Inventory is an important procedure for each company. It is represented by the process of reconciling the existing property of the company with the information that is available in the documentation of the enterprise. The main objective of this process is the comparison of data and the identification of shortages. The timing of the inventory may vary significantly from company to company. As a standard, the process is carried out annually before annual reporting. Additionally, each leader at any time can issue an order on the basis of which an audit is carried out, if there are good reasons for this.

Procedure appointment

Each company must conduct an audit at a certain point in time. It should be carried out annually, but the exact timing of the inventory depends solely on the decision of the head of the enterprise.

The process is carried out by a special commission, which includes specialists from different departments of the company who are not interested in the results of the audit. The legislation provides certain cases in which an inventory is required.

During this process, various company documents are examined, which include agreements drawn up with contractors, inventory cards, invoices and other papers. The actual amount of different property should correspond to the information from these documents.

Inventory concept

It is represented by a unique instrument of control over all property values of the company. It lies in the fact that there is a comparison of data from documents with actual indicators. The process rules include:

- the main terms of the inventory are fixed in the legislation, but each head of the company can increase the number of inspections over a certain period of time;

- the procedure may be carried out in respect of fixed assets, materials or other values belonging to the firm;

- verification may be documentary or in kind;

- during documentary inventory, all objects are confirmed by special entries in the documentation;

- the in-kind check is used for inventories and fixed assets, therefore, due to this process, counting, measuring and overweight are performed;

- during the process, the presence of financially responsible persons is required.

Regardless of the type of inventory performed, an inventory of the verified property is compulsory. For this, uniform forms are used. The procedure and timing of the inventory can be fixed in the internal accounting records of the company.

Purpose of

When performing the verification, several goals can be achieved at once:

- identification of the actual amount of different materials or fixed assets;

- definition of shortage or surplus.

After the process, the obtained information is compared with the data that are available in the company documentation. This allows you to determine how employees of the company comply with the rules for using different property. If a shortage is detected, an investigation is carried out, the purpose of which is to identify the culprit, after which he is held accountable.

The main varieties of the process

The number and timing of the inventory are set only by the management of the company. At the same time, the direct director of the company determines which inspection will be carried out at one time or another.

In terms of property coverage, an inventory can be:

- Complete.All values and property belonging to the company are checked. For this process, a large number of specialists are included in the commission, since it takes a lot of time to obtain data and verify indicators. Often, the procedure takes several weeks. It is considered especially difficult if the company has several units in which an inventory is required.

- Partial In this case, only any specific values that are being studied are selected. For example, a check of fixed assets or materials may be carried out. Typically, such an inventory is assigned upon receipt of information that there is a shortage or other problems in reporting.

On the grounds of the inventory may be planned or unscheduled. At the beginning of the year, any company can draw up a special plan based on which the procedure is carried out. If it is required to change the person in charge or transfer the property for rent, an unscheduled inventory is performed. Employees of the company are not notified in advance about its implementation, and it is often with its help that the most reliable results are obtained.

How is the process performed?

The timing of the inventory is set by the direct management of the company, so they can vary significantly between firms. The procedure depends on what kind of material assets of the company are checked. But this uses a single algorithm by all firms.

The procedure and timing of the inventory is regulated by the enterprise, but if the tax inspection reveals that the company does not perform the process at least once a year, this becomes the basis for an unscheduled audit. The inventory procedure is divided into the following steps:

- training;

- counting values;

- comparison of the results with the information available in the documents of the company;

- registration of results in accounting.

Although these stages are considered quite simple, in fact, quite a lot of time and effort is spent on their implementation.

Preparatory stages

Initially, the timing of the inventory is determined by the management of the company. Based on the decision, an order is issued.

A commission is formed by the head of the enterprise, which will be engaged in direct verification. It is determined which objects will be examined. Responsible persons of the company send receipts to the management, and an inventory form is prepared for each member of the commission.

Property Count

The procedure involves performing various actions. These include counting, weighing different materials or measuring.

Specific operations depend on the characteristics of the values. All information received is certainly entered into a previously prepared inventory form.

Data comparison

The information obtained is compared with information from the documentation of the company. If different discrepancies are really revealed, then the commission performs the following actions:

- the reasons for the surplus or shortage appear;

- reveals who exactly is the culprits of such problems;

- surpluses are written off;

- perpetrators are held accountable.

This stage is considered long and difficult, since the commission members have to compare a really significant amount of data.

Reporting Results

The last step is to compile a report on the inventory. It includes all the results of the process.

Based on the compiled documentation, changes are made to the annual reporting of the enterprise.

Rules for

The basic inventory rules include:

- the timing of the inventory is determined by the management of the company, but the exception is a mandatory audit conducted annually;

- Only professionals working in the company should be included in the inventory commission, but they should not be interested in the results;

- Before verification, information on the receipt and expenditure of values is studied;

- during the implementation of the process requires the participation of financially responsible persons;

- for property stored separately, special inventories are formed.

The check is carried out on the day specified in the order of the head. The timing of the inventory of property can vary significantly, but in large companies this process often takes up to several days. At the end of each working day, the premises with the property confirming the audit must be sealed. Documents related to the inventory are stored in a special safe.

When is inventory required?

The types and dates of the inventory are covered by both the law and the management of the company. In some cases, such verification is mandatory. These include:

- the transfer of various values belonging to the company to other persons or firms for rent;

- sale of valuables;

- redemption of objects that were previously received on the basis of a lease;

- transformation of a unitary enterprise into a commercial organization;

- before the formation of annual reports;

- change of persons who are financially responsible in the company;

- various facts of theft or damage to property are revealed;

- emergencies in the company;

- company closure or reorganization.

The term of the annual inventory is fixed in the legislation, therefore, company managers must issue an order to conduct an audit before compiling the annual balance sheet.

Documentation Rules

The number of inventories and the timing of the inventory are determined by the direct management of the company. The process is always accompanied by the need to prepare numerous documents. These include:

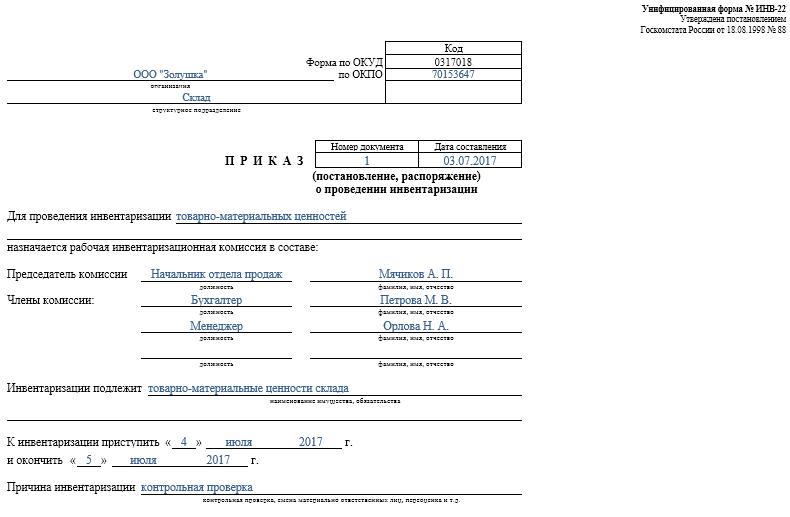

- Order. It is published by the head of the company before verification, for which the unified INV-22 form is used. Information about such an order is recorded in a special journal.

- Inventory of property. It is filled directly during the audit. A separate document is maintained for property under repair or temporarily transferred to another unit. Special inventories are made for leased property or valuables transferred for temporary storage.

- Collation statement. Its main purpose is the comparison of indicators. Therefore, there are recorded discrepancies between actual data and indicators from the accounting of the company.

- Statement of form INV-26. It is used to enter verification results.

As soon as the deadline for an inventory of fixed assets, materials and other property ends, the excess is written off in accounting. They are credited to income on the basis of market value, for which account 91 is used.

When shortages are identified, the culprits are initially identified, after which the necessary funds are collected from them to cover losses. If there is no opportunity to identify the perpetrators, then the shortfall is charged to production costs, for which account 94 is applied.

The results of the audit will certainly be reflected in accounting at the end of the month during which the inventory was carried out.

The practical benefits of the process

Inventory is considered an effective way to control the activities of the company, so all managers should be aware of its value. It benefits from the following features:

- it is guaranteed that all the information contained in the statements of the enterprise is reliable;

- the safety of various company values is controlled;

- various items are identified that have already expired;

- materials and elements that are not used by the company in the process of work are determined, therefore they are sold or leased for profit.

Based on the information obtained as a result of the inventory, it is possible to optimize the work of the company. Additionally, changes are made to the enterprise development strategy. Weaknesses in the functioning of the company are identified. In addition, negligent workers who do not have the necessary skills for the preservation of property are calculated.

Conclusion

Inventory is the most important process in any company. It allows you to identify different discrepancies between the actual amount of property and the data that are available in the reporting company. The timing and number of checks are set by the immediate supervisor.

Minimum inventory should be carried out once a year, namely before the preparation of annual reports. This ensures the availability of reliable data in the documentation.