In recent years, VAT legislation has undergone major changes. They referred to the reporting form and the desk audit mechanism. The rules have also changed, according to which explanations to the VAT return should be submitted if the tax authority requires them.

General VAT Reporting Information

Since 2015, VAT reporting has become fully electronic. This means that all tax payers are required to submit a VAT return in the form of an electronic document on telecommunication communication channels (TCS). This obligation does not depend on the size of the income, the number of employees of the company and any other criteria. Only those who do not pay VAT, but play the role of a tax agent, that is, report to other persons, are allowed to submit a declaration on paper.

Another global change - the sales and purchase book data is now included in the declaration. Thus, checking the report, the tax service sees the information from the invoices issued and received by the company. And not just sees, but compares with what the counterparty reflected in his declaration. Therefore, errors and, therefore, requirements to provide explanations on VAT in recent years have become much more. According to the statistics of the tax service itself, erroneous data is found in every second tax return.

How does the IFTS verify declarations?

VAT reports of all Russian companies and entrepreneurs fall into a single database. First of all, they are checked for internal errors. There are correlations between the values of certain lines of the VAT declaration to be executed. If this does not happen, then the report contains an error. In this case, the taxpayer will automatically be sent a request to provide an explanation of the VAT declaration.

Next, an external audit of reports is carried out in the context of each transaction. For this, by order of the Federal Tax Service, a special software package was developed. For the operation reflected in the buyer's declaration, the system finds the counterparty. Then the information from section 9 of the supplier’s declaration is compared with what the buyer reflected for the same operation in section 8 of his report.

The specified data must match. This will mean that the buyer deducted the same amount of tax that the seller paid to the budget. If the data does not match, a discrepancy appears. And if there is a discrepancy, a requirement will be formed on the explanation of the VAT return. Thus, the system of the Federal Tax Service finds gaps in the chain of VAT and taxpayers who apply unjustified deductions.

What errors can be in the report?

Employees of the Federal Tax Service periodically report errors that lead to VAT clarification requirements. Here are the most popular ones:

- Errors in control ratios. They occur if the data does not fall into its own rows. As a result, the ratios between certain cells of the declaration are not executed.

- Incorrect use of codes of types of operations related to the sale of goods. Taxpayers mistakenly use code 26 in situations where it is necessary to apply code 01.

- Incorrect reflection in the purchase book of the restored VAT on preferential operations.

- Incorrect entries in books of sales and purchases when reflecting VAT from the advance payment and its recovery after sale.

- Incorrect reflection of import operations.

- Inconsistency of transaction information specified by the supplier and buyer in their declarations.

As for the last point, this is not one mistake, but a whole group.And so big that the Federal Tax Service decided to divide these differences into 4 types and assign each of them its own code.

Code “1” is the most dangerous for deduction. It is put if the counterparty to the operation cannot be identified, he filed a “zero” VAT return or did not indicate the disputed transaction in the report. Code “2” indicates discrepancies in sections 8 and 9 of the taxpayer declaration. Most often, these errors are related to the reflection of VAT deductions from advances received. Code "3" is intended for errors in the declarations of intermediaries and means a mismatch of data on received and issued invoices. If the error is of a different nature, it is marked with the code “4”.

Of course, the list of errors is much wider. The tax authority has the right to request clarification on any information that it considers inaccurate or suspicious. For example, an explanation of the “zero” VAT return of a company that previously paid quite significant amounts of tax may be required. In this case, the inspection may suspect that any tax evasion scheme has been introduced.

Response time

You can get the requirement for explanations to the VAT declaration at the end of the next reporting campaign. They are formed automatically and sent to taxpayers through the same telecommunication communication channels (TCS) through which declarations are submitted.

The fact that the document is received must be confirmed. For this, a return confirmation confirmation is sent to the FTS system. It is important to comply with the deadline - 6 days from the date when the tax authority sent its request. Therefore, after submitting the report, it is extremely important to check the accounting system for possible requirements. From the day the confirmation receipt was sent, the deadline for the preparation of an explanation will begin. For this, only 5 working days are given, so hurry up.

Violators are facing sanctions. If the receipt confirming the acceptance of the claim does not arrive on time, then after 10 days the inspection may block the taxpayer’s bank account. If the explanation of the VAT return is not provided within five days, the fine will be 5 thousand rubles for the initial violation and 20,000 for the repeated violation.

VAT declaration clarification form

Until recently, it was possible to respond to VAT requirements in any way, for example, by appearing in person or by sending explanatory documents by letter. Now, all taxpayers who report on VAT in electronic form (and this is the vast majority) are required to send explanations to the VAT return strictly in electronic form. The tax service has developed a special format for such an explanation, which is mandatory. If the company ignores this rule and sends an explanation on paper, the tax authority will not accept it. In this case, it will be considered that no explanation has been provided. If the electronic document format is violated, its admission will be denied.

Users of popular accounting programs should not have difficulties with the form of electronic explanation. Data exchange with the tax authority is carried out through electronic document management operators and is integrated into the company's accounting system, for example, in 1C. Explanation of the VAT declaration in this program is formed in the section “Refining the indicators of the declaration”. It can be accessed from the section “Reporting on value added tax”. In other accounting systems, the logic is approximately the same, although the name of the sections may differ.

Data verification and response preparation

So, the taxpayer has received a request for clarification and must prepare an answer. Before this, you need to check the information and operations that the tax authority considered erroneous. It is necessary to raise the primary documents and compare them with what is reflected in the declaration. This is especially true in cases where invoices are kept in paper form.

If discrepancies with the counterparty’s data are revealed, it is necessary to reconcile them. It compares the information of invoices and records with which both parties reflected the transaction in their books of purchases / sales. The party that made a mistake must make corrections to the relevant documents. As a result, the invoice information of both parties should become identical.

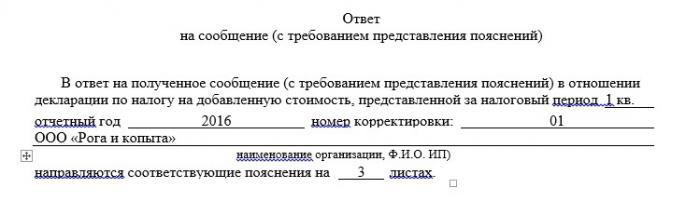

In the explanation it is necessary to indicate the correct data on the disputed transactions. In addition, you can attach scanned copies of documents that confirm the corrections. An explanation should be sent to the Federal Tax Service Inspectorate even when no errors were revealed as a result of the audit. In any case, the demand should not go unanswered.

Submission of revised declaration

If the errors identified by the tax authority are confirmed, you may have to submit an updated VAT return. This is necessary in cases where incorrect data led to a decrease in the tax base or to an overstatement of the deduction. That is, if the error caused a decrease in the amount of VAT payable, an updated declaration must be submitted necessarily. This must be done within the same time period as is allotted for clarification, that is, within 5 working days after receiving the request. But before filing the “clarification” it is necessary to pay the shortage of VAT, as well as interest for late payment, which will increase the chances of avoiding a fine.

In cases where incorrect information in the declaration did not cause a reduction in VAT payable, the refined declaration can be omitted. It will be enough to send an explanation to the IFTS.

Explanation sent. What's next?

So, the explanation of the VAT declaration and its annex, that is, copies of supporting documents, are sent to the Federal Tax Service in electronic form on the TCS. In response, a notification of acceptance of documents will be received, signed by an electronic digital signature of an IFTS specialist. If the explanation is made in violation of the established format, the taxpayer will receive a refusal to accept it. In this case, you need to bring it into line with the format and send it again.

The further fate of the explanation, unfortunately, may remain unknown. The fact is that the tax authority is not obliged to inform the company or the entrepreneur if their explanation led to the elimination of errors. So if you want to find out exactly this issue, you will have to contact the inspection.

But the fact that the explanation was not enough, the taxpayer must know. In this case, the company or individual entrepreneur may be required documents to verify the disputed operations. Also, other tax control measures, for example, examination, may be applied to the inspected person.

If VAT exemption applies

Preferential categories of tax payers are a separate issue. They are checked for the legality of applying the benefits. In this case, the taxpayer will be sent completely different requirements for explanations of the VAT declaration. A sample of such a requirement is given in the letter of the Tax Service dated 05.06.2017 No. ED-4-15 / 10574.

It is necessary to answer such a request in a completely different way. As evidence that the company had the right to benefits, it can send the register of supporting documents to the Federal Tax Service. This rule was introduced in 2017 to implement a risk-based approach to checking preferential VAT returns. The registry should be compiled in accordance with the form developed by the Federal Tax Service. It indicates the main parameters of the operation - the code, amount, data of the counterparty, as well as the name of the supporting document. The list and forms of standard contracts for preferential operations are attached to the registry.

The tax service will review the registry and request some of the documents listed therein for verification. Thus, the inspection facilitates its own task of processing documents, and also reduces the burden on taxpayers upon their submission. If the company does not send such a register or violates its format, the inspection will ask for verification of documents in full.The timing and procedure for responding to such a requirement is standard. Within six business days, you must send a receipt confirmation, and in the next five business days - explanations in the form of a registry.

How to reduce the risk of receiving VAT claims?

As you can see, modern technology helps inspectors to identify any errors in reports almost immediately. But they also come to the aid of the taxpayers themselves, giving the opportunity to identify errors even before the formation of the declaration. The first such tool is the introduction of electronic document management. The less manual work on the preparation of documents, the lower the likelihood that a mistake will be made due to the human factor. In addition, having established the exchange of invoices with its suppliers in electronic format, the company will protect itself from possible discrepancies.

Another powerful tool that will help to avoid data inconsistencies with contractors is all kinds of services for reconciling invoices. Companies and entrepreneurs upload their data there and check with contractors before sending a VAT return. The difficulty is that in this way you can only check with those companies and individual entrepreneurs that are users of the same service. A simplified version of such a reconciliation is on the tax service website.

VAT is one of the main taxes that form the income of the Russian budget. Therefore, much attention is paid to its administration. Recently, control in this area has been tightened, which is associated with the reduction of the FTS software package for checking VAT declarations. For the year of his work, he reveals about 3 million discrepancies in the reports. This means that millions of claims are sent to taxpayers annually to clarify the VAT return. And in general, there is nothing to worry about in getting them. The main thing is to respond to IFTS questions correctly and in a timely manner.