The most common document that reflects information on the income of individuals received from the employer is a certificate in the form of 2-personal income tax. This document may be needed by each employee for various authorities. A certificate of personal income is required if the employee is in the process of applying for a loan at a bank, in litigation or for submission to government agencies. In our article, we will try to consider the main features associated with this help.

What is 2-PIT?

2-PIT is a standard reporting form for an enterprise on income received by its employee, as well as on tax deductions and taxes that were withheld. As a rule, a certificate is compiled for the reporting year, six months. However, it can be obtained for any required period.

The information contained in the certificate may vary and depend on who receives this certificate - the employee himself or the Federal Tax Service.

The personal income statement form has a sample approved by the Federal Tax Service. Nevertheless, it is recommended that you first familiarize yourself with the current, current edition of the order in order to verify the relevance of the form and not fill out its outdated sample.

Information required to be shown in the income statement

Certificate 2-NDFL issued to the employee by the organization, which is his employer.

There are two main types of help, depending on the purpose:

1. For presentation to an individual (who is a real or already dismissed employee of the enterprise). Issued on request.

2. For submission to the IFTS in the manner of mandatory reporting.

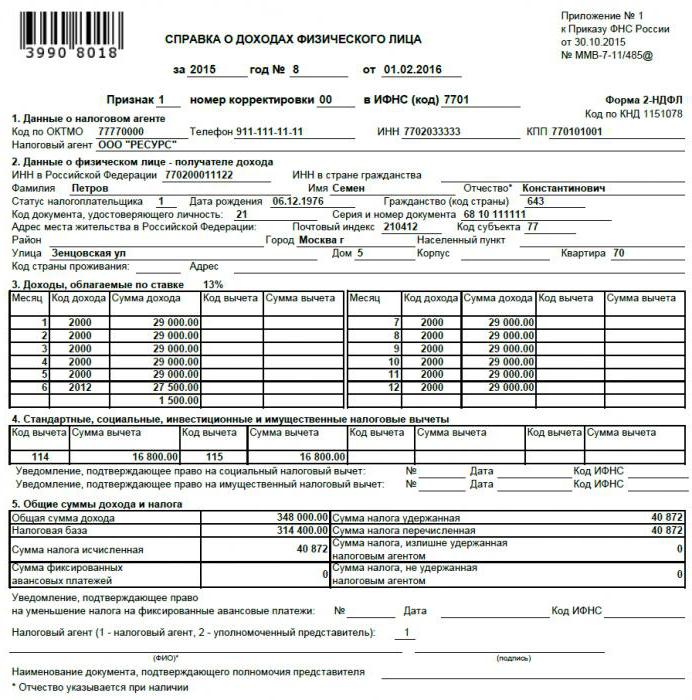

The certificate of personal income, which is issued to the employee, should contain the following data:

- General information about the company issuing the certificate. Includes the name of the organization with an individual taxpayer number and registration code.

- General information about the recipient of the certificate.

- The monthly total income taxed by an individual’s income.

- Types of tax deductions.

- Summary data on the amount of income for the period, as well as on the amount of taxes paid and deductions provided.

Reporting Help

A statement can be submitted by the company for the following types of tax reporting:

1. For all individuals who received income from this organization for the past reporting period (displayed on the form as sign No. 1).

2. For all individuals whose income the company did not withhold tax on personal income (displayed on the form as sign No. 2).

When filling out an income statement for an individual with a sign No. 1, the following data should be contained:

- General information about the company issuing the certificate: name, taxpayer identification number, tax reason code.

- General information about the person to whom the certificate is provided.

- The monthly total income taxed by an individual’s income.

- Tax deductions.

- The total amount of income for the reporting period, the total data on taxes and deductions.

Help with a sign number 2

When submitting a tax certificate on the income of an individual with a sign No. 2, the following information should be displayed:

- General information about the company issuing the certificate: name with an individual taxpayer number and code that indicates the reason for the company to be registered with the tax authorities.

- General information about the person to whom the certificate is provided.

- The total total income from which the withholding tax on the income of an individual was not made.

- The amount of tax that was not withheld.

Where can such a form be claimed?

Certificate 2-NDFL on the income of an individual may be needed by an individual who is on the staff of the enterprise in the following cases:

1. When passing the procedure for obtaining a loan from a bank.

2. In preparation for the surrender and preparation of tax deductions at the Federal Tax Service.

3. When applying for a pension at the Pension Fund of the Russian Federation.

4. When applying for social benefits by submitting an application to the social protection authorities.

5. In the course of litigation concerning labor matters, or in determining the amount of alimony.

6. When the tax return is submitted to the IFTS (forms 3-NDFL; required as a document confirming income).

7. When passing the guardianship procedure.

8. When passing the visa application procedure.

Directly to the IFTS, a company submits a certificate without fail. It is provided for general monitoring of taxes on the income of an individual, as well as for monitoring violations that may entail verification at the enterprise.

Features and order of submission of reference 2-NDFL

Submission of copies of a statement of personal income is illegal. Therefore, it is issued only in its original form. Extradition can be made not only to an employee who is a citizen of the Russian Federation, but also to a foreign citizen at his request.

Rules for submitting a certificate to individuals

1. The legislative basis for extradition is the Labor and Tax Code of the Russian Federation.

2. The basis for the issuance of the certificate may be a written statement from the employee (may be executed in free form).

3. The time period within which this paper is to be issued must not exceed three days after the date of writing the application for extradition.

4. The certificate must be issued in the number of copies requested by the employee.

5. It can be presented either in person into the hands of an employee or by postal mail at the place of residence. Copies that are submitted in electronic form, as well as copies that do not bear the seal of the organization and the signature of the authorized person, are invalid.

A certificate of income of an individual is filled in according to the model that is available in the organization.

Rules for submitting information when reporting to the Federal Tax Service Inspectorate

In the case of providing a certificate with a sign number 1, the following rules must be observed:

- The legislative basis is the second paragraph of Article 230 of the Tax Code.

- The basis for the submission is a requirement by law. And it has a mandatory order.

- Dates of submission: before the beginning of the second quarter of the year following the reporting year (that is, until April 1).

- A statement of the income of an individual (the sample of filling is presented above) should be presented in the amount of one copy for each employee of the organization.

The following presentation methods are possible:

- Personally representative of the organization.

- By postage.

- Via the Internet or on electronic media. In this case, an electronic signature of the organization is required. It is accompanied by the provision of an explanatory register in the amount of two pieces.

In the case of the presentation of a certificate of income of individuals with a sign No. 2, the following rules must be observed:

- The legislative basis is the fifth paragraph of Article No. 226 of the Tax Code.

- The basis for the submission is a requirement by law. And it has a mandatory order.

- Duration of submission: before the end of the first month following the reporting year in which payments were made without withholding the personal income tax (that is, until January 31).

- Must be provided in duplicate for each employee.One is intended directly for the inspection of the Federal Tax Service, the second - for the employee of the enterprise.

The following delivery methods are possible:

- Personally representative of the organization.

- By postage.

- Via the Internet or on electronic media. In this case, an electronic signature of the organization is required.

- For an individual - either personally in hand, or by mail.

Possible liability for evasion of 2-NDFL certificate

In the event that an enterprise refuses to submit a certificate of the amount of income paid to an individual at the request of an employee or makes violations when issuing a certificate, then such actions can be regarded from two perspectives, each of which entails administrative liability:

1. Failure to issue a certificate (regulated by the third paragraph of Article 230 of the Tax Code and Article 62 of the Labor Code of the Russian Federation). In this case, respectively, with the Code of Administrative Offenses, the application of such preventive measures is possible:

- An administrative fine may be imposed on the official responsible for issuing certificates. It ranges from 1 thousand rubles to 5 thousand rubles.

- An administrative fine may be imposed directly on the organization. It ranges from 30 thousand rubles to 50 thousand rubles.

- Freezing the activities of the organization for up to three months.

2. Refusal to issue a certificate. In accordance with the Code of Administrative Offenses, an administrative fine may be imposed on the official responsible for issuing certificates in the amount of 1 thousand rubles to 3 thousand rubles.

Certificate of annual report for IFTS

If we talk about the submission of a consolidated statement of personal income in the context of submitting annual reports to the IFTS, then two cases can be differentiated:

1. Delay in feed (delay). A penalty in the amount of two hundred rubles (in accordance with the first paragraph of Article 126 of the Tax Code of the Russian Federation) is imposed on the company for each certificate that was not submitted in time.

2. Actions to fail to provide certificates requested by the Federal Tax Service Inspectorate, or deliberate distortion of the information contained in them (second paragraph of Article No. 126 of the Tax Code of the Russian Federation). If such actions are detected, the law provides for a fine not exceeding 10 thousand rubles, which may also result in an administrative penalty in the form of a fine on an official in the amount of 300 to 500 rubles.