VTB 24 is a large and well-known bank, whose branches are located in different regions of the country. It offers many different banking products, among which a mortgage is considered to be especially popular. It is offered on favorable terms, since a low percentage is set. But often, existing borrowers have certain financial problems that do not allow them to further cope with the credit load. To avoid delays, they can take advantage of VTB 24 mortgage restructuring. It consists in making certain changes to the loan agreement.

The concept of restructuring

It is represented by a process involving a change in the loan agreement, which leads to an adjustment in the payment schedule. Its purpose is to reduce the credit burden on the borrower. Such an opportunity is offered only if there are good reasons, when a citizen really has difficulties with repaying a loan.

The law does not have an exact normative act regulating the restructuring procedure, but almost all banks operate according to a single scheme. The procedure begins only after the submission of the relevant application by the borrower. Documents confirming the deterioration of his financial situation are attached to this document.

VTB 24 Bank provides mortgage restructuring quite often, since each institution is interested in the repayment of a large loan in a timely manner.

Grounds for

Before applying for the restructuring of the VTB 24 mortgage, it is necessary for the borrower to prepare documentation confirming that there really are good reasons for implementing this process. Such grounds include:

- identification of a serious illness with the borrower or his family member requiring expensive and long-term treatment, therefore, further the citizen can not transfer the required amount of funds to repay the loan;

- loss of employment associated with the closure of the enterprise, reduction or other circumstances beyond the control of the borrower, therefore, if he quits for violations or by drawing up an application of his own free will, restructuring will be refused;

- a significant reduction in salary, and the application to the bank will have to attach a 2-NDFL certificate, which shows how much the borrower's earnings have decreased;

- an accident occurred that led to a loss of performance;

- the appearance in the family of a newborn;

- conscription of the borrower into the army for service;

- the death of a borrower who did not have a life insurance policy, therefore, a credit vacation is issued for six months, during which relatives can enter into an inheritance;

- the occurrence of other force majeure situations that negatively affect the financial condition of a citizen, for example, flooding or a fire in an apartment.

Any situation must be proved by official documents. Only after this, the restructuring of the VTB 24 mortgage will be approved. Feedback on this procedure is only positive, since due to changes in lending conditions, borrowers, even with low incomes, can easily cope with the loan load.

What loans are subject to restructuring?

Restructuring can be used for many banking products. These include the following types of loans:

- mortgage loan;

- target loan, the main purpose of which is the acquisition of a car;

- large consumer loans;

- credit cards.

If a loan was issued with the provision of mortgaged property to the bank, then it is much more difficult to arrange a refinancing. This is due to the fact that the bank can easily refuse the borrower to change the terms of the loan agreement, since restructuring is only a voluntary desire of the organization. The latter will be able to return their funds by selling collateral.

Ways to change conditions

At VTB 24, mortgage restructuring involves various changes to the loan agreement. The choice depends on the specific circumstances, but when drawing up the application, the borrower can independently indicate which method of re-lending is considered the most optimal for him. Therefore, the following options are selected:

- halving the payment for up to one year;

- registration of credit holidays, assuming that within six months the borrower will pay exclusively interest, and the main debt will remain unchanged;

- change in the currency in which the loan was issued, so if a currency mortgage was issued, then you can transfer it to a ruble mortgage loan, and this requires the support of the state, offering a preferential rate of 7%;

- an extension of the loan term for a period of up to 10 years, which will lead to a significant reduction in the monthly payment, therefore, even with a minimum income, the borrower can cope with the loan load.

Through the use of such opportunities, citizens are able to prevent delays, which inevitably leads to a deterioration in credit history. In this case, the bank will be sure that all funds issued earlier for the purchase of housing will be returned in full by the borrower.

What kind of support is offered by the state?

It is proposed to additionally restructure the mortgage with the help of the state. VTB 24 provides an opportunity for citizens who have previously issued a foreign currency mortgage to transfer it to a ruble mortgage loan with state support. Two options are used for this:

- the existing loan is converted at a preferential rate of 7%;

- debt is reduced by 600 thousand rubles, and these funds are paid to the bank from the state budget.

In addition, with the support of the state, it is possible to reduce the rate to 9.7% when transferring a mortgage to VTB 24.

Process conditions

The conditions for the restructuring of mortgages at VTB 24 are quite strict. To take advantage of government assistance to change lending conditions, the following requirements must be met:

- the presence of late payments, ranging from 1 to 3 months;

- one-time support from the state is 20% of the loan amount or 600 thousand rubles;

- the rate is reduced to 12%;

- To participate in this program, it is required to collect numerous documents submitted to AHML;

- documents are considered within 10 days, after which the applicant will be notified of the decision.

If the borrower does not want to use the help of the state and does not want to have delays in it, then if financial difficulties arise, it is advisable to immediately contact the department of the institution with a statement on changing the terms of the agreement. In this case, the restructuring of mortgages at VTB 24 will provide an individual with the opportunity to avoid a deterioration in credit history.

Borrower Requirements

An applicant for a change in loan conditions must meet certain requirements of the bank. These include:

- income per family member does not exceed twice the subsistence level, and this value differs significantly in different regions;

- over the past few months, family income should decrease by more than 30%;

- citizens belonging to vulnerable groups of the population, for example, families with children with disabilities, people with disabilities, civil servants, and employees of various companies important to the state, can count on state support for restructuring;

- the price of purchased housing does not exceed 60% of the average property price in the region;

- quadrature of housing should not exceed 100 square meters for an apartment m., and for the house - 150 square meters. m

The Bank may independently establish additional requirements and conditions.

Mortgage requirements

The conditions for mortgage restructuring in VTB 24 are determined directly by the management of this institution. Therefore, some requirements are made even for a loan being issued:

- initially the mortgage was registered in VTB 24, because if the loan is transferred from another bank, then this procedure is called refinancing;

- the amount of debt at the time of preparation of the application should vary from 30 thousand rubles. up to 1 million rubles.

It’s allowed to make an application even on the institution’s website, but in this case, restructuring is proposed only with a debt of up to 500 thousand rubles.

What documents are needed?

It is important to correctly prepare the necessary documents for the restructuring of the mortgage at VTB 24. These include the paper:

- passport of the borrower and all co-borrowers, if they were involved in obtaining a mortgage;

- mortgage agreement;

- documents for the purchased property, which include an extract from the USRN, technical papers and other documentation;

- certificate of family composition;

- certificate 2-NDFL and other documents confirming the receipt of income in the family;

- documents proving the existence of certain circumstances that do not further allow the borrower to cope with the credit load, and they can be submitted by a work book, medical certificate or income statement.

The more evidence of a deterioration in the financial position of the borrower is transferred, the higher the likelihood of obtaining approval.

Application Rules

An application for restructuring a mortgage can be filed in various ways:

- compiling an online application on the VTB 24 website;

- the formation of the document directly in the department of the institution, for which the bank employees issue the citizen the corresponding form;

- engaging a representative who must have a power of attorney certified by a notary with him.

In VTB 24, the restructuring of the 2017 mortgage was significantly different from the conditions that are offered in the current 2018. There is an opportunity to take advantage of state support, which will significantly reduce the interest rate.

The most relevant is the use of online treatment, since it is enough to log in to the site, after which data about the loan are entered. After that, the optimal option for changing the terms of the loan agreement is selected. But this method is suitable only for borrowers who have no more than 500 thousand rubles left to repay the mortgage. debt.

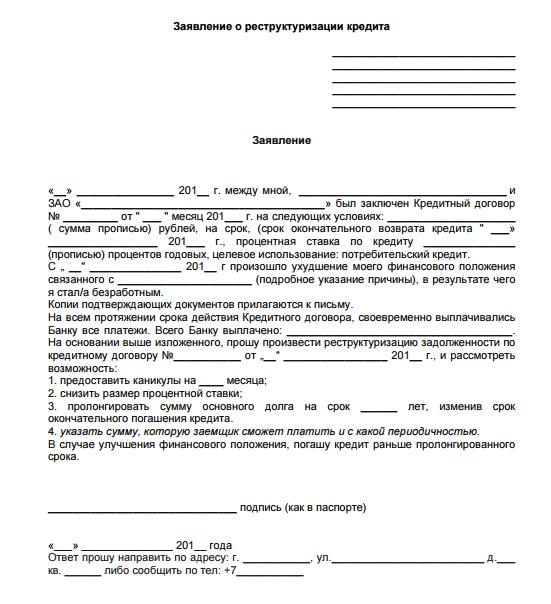

A sample application for the restructuring of the VTB 24 mortgage can be examined below.

How is the application considered?

If the application is filled out correctly, and all documents are attached to it, confirming that the borrower really had financial problems, then the documentation is considered within 5 days.

If the decision is positive, then the bank employee will contact the borrower and make an appointment at the branch. In face-to-face communication, all conditions for restructuring the VTB 24 mortgage are discussed. If both parties agree to the nuances of cooperation, a new loan agreement is signed.

If a negative decision is made, the bank client will receive a letter containing information with the reason for the refusal.

Reasons for refusal

Most often, a refusal to change the terms of a mortgage loan is due to the following reasons:

- the borrower already has delays in the past, and the restructuring is carried out exclusively in relation to bona fide and responsible payers who have really encountered serious problems, which the bank is notified in advance of;

- Documentation confirming that the borrower has actually encountered certain financial difficulties due to which he can no longer cope with the credit load is not attached to the application;

- previously, a citizen applied for restructuring;

- Bank employees decide that the difficulties that arise are not grounds for changing the terms of the contract, as income decreased slightly.

The reason for the refusal is indicated in the official document transmitted to the borrower. It will not even be possible to challenge such a decision even through a court, since banks decide on their own whether the terms of cooperation will be reviewed or not.

Pros and Cons of Restructuring

This process has both positive and negative parameters. The pluses include the ability to reduce the loan burden from the borrower. Documentation is reviewed promptly, and borrowers rarely face failure.

But the VTB 24 mortgage restructuring program has some drawbacks. These include the fact that the final overpayment of the loan is increased by increasing the loan term. Take advantage of such an offer several times will not work.

Conclusion

Restructuring at VTB 24 is represented by a unique process that allows changing lending conditions. It is offered on favorable terms for each borrower. For its execution, it is important to correctly prepare documents confirming the deterioration of the financial situation of a citizen.

You can apply online or with a personal appeal to the bank. The document indicates the desired type of restructuring and the reasons for using this opportunity. The decision is made within 5 days. If it is positive, then amendments are made to the current mortgage agreement.