In the process of accounting, it is necessary to clearly identify what relates to fixed assets and working capital. Not only the economic side of the issue depends on this, but also the correctness of the documentation. So, we will understand what are fixed and circulating assets and what is their fundamental difference.

Fixed assets

In economic theory, this concept means all the material and technical values due to which the production process can take place. They act exclusively in kind, and their cost is reimbursed in equal parts during operation, the time of which is at least one year.

In turn, fixed assets are a significant and always significant part of the property. Without them, it is impossible to open an enterprise, and they are the main participants in any process that leads to the final result - the sale of products or services. Fixed assets include all buildings, machinery, equipment, etc., which makes up a considerable part of investments at the initial stage of the enterprise life cycle.

Current assets

Working capital - this is material values expressed in monetary form, which directly participate in the production process, but only once. They completely transfer all their cost to the cost of production. For example, fixed assets include machine tools and workbenches, thanks to which the production process is carried out, and working capital - materials and raw materials, without which nothing will be realized.

Working capital is almost always expressed precisely in cash and is used to conduct continuous activities.

Differences in working capital from fixed assets

- Fixed assets include: furniture, buildings, machines, which, although they are directly involved in the production cycle, do not transfer their elements to finished products. Working capital is included in the final result in full and without balance. They are consumed in a single completed cycle.

- The cost of those and other funds is included in the prime cost with only one difference: fixed assets in the form of depreciation are only partially displayed on the price, but working capital is included in full. Indeed, the final retail price for the consumer mainly depends on the cost of raw materials and materials.

- Capital resources can be replaced only after full reimbursement of their value. This sometimes takes several years. Current assets are sold immediately, which means they need to be bought for the next production cycle.

Classification of fixed assets

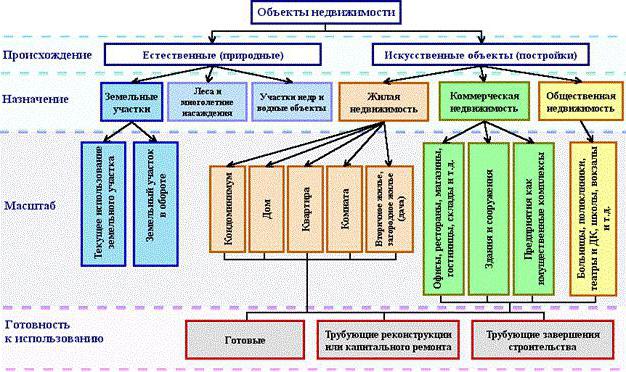

As for the classification of fixed assets, they can be distributed in different ways. In accounting, distinct categories are included in the balance sheet. In general, fixed assets in budget accounting include the following categories, presented in the figure below.

Almost all real estate objects have only two sources of origin: natural and artificial. Fixed assets of the enterprise include all land plots on which production stands, or which themselves are a source of finished products. So, the forest gives a tree, and the field - rye. Water objects and the bowels of the earth also fall into this category, although it is difficult to evaluate them, but the enterprise still needs the initial costs of buying a particular site to start operations.

Artificial buildings can have several purposes: housing, commerce or social real estate. Services also have their own fixed assets, and most often they are precisely the latter category, which includes buildings of kindergartens, schools, shelters, libraries, etc.

Own and leased funds

It is easy to guess that all own funds are the material and technical means that were purchased at the expense of the enterprise itself and are included in the book value. Rentals are accounted for a little differently. Depreciation costs are not calculated for them, and they are assigned “to the balance sheet”.

This question concerns budget organizations. Almost all available equipment is considered leased, because the company cannot use it of its own free will, as it pleases.

How to determine whether an item relates to fixed assets?

The question often arises whether the computer belongs to fixed assets? So, we will consider what criteria he meets and what not. To do this, answer a number of questions:

- Is the computer used for more than a year?

- Is he directly involved in production?

- During the cycle, is it fully used, transformed or processed, changes shape for the manufacture of the final product?

The first question implies the answer is yes. Naturally, the company will use the smart car for more than a year, and its cost will be evenly distributed in the form of depreciation for the entire life of the intended operation. We answer “no” to the second and third questions, which means that the computer cannot belong to current assets. We conclude that the PC belongs to the capital fund. Thus, you can determine what relates to fixed assets in accounting, and what does not.

What can not be defined under the category of fixed assets

There are a number of items that have been practically used for more than a year, I take an indirect part in the production process, but they cannot be called fixed assets. This category includes the following material and technical values:

- Tools designed for fishing and seafood.

- tools and accessories that complement the basic equipment and are used for individual and rare orders. Fixed assets include conveyors and machine tools, but not rolling rolls, shuttles, catalysts and sorbents.

- Uniform of employees, clothing of medical staff, bedding.

- Temporary buildings, for example, on construction sites.

- Items and structures created exclusively for their further lease.

- Animals considered young.

- Perennial plants used exclusively as planting material for young shoots.

- Forestry tools: chainsaws, loppers, wire ropes, temporary seasonal roads, small buildings and mobile homes, whose service life does not exceed two years.

Features of budget organizations

The main tasks that are put before the budget organization are the proper recording of all manipulations with real estate and the preparation of relevant documents in accounting. The issue is governed by paragraph 32 of Instruction No. 107.

According to this provision, fixed assets in budgetary organizations include items and material and technical means that fit into the categories:

- the term of use is supposed to be more than 1 year;

- initial cost of at least 50 minimum wages.

This category includes such groups of objects: buildings and structures, data transmission devices, utilities, work equipment, measuring instruments, computer equipment, office equipment, organization-owned vehicles, tools and equipment, livestock, various plantings, roads for internal use, etc.

Features of accounting for fixed assets in budgetary organizations

As stated in the legislation, a budget organization has the right to dispose of this property, but not to sell it. All income from its use goes to a separate balance sheet and remains in the power of the organization. Therefore, there is a feature of accounting for property displayed in the balance sheet.

The main account "01" - Fixed assets. His subaccounts:

- 1 - designed for those items that were purchased for budget money.

- 2 - property acquired as a result of entrepreneurial activity.

- 3 - values accepted as a gift.