Profitability is the main goal of all commercial enterprises. Without it, a business cannot survive in the long run. Thus, when measuring financial flows, profitability and forecasting future profits, profitability is a very important indicator.

What is profitability?

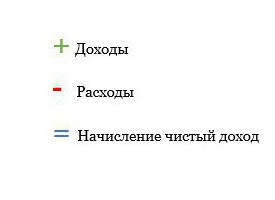

Profitability is such a use of funds in which the organization not only covers its costs with revenues, but also makes a profit. Profit and profitability of an entrepreneur are measured through income and expenses. For example, if crops and livestock are grown and sold, then, respectively, their owner (for example, a farmer) receives income. It is important to understand that money comes into the business from activities, while borrowing does not create income. This is just a cash transaction between a businessman and a creditor, with the help of which the first receives money from the second for the functioning of the business or the purchase of assets.

Costs - this is the cost of resources used (or consumed) in the business. For example, corn seeds are a farm resource, as they are involved in the production process. Expenses are funds spent, for example, on the purchase of a new vehicle, if the car, useful life which - more than one year, was disabled in less than a year. However, repaying a loan (as well as obtaining it, as mentioned above) does not count as expenses, since it is simply a transfer of funds between a business and a lender.

P & L

In order to find out what profitability is, you need to understand the concepts of profit and loss. This is essentially a list of income and expenses over a certain period of time (usually a year) for the entire business. Information on financial flows includes a simple analysis of profit and loss.

The profit statement is traditionally used to evaluate the profitability of prices and the entire business for the past period. Nevertheless, it is the data on income and expenses that contain information on the basis of which forecasts can be made on the profitability of the case for the upcoming reporting period. That is, a budget can be planned to project profitability for a particular project or part of a business.

Why calculate profitability?

If you are calculating a profit indicator for the past period or trying to predict profitability for the coming period, then measuring profitability is the most important component of success. A business that is not profitable cannot survive. A business that is profitable will allow you to reward your owners at the expense of a large return on their investment.

Increasing profitability is one of the most important tasks of business managers. Managers are constantly looking for ways to change their business, increase profitability. To do this, they first of all need to not only learn what profitability is, but also take into account possible changes in the level of income. These potential changes can be analyzed in terms of profit or loss or partial budget. Partial budget planning allows you to evaluate the impact on profit and profitability of small and gradual changes in the business before they are implemented.

A variety of profitability can be used to assess the financial condition of the business. These relations, created on the basis of income and expenses, can be compared with industry indicators.In addition, with their help it is quite realistic to monitor the situation during the year to identify emerging problems.

Cash (cash) accounting method

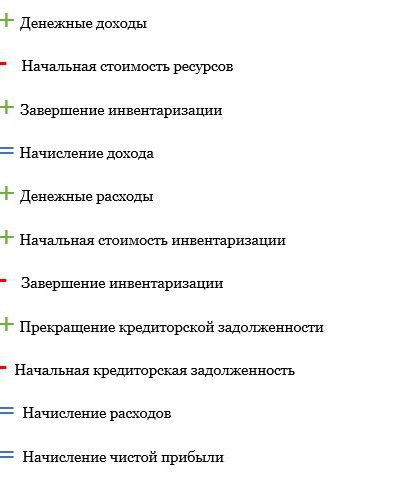

Traditionally, entrepreneurs have used the so-called monetary method of accounting, where income and expenses are recorded in the profit and loss account when goods are sold and services are paid. This method, used by most businessmen, allows you to calculate the cost of a resource not already used in the course of entrepreneurial activity, but just purchased, that is, its nominal price. This is used as a way to manage tax liabilities year after year. Nevertheless, many business systems take resources into account as an expense only when they are actually involved in business activities. In this case, profitability is calculated as follows:

Cash accounting

Net income may be distorted when using the cash basis of accounting at the expense of profit that was not expected. For example, the sale of two full crops in one season. Selling the resource that we purchased last year, we will receive less money due to its depreciation.

Accrual method

In order to provide a more accurate picture of profitability, an accrual method can be used. With its help, the income received is calculated from the position of when the products are produced (and not when they are sold), and expenses are reflected in the statements when using resources (and not when they are purchased). Accrual uses the traditional cash method of accounting throughout the year, but adds or subtracts inventories of products and production resources that the entrepreneur has at the beginning and at the end of the year. The calculation of profitability by this method looks in general terms as follows:

Profitability of production can be defined either as accounting profit, or as economic profit. Consider each of the species.

Accounting profit (net income)

Traditionally, profit was calculated using the so-called accounting profit. First of all, you need to think about a tax return. It contains a list of your taxable income and deductible expenses. These are the same items used in calculating accounting profits. Nevertheless, a tax return cannot give you an accurate picture of profitability due, for example, to the rapid deterioration of resources or other factors. That is why the profitability of the organization is often calculated using net income.

Accounting profit is an intermediate picture of the viability of your business. She will show that if one year of losses cannot permanently harm your business, then several years in a row (or if net income is not enough to cover expenses) can jeopardize the viability of the whole thing.

Economic profit

In addition to deducting business expenses, expenses are also deductible in the calculation. economic profit. Opportunity cost connected with money (equity), labor and management abilities. It takes into account what kind of profit you would gain or lose if you would engage in another business, work in a different specialty, use that resource, and not another. An alternative cost is also the return on investment, which the entrepreneur for one reason or another did not invest elsewhere. When calculating economic profits, they are displayed along with other expenses.

Economic profit predicts a long-term business outlook. If you can consistently generate a higher level personal income Using money and labor elsewhere, consider whether you want to continue to do this or that business.

Flow of funds

People often mistakenly believe that a profitable business will not face cash flow problems.Despite the fact that profitability of production and cash flows are closely related, they have a number of serious differences. Lists of income (statement of income and expenses) indicate the movement of funds, which include their inflow and outflow. Profit and loss information also speaks of profitability, while the cash flow statement shows liquidity.

Many points of income - this is cash flow. The sale of equipment, products and so on, as a rule, is income and relates to cash flows. Many items of expenditure characterize the outflow of cash points. The acquisition of additional units of resources, for example, is an expense and, accordingly, an element of cash outflows.

However, there are many cash positions that are not items of income and expense. For example, buying a tractor is considered an outflow of cash when paying in cash at the time of purchase. If money is borrowed with a quick loan, an advance payment is also an outflow of cash. The tractor is the main asset and has a validity period of more than one year. It is included as an expense in the income statement, but it is reduced in value due to depreciation of the physical and technological. This phenomenon is commonly known as depreciation. Depreciation expenses are established every year.

Depreciation is calculated for the purposes of income tax that may be received. But in order to accurately calculate net profit, a more realistic depreciation amount should be used to bring the actual decline in value over the course of the year closer.

The amount of interest paid on the loan is also included as an expense, along with depreciation, because the cost of borrowing money is of interest to the parties to the loan. Nevertheless, the loan itself is not an expense, but simply a transfer of funds between the debtor and the creditor.

Other financial statements

The income statement is just one of several such documents that can be used to measure the financial stability of a business where there is a return on equity. Other general information includes a balance sheet and a statement of cash flows.

They relate to each other to form a comprehensive financial picture of the business. The balance of assets and liabilities shows the solvency of the enterprise at a certain point in time. It is often prepared at the beginning and end of the reporting period (usually from January 1 to December 31). The operator records the assets of the enterprise and their value, as well as the value of liabilities or financial claims in relation to the business (i.e. debts). The amount by which assets exceed liabilities is the net worth of the business. It reflects, one might say, the price of a business in relation to the owner.

Cash flow information is a dynamic operator that registers cash flow during the reporting period. Positive (negative) cash flow will increase (decrease) depending on the working capital of the enterprise. The latter is defined as the amount of cash used to carry out business operations. It is calculated as current assets (cash) minus current liabilities (payable during the upcoming reporting period).

The need for profitability forecasting

A full set of financial statements, including the beginning and end of net information about the amounts, profit and loss statement, cash flow statement, report on the movement of the owner of capital and measures of financial activity allows you to make a comprehensive financial analysis of the business and get the most accurate and reliable data about its profitability, including evaluating the profitability of capital and prices. There is one more important indicator. This is cost-effectiveness.

In order for entrepreneurs to evaluate the profitability of an activity, you need to find out what profitability is, and then take into account all the financial indicators discussed above, which allow you to check business data and understand what kind of result you can count on.