Companies, corporations and other business entities seek to improve their operations and increase profitability indicators. Profit is the main goal of the organization. In order to grow and develop, enterprises establish close ties with each other. Joint efforts help to achieve great heights and prosperity.

Ensuring a worthy meeting of business partners requires significant financial costs. This item of expenditure involves a fairly extensive list of activities. In tax accounting, they are referred to as "entertainment expenses". Every accountant knows that such costs attract the most attention from the State Tax Service. This is due to the fact that the article reduces the amount of taxable net profit of an economic unit.

Hospitality expenses

Organizational expenses apply to guests and representatives of the meeting enterprise. The place where a meeting or reception of business partners is held can be a restaurant, cafe, a meeting can also take place in the office of the company. It all depends on the preferences of the meeting party and the nature of already established partnerships. A business reception is defined by the Tax Code of the Russian Federation as measures to ensure a comfortable environment for negotiations or meetings. Maintenance involves the following costs:

- car delivery;

- escort of foreign partners;

- translation services;

- restaurant service;

- payment for a hired driver.

Regardless of what the spending is formed?

There are a number of factors that do not play a role in the process of creating a costly article in accounting, which relates to building partnerships in person.

These include:

- Time of receipt. It does not matter at what time of the day the meeting takes place, whether it’s working time or not. Spending refers to representation and in the case of events or meetings outside the working week.

- Place of organization of the meeting. In choosing enterprises are limited to an office or a restaurant. If the format of the institution does not correspond to the importance of the reception, then such expenses cannot be attributed to representative expenses.

- Negotiators can be officials and private persons, as well as company clients.

- If the amount of spending does not exceed the norm, the number of participants does not matter.

- The result of the meeting cannot affect the amount of spending. Whether cooperation will be established or not, payments were made. So, they are recognized as representative.

Compliance with the rules and regulations of accounting for hospitality expenses, how to formalize, an example is presented in the article.

Place of spending in tax accounting

Representation expenses in tax expenses are reflected in Article 264 of the Tax Code of the Russian Federation; it provides a complete list of types of expenses for representation purposes. Compliance with legislative acts when writing off expenses is necessary in order to tax enterprises and organizations. The costly part of organizing meetings is related to other expenses for the sale of products and their production.

The expenses are indicated in the letters of the Ministry of Finance dated 09.10.2012 No. 03-03-06 / 1/535, dated 01.12.2011 No. 03-03-06 / 1/796 are called hospitality expenses. And subject to strict control. All definitions are indicated without modification or deviation. Each of the types of expenses for meetings and negotiations is subject to strict control, therefore, for hospitality expenses we draw up documents correctly.

The list of documents prior to the formation of cost items

Documentary evidence of the allocation of funds for meetings and negotiations serves as the basis for writing off the amounts spent.

The basis for spending is:

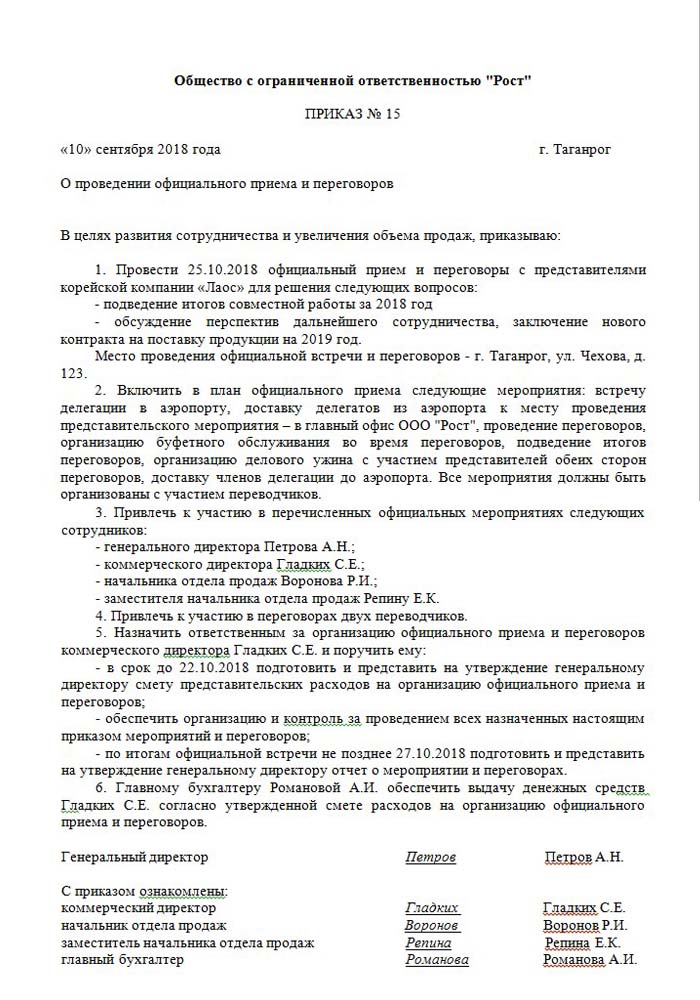

- Order of a higher management, director or person replacing him. This document includes specific time and date of meetings, venue of negotiations, a list of all participants.

- Estimated cost of the event. It is compiled separately for each stage of the occurrence of expenses: transport, restaurant service. The document is approved without fail by the director of the enterprise.

- A list indicating the sequence of events. Valid only with an order.

- Report on the results of the meetings. Composed by his responsible person, he has a similar structure to the order. Reflects the result of the meeting.

- Act of writing off expenses. Reflects the full picture in monetary terms. Signed by the head and chief accountant.

- Primary documents confirming expenses: acts of work performed, checks, etc.

It should be noted that a legislatively approved list of internal orders does not exist. This remains for management consideration.

Rationing of a part of other expenses

There is a clear definition of the amount of expenses for organizing meetings and receptions. This indicator may not exceed 4% of the salary fund for employees of the enterprise for the reporting period. The value of expenses for representation is reflected on an accrual basis in the annual report.

The date when the expense report for hospitality expenses is approved is considered the exact time of their implementation. If the business unit uses the accrual method, then the costs are classified as indirect within the reporting period.

The cash method of reflection of expenses reflects completed payments only on the provision of documentation confirming their implementation. These are checks, acts of work performed.

VAT on hospitality

It is very important to write off the value added tax of enterprises organizing receptions and meetings with partners. For all goods and services used by representatives of the organization, a mandatory tax is charged. Its amount can be deducted from their taxable profits of the event organizer. Such settlements are regulated by articles 171-172 of the Tax Code of the Russian Federation. Possible reduction of seized amounts in certain cases:

- if there is an invoice indicating the amount of VAT;

- representation expenses belong to the type of activity of the enterprise that is taxed;

- expenses are properly documented in accounting.

When a number of events are held during the organization of negotiations and meetings, those responsible have an idea of how costs can affect further taxation of profits. Therefore, they place orders only with those performers who can provide an invoice. For example, retail stores do not always issue checks with a separately allocated amount of VAT. This means that it cannot be deducted in the future taxation of profit.

Representation calculation example

It is important that only the amount of VAT of standardized representation expenses is taken into account. If expenses have occurred in excess of the norm, then they relate to other non-operating expenses and do not affect the amount of profit during taxation. Reflected on account 91, subaccount 2 "Other expenses". In tax accounting, the amount of VAT of representative expenses in excess of the norm is not reflected in any way.

It is possible that the difference in accounting and tax accounting will amount to VAT over expenses, it is taken into account in a permanent tax liability.

In accounting for VAT on hospitality expenses, how to draw up an example:

Products of Rost LLC are subject to VAT. In March 2018, a meeting with partners was organized at the enterprise.

| № | The amount of hospitality expenses, rub | VAT, rub | Payroll for the period, rub | Representative expenses, 4% of the wage bill, RUB |

| 1 | 5950 | 907 | 140000 | 5600 |

As a result, 5950-5600 = 350 r - go to write off other expenses.

Accounting for hospitality expenses in accounting

Unlike tax, in accounting expenses for a representative office do not have a separate reflection item. They include:

- depreciation deductions;

- material costs;

- to pay;

- social payments;

- other expenses.

In paragraph 8 of PBU 10/99, it is indicated that the company independently distributes expenses in internal accounting. Most often they are attributed to others, at industrial enterprises this is 26, and at trade - 44.

We show how to arrange hospitality expenses. An example of an accounting posting when debiting amounts to services.

| Debit | Credit |

| 26 "General expenses" | 60 "Settlements with suppliers and contractors" |

Accounting for material values (products, etc.)

| Debit | Credit |

| 44 “Costs to sell” | 10 "Materials" |

Conducting an operation in accounting programs

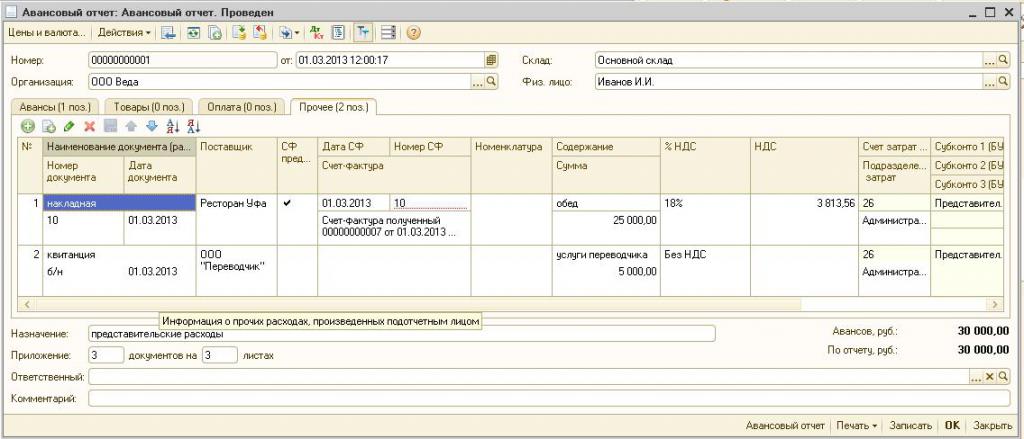

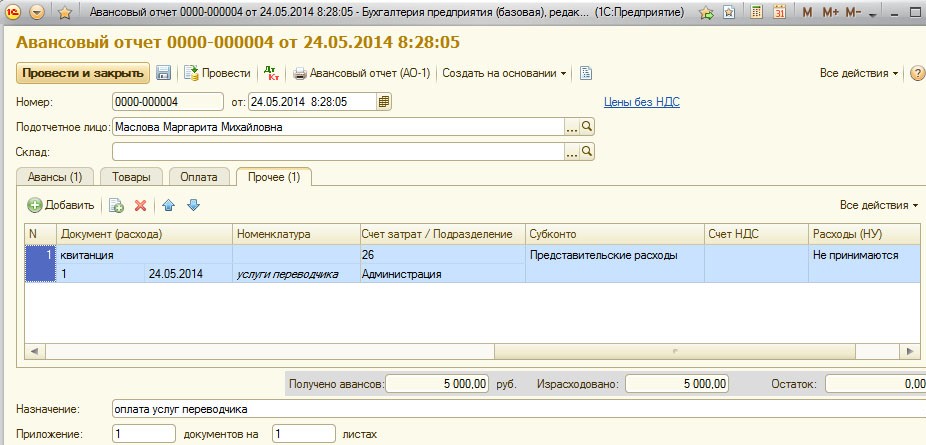

How to arrange hospitality expenses, an example in 1C.

The program for maintaining 1C accounting allows you to create advance reports, based on which the write-off of the sums of expenses for the representative office takes place. In 1C Accounting 8, presentation of hospitality expenses takes place according to a similar algorithm as in earlier versions of the program.

The essence of accounting is to create a bank statement or to issue money from the cash desk, and then on the basis of these documents an “Advance Report” is created, in which all expenses are indicated. Details can be found in the video below.

Requirements for writing off hospitality

The expense part of organizing receptions and meetings with partners is always of interest to the tax service. The management of the company often tries to reduce the amount of taxable profit by writing off part of the cost of representation. Therefore, representatives of the fiscal organization carefully check all the documentation confirming the accuracy of the spending.

The main requirement for writing off is the availability of thorough documents:

- internal order;

- an agreement with a company that provides negotiation services;

- primary documents: acts of work performed, an invoice from a restaurant or checks from retail stores.

Among other things, enterprises undertake to include in the list of expenses only those that are approved by law.

Representative expenses cannot include:

- permits and payment of rest in sanatoriums;

- spending on recreational activities;

- money for gifts and souvenirs to partners;

- accommodation of partners in a hotel;

- reimbursement of medical services, if any;

- corporate event costs.

Often there are contentious issues between representatives of the Tax Service and employees of the organization about the correct allocation of expenses for representation. These disputes are resolved by the arbitration court. Therefore, before writing off, it is necessary to make sure that it complies with Order No. 26n of the Ministry of Finance of the Russian Federation of March 15, 2000.