are paid quarterly, semi-annually or at the end of the calendar year. Distribution of profit in LLC between participants on a monthly basis can be carried out only on condition that this payment period is specified in the Charter of the company.

The most convenient is the annual distribution of profits. This is due to the fact that the activities of the enterprise can be planned, and there will be no shortage of funds for the implementation of tasks. Semiannual and quarterly payments are less convenient, as they require greater mobility in changing the directions of activity of a business entity.

The procedure for the distribution of profits in LLC between the participants involves the payment of the share of the investor no later than two months after the approval of the decision to make payments. But this period can be established by the Charter of the enterprise as shorter or longer.

When are dividends not paid?

There are restrictions on the distribution of net profit, which are associated with limited financial reserves of the enterprise.

Investors do not receive a share in net profit if:

- not fully replenished the authorized capital;

- the company has not closed all of its tax liabilities;

- LLC financial position is close to bankruptcy;

- if, in the case of dividends, the company is on the verge of bankruptcy;

- if the assets in value terms are less than the value of the authorized and reserve capital at the time of the decision on the distribution of profit to the founders, or may decrease after making payments.

The investor can receive a share of the net profit after the expiration of the settlement period for three years. In addition, the period for the payment of dividends is separately specified in the Charter of the enterprise at the time of formation of the LLC and can reach five or more years.

If the depositor has not claimed a share in net profit, it is returned to the balance sheet of the enterprise as retained.

Reflection in accounting

At the end of the calendar year, before the date of the meeting is set, retained earnings are allocated to line 1370 of the balance sheet. If this amount is a positive value, then it should be divided. In case of a negative indicator, the value is taken in brackets and refers to losses. When distributing profits in the LLC between the posting participants, they are classified as active-passive accounts. 84 account - "Retained earnings", it corresponds to each other in debit and credit. Each of the accounts may have its own internal sub-account. 84 account corresponds with 75 "Settlements with founders".From this account, funds are deducted for taxation and payment of dividends to depositors.

Distribution of profit in the LLC between the participants: an example

The date of accounting entries is the day the protocol is signed based on the results of the meeting. This necessarily takes into account the accountant of the enterprise.

An example of a distribution is the aforementioned Rus enterprise.

The protocol date is 02/10/2018, which means that the corresponding accounting records were also issued at that time. The amount of net profit (by decision of the founders), which is subject to distribution, is 50,000 rubles.

So, the distribution of profit in the LLC between the participants, accounting entries:

- D 84 K 84: 50,000;

- D 84 K 75: 50 000;

- D 75 K 68: 6 500;

- D 75 K 50: 43 500.

Depending on the number of participants, the net profit is divided:

- the first participant - 34%, 14,790 rubles;

- the second - 20%, 8,700 r .;

- the third - 22%, 9 570 p .;

- the fourth - 24%, 10,440 p.

The company is obliged to adhere to the rules and terms of payments and meetings specified by the legislation of Russia, also being guided by the Charter of the company. Public services carefully monitor the process of making tax payments and the timing of payments.