A construction co-investment agreement, a sample of which will be presented later, is usually executed by enterprises engaged in the construction of facilities with insufficient funds to continue work. According to such an agreement, after the completion of the measures and obtaining permission to put the facility into operation, part of it is transferred to the entity that financed the project, in proportion to the amount paid. Let us further consider the features of such a transaction.

Specificity of taxation

In practice, it is widely believed that a co-investment agreement for the construction of a non-residential building or multi-apartment building saves the entity that has accepted the funds from including them in the VAT base. This position is determined by the norms of the Tax Code. In particular, Article 39 of the Code states that the disposal of property of an investment nature is not considered a sale for tax purposes. The relevant provision is secured in sub. 4 p. 3 norms. Meanwhile, in this subparagraph there is a list of operations that have an investment nature. Among them:

- Contributions to the capital of business partnerships and companies.

- Mutual contributions to cooperative funds.

- Deposits under simple partnership agreements (on joint activities).

These operations are long-term in nature. The co-investment agreement for the construction of a residential building or industrial structure involves the transfer of the object in exchange for money or other property. In the sense of the rules, such an operation should be recognized as an implementation for tax purposes.

Terminology

There are no provisions in the law that clearly disclose what a construction co-investment agreement is. The sample document is also not described by the rules. Among the whole variety of definitions proposed by specialists, the most appropriate is the following. Co-investment agreement - an agreement involving the investment of money and other property for the purpose of subsequent profit.

Turn to the law. As the law of the RSFSR No. 1488-1 indicates, investments are recognized as investments in the object of economic activity for profit. This definition is present in 1 article. Paragraph two of the same norm states that investment is considered practical activity aimed at the sale of invested funds. Federal Law No. 160 refers to foreign capital. Foreign investment, according to Section 2 of the law, is considered the investment of foreign currency in the object of economic activity within the Russian Federation.

Some experts, analyzing the current standards, propose to officially fix the definition of an investment (co-investment) agreement. However, most experts believe that this is impractical. Taking into account the provisions of laws No. 1488-1 and 160, it can be said that any agreement aimed at making a profit is considered as a co-investment agreement.

Federal Law No. 39

This normative act defines investment activity in the narrow sense. Federal Law No. 39 deals with capital investments, that is, actions aimed at making profit in the long term by operating the OS created by the organization. The law also does not disclose such a thing as a co-investment agreement. The normative act gives a reference to the Civil Code. It follows that for an entity that will eventually register a constructed or acquired facility as an OS, any agreement entered into during the construction process will act as a co-investment agreement.

Accounting

In PBU 23/2011 there is a definition of investment activity. Clause 10 states that those operations associated with the acquisition, creation, disposal of non-current assets are recognized as relevant operations. These include:

- Costs of the purchase, construction, modernization, reconstruction, preparation for the operation of assets. They include, among other things, the costs of research and development, technological work.

- Sale of non-current assets.

- Calculation of interest on liabilities included in the cost of investments, in accordance with the provisions of RAS 15/2008.

- Payments related to the purchase / sale of shares / shares in other companies. The exception is financial investments that involve resale in the short term.

- Issuance of loans to other entities or their repayment.

- Acquisition / sale of debt securities, except for investments acquired for subsequent resale (in the short term).

Thus, the PBU refers to transactions with non-current assets. These include OS, intangible assets, long-term investments. Given the provisions of Federal Law No. 39, it should be noted that a co-investment agreement for the construction of a residential building or industrial structure is an agreement involving a change in the size of non-current assets, which are reflected in 1 part of the asset balance.

Nuances

Not always a co-investment agreement is such for a partner. If an operating system is purchased, then it can be sold not only (used), but also products (goods). For the acquirer, the contract will be investment in any case. As for the seller, it all depends on the object that he implements.

When drawing up a contract agreement for the construction of fixed assets, an investment contract is necessary exclusively for the customer. It does not matter to the contractor how the counterparty will accept the constructed facility for accounting. The customer can reflect it as a fixed asset or as property intended for further sale (i.e. as a finished product). For the contractor, the agreement relates to ordinary activities.

If we talk about the memorandum of association for the formation of a new enterprise or the purchase of a share in the capital of an existing company, then for the owner of the funds it will be investment. For the company itself, the agreement can be recognized as such only when its fund is paid by the OS. In this situation, the debt of the founder will be repaid by a non-current asset.

YOU Opinion

In one of its decisions, the court determined how it is necessary to interpret the agreement on co-investment of a residential building or industrial structure. It is worth saying that in practice this agreement has a variety of names. The interpretation proposed by YOU has nothing to do with such a concept as a co-investment agreement. The re-qualification of an agreement is determined by a number of circumstances. First of all, it is caused by the need to clarify the purpose of the agreement for tax purposes. YOU proposed the following. Agreements related to investment in construction should be referred to as contracts of sale of future real estate. Accordingly, the tax authorities regard such transactions as the sale of property. As a result, the investment contribution is considered as an advance payment, which will subsequently be taxed with VAT, according to Article 154 of the Tax Code (clause 1).

It is worth saying that before the adoption of the decision of the Supreme Arbitration Court, the payers were guided by the provisions of paragraph 3 of Article 4 of the Federal Law No. 39. The norm states that a customer who does not act as an investor has the right to use, own, dispose of capital investments for a period and within the powers stipulated by the contract. As can be seen from the wording, the entity does not receive ownership of the funds received from the outside. Accordingly, the type of agreement was established - an agency agreement.As a result, the transfer of funds or other property was not associated with the further implementation of the structure and did not act as an object of taxation. Providing the investor with the real estate in which he invested was also not considered a sale.

Currently, the situation is different. It should be noted that in the decision of the Supreme Arbitration Court several agreements are named that can be used as part of relations to finance the construction of the facility. However, the agency agreement is not applicable to them. This is due to the fact that, according to the decree, the ownership of the object can arise only from the owner of the site.

Co-Investment Agreement: Postings

Consider a situation where the share of the completed facility will be operated by the entity that financed its construction for production activities, leasing or management needs. How is a co-investment agreement reflected? The postings will be as follows. By db count 08 formed the value of the object. It can be charged to the account. 01 "OS" or cf. 03 "Profitable investments". The formation of the initial cost is carried out in accordance with RAS 6/01. In some cases, borrowed funds are used to create an object. Then the accountant must take into account the provisions of PBU 15/2008.

As paragraph 7 of the rules indicates, the cost of an asset should include interest that is due for deduction in favor of the creditor and is directly related to the acquisition, manufacture (construction) of the object. When compiling postings under a co-investing agreement with a co-investor, an accountant should remember that borrowing costs can evenly be included in other expenses throughout the life of a debt.

Special cases

If the construction of the facility was suspended for a long period (more than 3 months), the inclusion of the interest due to the creditor in the construction cost ceases from the first day of the period following the month in which the event occurred. For this period they should be written off to other expenses. In case of resumption of work, accrued interest is transferred to the value of the asset. The period during which the additional coordination of the organizational / technical issues that appeared after the start of the construction of the structure will not be considered a suspension period.

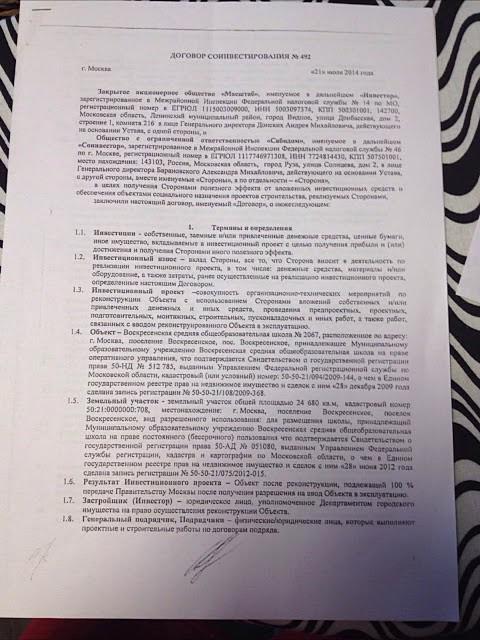

Co-investment agreement: sample

The agreement is drawn up according to the general rules provided for documents of this type. The standardized form is not approved by law. However, the rules provide for mandatory details that must contain all agreements, including a co-investment agreement. A sample document includes the following information:

- Names of the parties.

- Date and place of transaction.

- General Provisions

- Subject of the agreement.

- Rights and obligations of participants.

- The cost of the agreement.

- Responsibility of the parties, including in case of unilateral refusal to fulfill the terms of the transaction.

- Force Majeure.

- The validity period of the contract.

- Final provisions.

- Details of the parties to the transaction, their signatures, stamp imprints. If a co-investment agreement is concluded with an individual, then his passport details, address of residence, full name are given.

To declare a transaction valid, a written agreement must be followed. State registration of a co-investment agreement is not provided for by law. Without fail, the agreement must indicate all material conditions. These include, in particular, the definition of the subject of a transaction. For example, a co-investment agreement is drawn up for the construction of a non-residential building. The model agreement should include information by which the object can be uniquely identified.

Important point

Before making an agreement, the entity planning to finance the construction of the facility should check the counterparty’s solvency.If the second participant who has entered into a construction co-investment agreement (builder) is bankrupt, a lawyer is needed to resolve the situation with the least losses. As a rule, it will not be possible to solve the problem peacefully. Will have to contact the court. In this case, it is necessary to take into account the norms of legislation governing the bankruptcy procedure.

Revaluation of tax liabilities

If the relationship is not regulated by a contract of partnership and a simple partnership, the value of the property that is transferred by the investor for the construction of the facility is subject to VAT, calculated at a rate of 18%. In this case, questions may arise in the accounting of expenses and taxation by the owner of the site. Control authorities may consider the funds transferred by the investor as the income of the developer. According to the law, they can be reduced by documented expenses. From this it follows that entities participating in such transactions should reassess their tax liabilities for VAT and deduction from profits. Such operations must be carried out both under the planned and already concluded agreements, taking into account the statute of limitations (three years) for conducting inspections of the Federal Tax Service.

The specifics of the reflection of funds at the recipient

In considering this issue, attention should be paid to subparagraph 23.1 of paragraph 3 of article 149 of the Tax Code. In accordance with it, VAT is not charged on the services of the developer provided by him, according to the contract of shared participation in the construction. This agreement is drawn up taking into account the provisions of Federal Law No. 214. An exception is the work that the subject carries out as part of the construction of production facilities. The funds received from the co-investor must not be reflected in the form of targeted financing, investment contribution, etc., on the balance accounts 76/86, but as an advance payment under the purchase and sale agreement on the account. 62. This money must be included in the tax base for VAT.

Harmonization of Terms

There are cases when, at the time of signing the agreement, the parties have not decided which part of the structure will be transferred after the work is completed to the project sponsor. Contractors may decide that the separation will be carried out after completion of construction. Thus, the entity that transferred the funds, learns about the parameters of the object actually bought by him, only at the time of execution of the acceptance certificate. In this case, the co-investment agreement they have concluded should still be interpreted as an agreement on the sale of a future object.

Recipient accounting questions

After drawing up a co-investment agreement, the developer, during the construction of the structure, conducts two types of activities. He creates a part of the object for himself. In other words, the developer makes capital investments in the OS. The second part of the facility is being built for subsequent reimbursable sale to a third party. In this case, we can talk about creating finished products (albeit immovable). If you strictly follow the requirements of accounting, the cost of constructing a fixed asset must be concentrated on the balance sheet. 08, and the cost of manufacturing the product - on the account. 20.

Meanwhile, such a separation in the construction process can only be done theoretically. In practice, such a differentiation is impossible, especially when the partners have not decided which rooms will go to whom. Moreover, under the terms of the agreement, it may be provided that all costs for the facility are accepted by the developer after obtaining permission to put the facility into operation.

Until then, the accounting registers will reflect the amounts transferred to finance the work. According to some experts, these funds should be reflected in the balance sheet. 60.

Conclusion

Legal constructions of various agreements, including co-investment, were created primarily to evade entities from paying VAT. The situation has changed YOU.By re-qualifying the co-investment agreements in the purchase and sale agreements of the future object, the court actually provided the tax authorities with the opportunity to replenish the budget with funds received by developers from their partners. Meanwhile, as experts say, the changes introduced have affected the consequences arising from such transactions on both VAT and deduction from profits.

The main feature of co-investment agreements is the fact that the funds received in favor of the developer do not become its property. He does not have the right to dispose of them at his discretion, but is obliged to send them to the construction of the facility. Accordingly, the funding received is targeted. Within the meaning of the norms of the Tax Code, these funds do not change the base for deduction from profit and are not taken into account when calculating VAT. It seems that the legislation should clarify this issue.