Writing off bad receivables is an integral part of the business. The bad thing is that such debts are not always recognized as bad, after which it becomes possible to write them off. To understand what we are talking about, we first explain what accounts receivable are.

Definition

Accounts receivable - the amount of debt due to a company, enterprise or firm from other companies, enterprises, firms or citizens who are debtors and this complies with Russian and international accounting standards.

Accounts receivable are past due and normal. Overdue, in turn, is divided into hopeless and doubtful. According to the law, doubtful debt is a debt to an organization that arose during the fulfillment of obligations under a contract, which was not paid on time, specified in the contract and not secured.

Bad debt is a debt whose statute of limitations has expired, as well as debts that are not recoverable. A debt is recognized as bad only on the basis of an act of a special authority or after the liquidation of a debtor.

When does a debt arise?

The grounds for the occurrence of such debt are:

- Bankruptcy or liquidation of the debtor.

- The limitation period has ended, the amount is not agreed with the debtor.

Procedure for writing off debts

Once the debt has been discovered, you need to think about writing off bad receivables. First, they try to solve the problem with the help of claims, if this did not help, then lawsuits are used.

When, after the statute of limitations has expired, the debts are not closed or the debtor liquidated his enterprise, the only way out of the situation is by writing off the bad receivables.

According to the Civil Code (Article 196), in order to be able to write off a debt, a limitation period of three years must pass.

The write-off of bad accounts receivable from accountants is done by writing off the debt inventory, management order or written statements.

An inventory of debts is carried out according to the Guidelines for the inventory of liabilities and property. Based on the results of the event, an inventory act is drawn up using IVN-17 form. In addition, it is necessary to draw up a summary certificate in which they write:

- details and name of the debtor;

- date of debt and its amount;

- information from primary documents that confirm the debt;

- documents that contain information that there were attempts to repay the debt.

In addition, the act must reflect the amount of debt that is not agreed upon and agreed with the counterparties. Only based on this certificate, the head of the enterprise can sign an order to write off the debt.

Grounds for cancellation

To write off both bad debt and any other, you need to have reason. They must be supported by the necessary documents.

According to the Tax Code, such grounds include:

- liquidation of the debtor;

- end of limitation period;

- impossibility of recovery.

To part with the debt, the company must draw up documents to write off bad receivables.

These are the following documents:

- The act of inventory of mutual settlements with debtors in the form of INV-17.

- If it is impossible to recover the debt, then it is necessary to provide a decision of the bailiff that the proceedings are terminated.

- An extract from the state register of legal entities in which there is a record that the liquidation procedure of the enterprise is completed. This is if the counterparty is liquidated.

- The order of management that it is necessary to write off debt. The document is based on the remaining securities provided.

It is important to remember that it is impossible to write off receivables that are uncollectible if the debtor has no property. Such a debt is held for 5 years due to a possible change in the financial condition of the debtor.

Limitation of actions

The first thing that is determined before debt cancellation is the limitation period, or rather, its period. The beginning of this period shall be considered the moment when the firm or company established the fact that its rights were violated. The day from which the temporary violation of the payment of money for services or goods provided under the contract went perfectly is perfect. But prescription can be interrupted. The reasons for this will be:

- appeal to the court with a lawsuit against the debtor;

- the debtor acts so that the debt is automatically recognized.

An example of the latter reason is the repayment of a part of a debt, the signing of an act of convolution, a request for a deferred payment.

How to write off debt in accounting?

After the inventory, its results are drawn up, and dubious and uncollectible receivables are identified, whose statute of limitations has expired.

Documents that can confirm the presence of debt and the expired statute of limitations:

- Documents and contract for payment to him.

- Papers that confirm the services or delivery provided (invoices, acts).

- If there is a reconciliation act on hand, then it must also be provided.

- Official correspondence between the two parties, which confirms the fact that there were claims for a refund. Copies of letters must be supported by a document that indicates that the debtor received the letters. Such a document may be a notice of delivery.

It must be remembered that if there is an act of reconciliation for a specific date, then the term is calculated on a new one.

In order to be able to write off the receivables you need to have evidence that there is no way to write off the debt. For this, a lawsuit is filed against the counterparty, to which an act of unreasonability of recovery and a resolution are applied. In turn, this act says that the proceedings are completed.

To confirm the amount of debt, it is necessary to present all contracts with the debtor, as well as acts of transfer and acceptance of goods and invoices. In addition, other documents must be provided confirming that the debt actually exists and its amount. By the way, the shelf life of securities that confirm that the cancellation of debt was justified is 5 years for accounting and 4 years for tax accounting. This period is counted after all debt has been written off. In order to subsequently avoid confusion in the documents, such papers must be stored in a separate place until their expiration.

This type of debt can be taken into account on accounts 73, 60, 76, 62, together with VAT. When it is written off to other expenses, the VAT that is charged on goods and services is also taken into account.

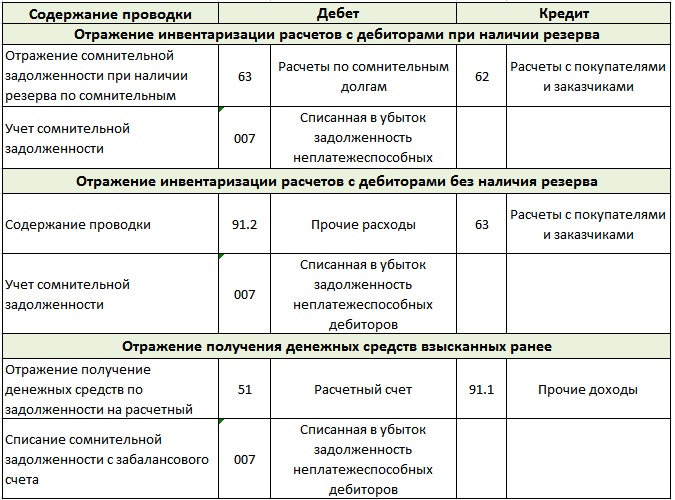

Write-off of bad receivables at the simplified tax system is carried out in accounting as follows:

- The debit of account 63 is the credit of accounts 60, 70, 62, 71, 76, 73. Only debts that have expired are written off. The same principle also works for writing off debt, which is not possible to collect.

- The debit of account 007. This reflects the debt that is not possible to collect, because it is written off.

On account 007 you need to keep a separate account for each debtor who has not fulfilled his obligations. Still separately take into account each debt, which is written off at a loss.When both debtors and receivables fall on one debtor, mutual settlement is carried out first.

And only when, according to accounting, bad accounts receivable cannot be covered by accounts payable, it is attributed to losses. This action is necessary in order to avoid unnecessary tax risks. If the company does not have a financial reserve for doubtful debts, the debt is transferred to the account "Other expenses".

How to write off debt in tax accounting?

According to article 226 of the Tax Code of the Russian Federation, if there is a reserve for doubtful debts in a firm, then it is from it that debts that cannot be collected are written off. However, in case of insufficient reserve, the remaining debt is included in non-operating expenses.

When the company does not have a reserve for closing debts, all losses are included in non-operating expenses. Be that as it may, but the amount for writing off the debt, together with VAT, reduces the taxable income. If the correct write-off of bad accounts receivable in tax accounting is made, then the company can reduce the tax burden in a certain period.

Such expenses should be recognized and reflected in the reports when the statute of limitations of the claim has expired or the enforcement proceedings have ceased and the debt has been recognized unrealistic for collection. In the event of the liquidation of the debtor, the debts are recognized as hopeless at the time when the debtor is officially excluded from the Unified Register.

Including VAT to write off debts

In the tax reporting, the procedure for writing off bad receivables must be supplemented with the following information: deferred VAT calculations - current VAT calculations.

When the company has a reserve for doubtful payments, all debts that are included in this reserve are classified as non-operating expenses. There is no VAT charge from these expenses until the end of the quarter. At the quarterly end, the amount (under the inventory act) of bad debt and the reserve amount are compared. If the latter covers debts, then this indicates that not all debts of the enterprise are non-refundable, which means that VAT must be paid from them. When the total amount of debts exceeded the reserve, the amount of the overpayment is deducted from the tax base. The deduction is based on data from the reconciliation report.

In enterprises where there are no reserves, accounting is required to conduct the procedure on a monthly basis. To be honest, the cancellation and recognition of the hopelessness of receivables does not have to occur before the end of the statute of limitations. It’s just that during the approach to the deadlines, you will have to urgently remove the losses and write them off within a month.

Why write off debt?

The fact is that current receivables are recorded in the general account of the company. This results in large taxes. Mythical money does not allow you to properly execute financial statements, so as to remain in balance.

That is why debts are written off, because there is no other way to get rid of exorbitant taxes. But again, you can write off the debt if it is recognized as hopeless. To do this, you need to properly issue all the charges.

First, we clarify that it is not always possible to write off all the debts of the company. For writing off, those that fully comply with the concept of debt, impossible to recover. Recall that these are debts that are impossible to recover from the debtor, these are also debts that have ended the statute of limitations or the debt of a company that has been liquidated and now does not exist.

Only the bailiff can decide that debt cannot be recovered.

Nuances

There are not many of them, but they are.

- When the debtor is an individual entrepreneur, it is impossible to write off his debt only on the basis of what was expelled from the Unified State Register of Enterprises.According to the law, an individual entrepreneur confirms that when he goes bankrupt, he will be liable to creditors for personal property. This means that closing a firm by an individual entrepreneur does not exempt him from paying debt. It is necessary to repay the debt, even if you have to sell your own property and things.

- In the case when two official companies have debts to each other, the debts are recalculated first. After such a recalculation, as a rule, only the firm that owes a large amount remains a debtor.

- The accounts receivable of a private person can only be written off after the bankruptcy procedure and the end of the audit. In two other cases, the debt can be written off from the debtor - this is the death of the owner of the company or the inability to establish the place where the debtor is located.

Who should write off?

We know that the inventory and accounting are carried out by order of the management of the company or at the time specified by law. Without fail, these events take place before the preparation of the annual report.

The client who has not returned the debt must go through the registry of doubtful payments. In addition to such registers, the debtor must be added to the lists of people who delayed payment by 90 days or more. If all this is not done, then such transactions will not accept tax.

Only the act of inventory, as well as documents that confirm the hopelessness of debt collection, give the right to write off funds from the account of the company. And since all the procedures that are related to money are managed by accounting, the write-off of bad receivables is also carried out by accountants. But they have the right to do this only after an official order received from the management of the company. It must be remembered that documents that relate to write-offs are kept for 5 years; you should not mix them with other papers.

After the statute of limitations has been suspended, the countdown is restarted. And the time that was before the interruption is not included in the new term.

Inability to fulfill an obligation

It so happens that there is no way to fulfill obligations. In such situations, no party is to blame. After all, the reasons for this are always independent of people. For example, a natural disaster, a fire. The death of the debtor can also be attributed to this group, but only in the case when the debt obligation is directly related to the personality of the deceased.

Obligations may also be completed if there is an act of a state body on hand. This also includes the writ of execution issued by the bailiff. It happens that the tax service does not take this as a basis for writing off a debt, but in this case you can contact the Ministry of Finance or the Supreme Arbitration Court. As a rule, they take the side of tax payers. To confirm, a letter is sent from the Ministry of Finance with the number -03-03-05.230 from 2010. The letter contains a link to your definition and it also indicates that from a certain point the debt must be considered hopeless.

Debt relief order

A sample order to write off bad receivables is usually held by the firm. In addition to general information, it must contain the following information:

- The name of the debtor company.

- Amount to be debited.

- Grounds for writing off bad debt.

- The specified procedure for writing off debt (costs and account created reserve).

If the order is filled out correctly, then in the future there should be no problems with paperwork.

No matter how much the head of the company would like to understand all the intricacies of taxation and accounting, this is not worth doing. At least, because a professional accountant will cope with such a task much better. And this means that time will be saved, nerves will remain whole and papers will be correctly drawn up.And you can advise the leader of the following - it would be better before you conclude an agreement with someone to give yourself work and form an opinion about a person, or even listen to your inner voice or an accountant. And then there will be much less such situations related to knocking out debts and, accordingly, work too. It is not in vain that there is a wise saying that you should never quarrel with your accountant. It has repeatedly confirmed its veracity.