Accounting is a difficult but necessary business in any business activity. Knowledge of all the subtleties and features in this area comes only with work experience. Many managers believe that having an accountant is the guarantor of proper accounting. And only after the dismissal of an employee, it turns out that the accounting was not kept in full. We have to carry out the restoration of accounting data.

Check

As you know, the problem is easier to prevent, so as not to waste time and money on the restoration of accounting and tax accounting. To do this, it is enough to conduct a small rapid test - compare the reporting data with the information in the program. If deviations are found, then the accounting is conducted with errors. The consequences can be unpredictable: from a counter check to the disqualification of a leader.

Mistakes can be made for various reasons: change of employee, lack of documents, workload of the department. Be that as it may, it is better to timely restore accounting and tax accounting. This will avoid penalties for non-compliance with the law and increase the effectiveness of the organization as a whole. Do not forget that for maintaining records in the organization, the head bears administrative or criminal liability.

Professional Services

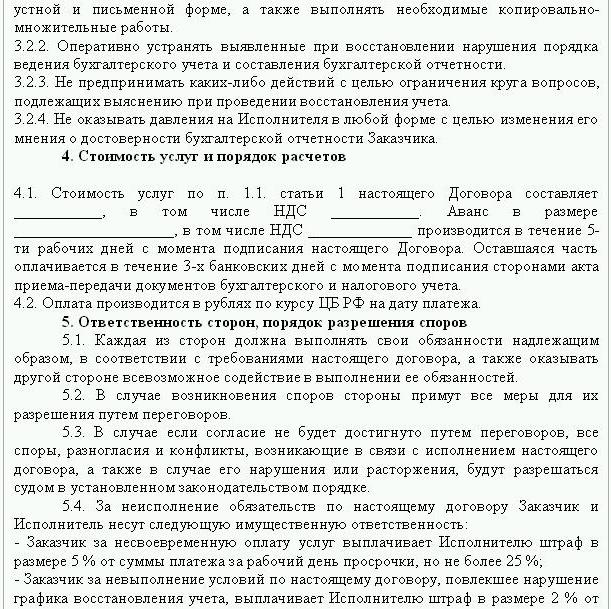

If reporting errors have been identified, then data recovery is necessary. In this case, an agreement is concluded to restore accounting, a sample of which is presented below. The document details the details of the parties to the transaction, the rights and obligations of the parties, the timing of the audit. It is very important to reflect in the contract the cost of services and the responsibility of the contractor for the performance of duties.

Creating a new legal entity makes sense only if the company is not responsible to other counterparties. If the company has valid licenses, long-term contracts and a large staff of employees, it is necessary to support its vital functions. Business experience and a positive business reputation also matter.

Accounting restoration services include:

- Analysis of the current state of the organization: accounting policies, workflow, chart of accounts.

- Reconciliation of settlements with all counterparties.

- Formation of a database of documents.

- Recovery of documentation and input of primary data.

- Reporting.

As a result, the documentation will be restored, streamlined and monitored. Accounting restoration services will be expensive. The price directly depends on the cause of the errors (shift of an accountant, the result of a tax audit, unqualified accounting) and the period for which reconciliation of settlements is necessary. The more errors are identified, the more work the auditors will have to do. On the other hand, the cost of services is much less than the costs that would be incurred by the company in case of improper accounting.

Targets and goals

The restoration of accounting by an audit firm begins with setting the goal - to bring the accounting into a state that complies with the law so that the regulatory authorities do not impose fines, claims and sanctions on the enterprise. Based on the goals and objectives, the following verification steps are carried out:

- Analysis of the current situation: initial processing of documentation.

- Determination of the scope of work, calculation of their cost, planning and coordination of events with the customer.At this stage, an agreement for the restoration of accounting is drawn up.

- Implementation of measures, including the creation, correction of accounting registers, primary documentation and reporting.

- Providing verification results to the customer.

Options

Where to start accounting recovery? With an analysis of the current situation and determining the amount of work. Full restoration of accounting by audit services may be required only if before accounting was not conducted at all or completely lost. Most often, partial data recovery is performed. which covers separate sections of a business unit, transactions or operations, verification of reporting and tax accounting for certain types of taxes.

Accounting Recovery: Where to Start

The first step is to take an inventory to determine the actual amount of fixed assets. Independent appraisers will determine the market value of the object and the period during which it worked. Based on these data, a balance is drawn up and the remaining life is calculated. Companies that are on the common system can find out the value of the object from a copy of the property tax declaration. Objects that are not taxed should be reflected in the appendix to the report.

If the company has real estate and land, then you need to contact the BTI and the registration chamber for copies of passports for these objects. You can check the information on the owners of the plots that are transferred to the organization on a rental basis at the Federal Registration Service. The property management committee has a charter of enterprises that own federal or municipal facilities. All data obtained must be recorded in accounting.

Recovery of fixed assets is carried out in the following sequence:

- An inventory card (OS-6) is entered for each object, which indicates the full name, residual value, a brief description and the remaining term of use.

- The cost of identified operating systems is reflected in DT01. According to KT02 “Depreciation” at the reporting date should be “0”. Indicate in these transactions the initial cost of the asset and the amount of depreciation is not recommended. Better reflect residual data. The remaining useful life of each facility should be established by the commission.

- If the company was established before 2002, then the report should include the approximate date of construction of the facility or its commissioning. According to these data, then the period of use in NU and BU will be determined. Until 2002, depreciation was deducted at different useful lives. The resulting permanent differences affect the amount of income tax.

- In the order on accounting policies should be prescribed a method of calculating depreciation.

Stocks

Next, an inventory of inventories should be carried out by recounting and weighing goods in warehouses. According to the results of the audit, the accountant:

- Reflects on DT10 the identified stock balances, and on DT41 - the remains of goods. Registration is carried out in quantitative and total terms at market value.

- If, according to the results of the inventory, overalls were found, then it should be recorded in separate cards. One document is written out for one responsible person. If the useful life of the clothing exceeds 1 year, then depreciation should be accrued on a monthly basis.

- In the order on accounting policies, the procedure for reflecting and disposing of goods and goods to the NU and BU MZP should be fixed.

Settlement data collection

Recovery of accounting documents begins with determining the stage of mutual settlements with all counterparties. Copies of all payment documents can be obtained at the bank by providing the details of the organization. In this case, a letter is drawn up in the name of the head of the department with a request to provide account statements from the archive with all attached files. Information must be restored at least six months in advance.From the documents provided, it will be possible to easily identify suppliers, buyers and balances on the current account. The next step is to send a reconciliation report to each agent and ask them to send along with the signed documents copies of all the agreements.

The FTS monitors the accrual and payment of taxes on time. To this end, the tax compiles business accounts cards, which reflects payments:

- for the current year;

- for repayment of debt for the previous period;

- on account of repayment of restructured debt;

- proceeds from the sale of seized property.

In order to restore accounting, the auditor or accountant sends a letter to the Federal Tax Service with a request to provide a reconciliation report. The document must necessarily indicate the TIN, the location of the organization, phone number, and the name of the head. The Federal Tax Service draws up an act in the form of No. 23 and sends it to the client. In addition, you can get a statement on the status of settlements with the budget. It is issued at the request of the taxpayer, drawn up in writing, or transmitted to the email address. The deadline for receiving the document is 10 days from the date of filing the certificate.

Each enterprise is required to register with the FIU and the FSS. From these institutions you can get copies of the declaration on the payment of UST and insurance premiums and find out the balance of payments, the amounts paid, whether a regressive scale is applied, whether there are people with disabilities in the enterprise.

On a quarterly basis, the company submits a balance sheet with all additions, a statement of profit and cash flow. Copies of these documents for several previous periods can be obtained from the FTS upon written request.

Calculations

The restoration of the accounting of firms under this article is formed from the reconciliation acts in the BU and is reflected in account 60:

- debit - if there is an overpayment to suppliers;

- credit - if there is a debt to suppliers.

If the organization uses the services of only a few counterparties, it is recommended to open sub-accounts separately for each counterparty to detail the calculations.

All settlements with customers are reflected in account 62. Debt of the counterparty is in debit and overpayment is in credit. In the same way as with suppliers, settlements with each buyer can be carried out on a separate sub-account.

Maintenance, restoration of accounting for non-cash funds is carried out on the basis of data from bank statements. Residual grease on current accounts is reflected in ДТ51. If the organization has balances of currency values, they are accounted for before DT52, converted into rubles at the Central Bank rate on the date of the inventory. Cash on hand is recorded in accordance with DT50.

The restoration of accounting and reporting with the FIU, FSS, MHIF is carried out on the basis of reconciliation statements received from these institutions. All amounts are accounted for in account 69, to which the corresponding sub-accounts are opened, reflecting the UST calculations in the part transferred to the Social Insurance Fund, the federal budget, for medical insurance and calculations for contributions to the Pension Fund. The amounts reflected in the act must coincide with those indicated in the payment documents from the bank. Identified discrepancies can be caused by the fact that funds are transferred to the account in the budget a few days after they are transferred. An error could be made in the payment documents, then the funds are credited to another account. In any case, when identifying deviations, it is recommended that you contact the FIU or the FSS for clarification.

The balance of account 69 will be:

- Credit, if the amount of accruals exceeds the amount of payment.

- Debit if funds are transferred to the budget in advance.

- Zero if overpayment and no debt.

Reconciliation acts with the Federal Tax Service will help you find out which taxation system the organization is on. The balance indicated in the documents should be reflected in the accounting statement on account 68.

Organization Capital

Where does the restoration of accounting begin within the organization's funding sources? With the constituent documents of the enterprise. The Charter shall indicate the amount of funds contributed by the founders. All subsequent changes in the amount of capital should be reflected in the minutes of meetings of shareholders. The calculated amount of the authorized capital should be reflected in KT80.

Balance: assets

To recover data, you need to get the last report submitted to the Federal Tax Service. Information in the balance sheet is recorded from the General Ledger. If it is absent, then the restoration of accounting firms is carried out on the accounts.

NMA (p. 110). If there is a certain amount on the accounts, then you need to find out from the management what trademarks or intellectual property the company owns. Appraisers will help to correctly determine the value of such objects.

OS (Art. 130). For enterprises engaged in construction, this line reflects the cost of equipment for installation and invested in intangible assets. If there is a balance sheet on page 135, then the organization has property leased. To restore accounting data, you need to request a lease.

Special accounts in banks (p. 140). This line shall reflect the amount of investments in short-term deposits. Floor information should be reflected in the bank statement and on account 55 of the general ledger.

Stocks (p. 211). Information on the quantity and cost of materials is recorded in the balance sheet according to the inventory. Figures may differ from those presented in the last report submitted.

The balance sheet shows the amount of tax received on transactions with all counterparties. If the company has many buyers, the amounts indicated on p. 220 (VAT) and 230 (DZ) will not help to restore accounting.

Data on funds at the cash desk and on settlement accounts are filled out based on bank statements.

Balance: liabilities

The amount of the constituent capital (p. 410) must correspond to that indicated in the constituent documents.

If the organization uses short-term loans. then their volume, including interest, should be reflected in the account. 66. Debt to the Pension Fund, social funds (p. 623) and the budget (p. 624) should correspond to that indicated in the acts of reconciliation with these organizations.

Deferred income (p. 640) include the amount of rental income, gratuitous assets, etc.

The total amount of leased fixed assets indicated on pages 910 and 911 must correspond to that indicated in contracts with counterparties, and monthly payments - with bank statements. Debt owed to lessors should be shown on off-balance sheet account 001.

After all the data from the balance sheet is posted, the restoration of accounting is where to start? If all data is entered correctly, then the debit balance of accounts and sub-accounts must coincide with the credit.

Income tax return

Accounting Recovery Where to Start? Data from the declaration should be reflected in the balance sheet of the organization, taking into account such nuances:

- Section 1 shows the amount of tax payable throughout the organization as a whole. This should be taken into account if the company has units that do not pay tax. The balance of account 68 must coincide with the amount of debt transferred to the local budget (p. 091) and the budget of the Russian Federation (081).

- Tax payable on dividends and interest on state securities is reflected in subsection 1.3 in pages “1” and “2”, respectively.

Consider filling out the remaining lines of the declaration:

- Page 070 - income from operations with debt obligations and from revaluation of the Central Bank.

- Page 010 - the amount of the organization’s revenue for the reporting period.

- Page 100 - non-operating income received in the form of interest on loan agreements, bills of exchange and other debt obligations.

- Page 041 - the amount of taxes and fees with the exception of the UST.

- Page 050 - the cost of acquired (realized) property rights in the past period.

- Page090 - the amount of losses for previous periods for service industries.

- Page 400 - the amount of accrued depreciation for fixed assets and intangible assets. If it differs from the calculated one, then the organization has objects acquired before 2002, which are now listed in a separate group.

- Page 030 - the amount of operating systems implemented in the previous period. You can determine the objects sold under the agreements recorded in the registration chamber. The depreciation amount for such objects is recorded on page 040, and revenue is included on page 030.

Possible mistakes

Restoring accounting and auditing is a long and painstaking process. The main problem is that the information from the statements will not coincide with that indicated in the reconciliation acts. First of all, this applies to all budget payments. For example, the auditor received an act on December 31. Charges are accrued in the balance sheet at the end of the month, and in the personal account from the Federal Tax Service - at the due date, that is, at the end of the 1st quarter of next year. If the organization transfers funds to the budget on a quarterly basis, then they will be listed as deducted in the accounting department, and according to the Federal Tax Service, they will be charged as advance payments. That is, at the end of the year, identical calculations will be only for 10 months without taking into account advance payments for the last quarter. The same situation will be with other reporting periods.

You can not throw out documents on the basis of which data recovery was carried out. They need to be collected and compiled in one registry. Responsibility for the safety of primary documents lies with the chief accountant.

Tax reporting may not be completed correctly. In addition, the organization has events that occurred after the reporting date, but before signing the document with the Federal Tax Service. If they were not correctly taken into account, then in the current period there will be a loss of material values by a large amount.

The regulation on the management of accounting allows the preparation of a balance with inaccuracies. The balance sheet shows the minimized credit and debit balance.

Loss of documents

If the documents were partially lost, then the company is in a better position, since it will not have to restore all accounting from scratch. Good results are obtained from conversations with management, accounting staff and other economic departments. In order to avoid such cases, it is better to periodically make archival copies of the accounting base in the form of printouts of WWS at the end of the month.

Controller selection

After all restoration work has been completed, it is worthwhile to exclude a key error - not a qualified employee. When hiring an accountant, one should test his knowledge in the field of activity of the enterprise and his skills in working with the program. Very often, “specialists” do not understand the database settings and generate reports based on the program. But not all configurations can be configured.

You should also decide in advance on age preferences. Young specialists have a large amount of theoretical knowledge and few practical work skills. Although they are determined to break into battle, it is not worth relying on them. At the same time, the “grandmother-accountant” will spend more time studying legislative changes than on adapting accounting in a company.

According to statistics, 80% of employees work well only if their work is controlled. The best way is to periodically withdraw reports on the main accounting accounts: “stocks”, “settlements with suppliers, customers”, etc. If the numbers on the accounts are in doubt, you should ask the accountant to comment on the situation. Any errors should be corrected immediately. If the accountant cannot cope with this task on his own, then you will have to turn to specialists - auditors.