Almost any legal entity has the right to create and close separate divisions. Moreover, quite often such a structural unit is opened temporarily, for the implementation of a specific project. However, the procedure for closing a separate unit has a number of features that you should be aware of.

General Provisions

A detached unit may in no case be located at the location of the parent company. The unit must have stationary workplaces (at least one) and exist in fact for at least one month.

Such a division of the company may be formed in the form of a representative office, branch or in any other form (warehouse, store, second office or workshop).

Closing a stand-alone unit: step-by-step instructions

Depending on the type, the liquidation procedure may vary slightly, but in any circumstances, business owners will have to solve a number of issues:

- HR

- property;

- administrative.

It is mandatory to notify the tax service of the closure of activities in the unit. On the other hand, there are no special requirements at the legislative level for such formations, although there are some discrepancies in terms. So, for example, that a decision on liquidation has been made, the Federal Tax Service should be notified within three days, and employees in 2 months.

In practice, before making a decision on liquidation, they not only notify employees, but also conduct an inventory and audit. After all, it is very important, especially if the unit is located in another city, to know exactly what material assets are available and what will be transferred to the main office. At the same time, not only values are subject to inventory, but also debts, fixed assets. It is possible that the business owner wants to check the payment of taxes and fees.

As a rule, a special commission is created at the main enterprise, which checks the balance sheet and conducts an inventory. Such a check will allow to find out and fix the values that are supposed to be sold after the liquidation of the unit.

Stage number 1 - personnel issues

Due to the mismatch in terms, it is still recommended to begin the procedure for closing a separate unit by resolving the personnel issue. After all, it is very important to comply with all the requirements of the current labor legislation, especially since the unit must have at least one stationary workplace, therefore at least one employee.

Depending on where the structural unit is located, the procedure will differ. If the office or warehouse is located in another region, then the workers will have to be fired according to the reduction procedure, or they should be offered a job at the location of the head office. In this case, employees of the upcoming dismissal must be notified in 2 months, to pay them severance pay in the amount of one-month salary. In the future, for three months, if the employee does not get a new job and is registered with the employment center, the enterprise will pay him the average wage for this entire period.

If the closure of a separate division takes place in the same region where the main office is located, socially vulnerable segments of the population cannot just be dismissed. These are pregnant women, parents with many children, if the family has children under 3 years old, single mothers or fathers.

Stage number 2 - decision making

It is possible to make a decision that liquidation is ahead at the general meeting.For some enterprises, this function is assigned to the board of directors. Based on the decision to close a separate division, the enterprise management issues an appropriate order confirming the liquidation.

Stage No. 3 - preparation of documents for notification of the IFTS authorities

Within 3 days from the date of the decision, the company management is obliged to apply to the tax service with a corresponding notice. For this procedure, a special form C-09-3-2 is provided. Filling it is quite simple, but it is presented with just two sheets. The first sheet shows all the identification data of the enterprise, from the PSRN to the TIN. The second sheet contains information about the location of the branch, which is subject to closure, the date of the decision.

The current closing form of a separate division can always be downloaded on the website of the Federal Tax Service. You can fill out the form either by hand or using a computer. When filling out on a computer, it is recommended to choose a standard font - Courier New, with a height of 16 to 18 points. If the form is filled in by hand, then it is necessary to write in capital letters, and where blank cells remain, put a dash.

The main thing to remember is that if several sheets of the form are filled out, then at each of them it is imperative to fill in the TIN and KPP column.

In cases when several divisions are simultaneously closed, for each of them a separate notice on the closure of a separate division is not compiled, but only the second sheets for each branch are filled out. The corresponding sheet is marked on the first sheet of the form, which immediately closes several departments of the enterprise.

If the charter of the enterprise has not changed since 2014, then you will have to make changes to it. Until September 2014, without fail, the charter of the enterprise should contain information about all divisions, now no such requirement is put forward. That is, if the charter has not changed for a long time, then form P13001 is additionally filled out, if there are no changes, then form P14001.

As a result, the following documents are submitted to the tax service when closing a separate division:

- form C-09-3-2;

- the decision of all participants in the enterprise, or a single participant;

- Form P13001 or Form P14001, as appropriate;

- in the new edition of the charter (if amendments are made to it);

- document confirming the state duty (this year its amount is 800 rubles).

For violation of the deadlines for the provision of information on the upcoming liquidation of the company, an administrative fine may be imposed, but, as a rule, tax specialists only manage with a warning.

Stage 4 - filing tax reports

Depending on the chosen taxation system, it is necessary to file a declaration for a separate division. If the branch had a bank account, then it should be closed.

Stage number 5 - deregistration

A unit cannot be considered liquidated until the Federal Tax Service Inspectorate has sent a notice that it has been deregistered. Regulatory documents for this provide a 10-day period. But in practice, inspectors may wish to conduct an on-site inspection.

But the obligation to send an application to close a separate division to all funds has been removed from enterprises. This function is now assigned to the tax service.

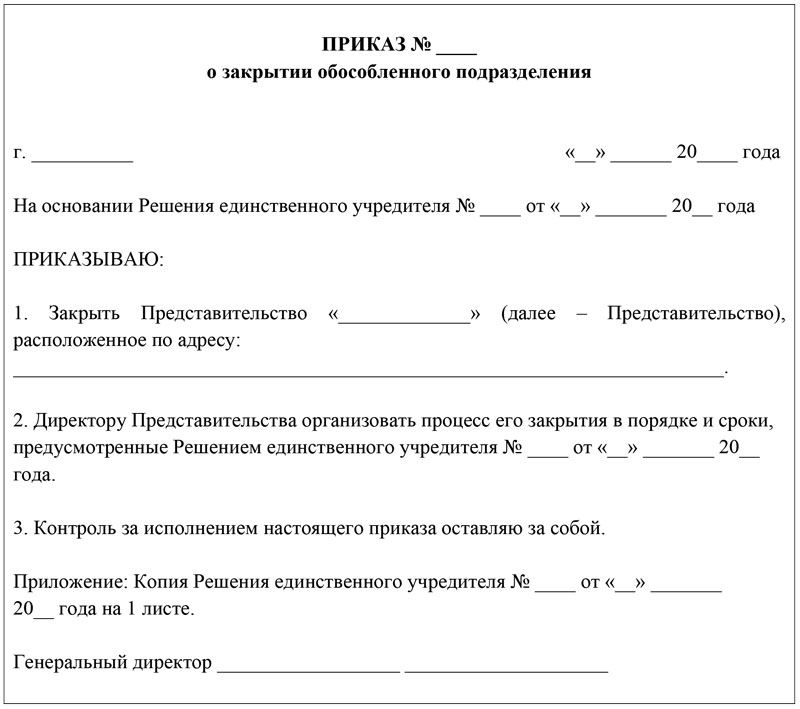

Rules for drafting an order

Any responsible person for the liquidation procedure of the branch can draw up the order, but the director must sign it. In the text of the document must necessarily be present two parts: justification and basis.

Justification is the real reason why the unit closes, for example, production necessity, loss-making or reorganization.

The basis is a reference to a regulatory or local document, according to which, the liquidation procedure has begun. It may even be a decision of the founder or board of directors.

The order to close a separate division must be registered in the register of general administrative documents. If specific positions are mentioned in the document, they are required to perform certain tasks, then these employees should be familiarized with the order under signature.

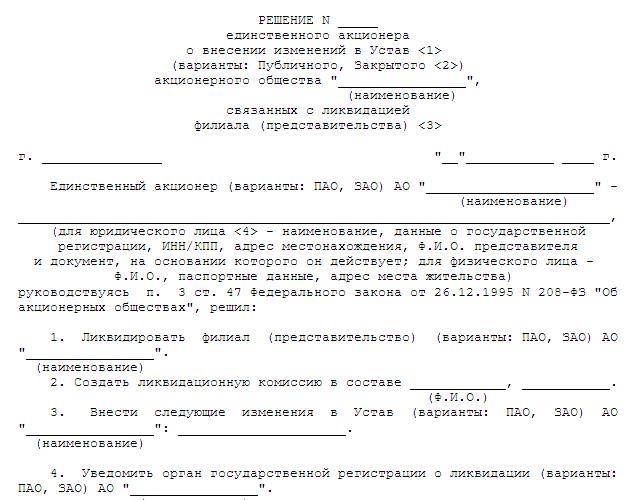

Liquidation decision

Most often, the opening and closing of a separate division is referred to the competence of the general meeting of shareholders. However, the law does not prohibit the delegation of such powers to the executive body. AOs usually have such rights with the board of directors. In any case, even if there is only one participant, the decision and protocol must have the following mandatory details:

- Full name of the parent company.

- Place and date of decision.

- The serial number of the document.

- Information about the founders or one member. If there are several founders, it is necessary to indicate the size of their shares.

- Next, an agenda is set out, which indicates not only the issue of liquidation, but also the issue of approving the new edition of the charter (if they are introduced), the issue of appointing an authorized person for conducting registration activities.

- Estimated times for liquidation

At the end, the document is signed by the secretary and chairman, or a single member of the company.

Distinctive features of the closure of the enterprise and division

The most important distinguishing feature is that a separate division does not have such a wide range of rights and obligations as an ordinary legal entity. After all, even if the branch is closed, the main office continues to work, and all property belonging to the unit automatically passes into the enterprise. And if the unit had violations in the field of taxation, then the head office will have to answer.

The closing time of a separate division is much shorter than during the liquidation of an enterprise. Indeed, in this case, it is not necessary to create a liquidation commission, form an interim and final liquidation balance sheet, submit notifications to the media, etc.