The decision on the application of a particular taxation system is made at the time of registration of the company or when changing certain parameters of the economic activity of the enterprise. If, having familiarized yourself with all the options of the tax system, it was decided to change the regime, to implement such a procedure it will be necessary to fill out an application for transfer to the simplified tax system.

Can I fill out an application form for USN

To prepare the form it is not necessary to contact specialized law firms. So that when filling out the form no elementary errors are made, it is enough to be guided by the information in this article. It is also worth remembering that to change the tax regime there is a certain period for submitting such an application, so it is very important not to miss it. An application for the transition to the simplified tax system, the deadlines for which are clearly defined by law, can be submitted to the Federal Tax Service by Russian post or in person.

Why switch to the simplified tax system

One of the most convenient and profitable tax regimes is a simplified system. It helps to minimize regular tax deductions. For companies that have a small business format, this mode is most convenient, since not only tax payments are reduced, but also the amount of workflow.

Criteria for the transition to "simplified"

In order to exercise the right to use the simplified tax system, a company must meet certain requirements set forth in the Tax Code of the Russian Federation.

The indicators should be as follows:

- The amount of income received, with the exception of credit investments, from 2017 cannot exceed 59.805 million rubles for the first 9 months of the year.

- The number of employees is limited to 100 people.

- The cost of depreciable fixed assets from the beginning of 2017 should also not go beyond 150 million rubles.

What time frame is the transition

An application for the transition to the simplified tax system must be submitted to the regulatory body by December 31 of this year. Those who did not manage to notify the tax inspectorate of a change in the tax regime are not entitled to apply the “simplification” from next year. Newly created enterprises are obliged to inform the regulatory authorities that they have decided to use the special regime, within 30 days after registration. If the deadlines are met, such firms have the right to use STS from the very beginning of their activity.

Organizations applying UTII submit an application for the transition to the simplified tax system in the first days of the month in which the obligation to pay a single tax ceased. When switching to the main mode, it is allowed to return to the “simplified mode” only after a year.

The basic principles of tax assessment when using special mode

The simplified taxation system is mostly focused on small businesses, as the special regime allows you to reduce tax liabilities. Organizations that have decided to use the “simplified payment system” should not be charged and paid VAT, property tax and profit. Individual entrepreneurs also receive exemptions in terms of paying income tax accrued on wages.

A simplified system involves the calculation of tax at two rates. Income reduced by the amount of expenses incurred is taxed 15%, and if only income is used in calculating the tax base, then a tax of 6% is paid.

Filing an application for the transition to the simplified tax system is a confirmation of a decision on the application of a particular rate.Each entrepreneur makes a choice of the tax regime based on projected income and the scale of economic activity.

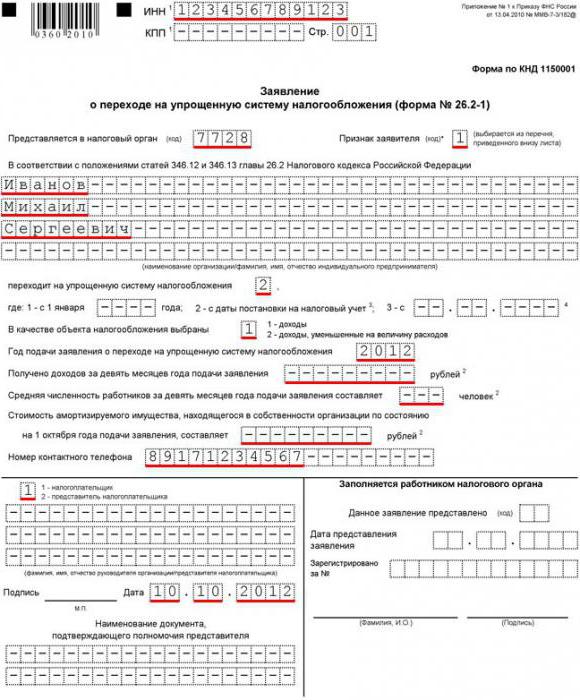

Application for the transition to the simplified tax system, sample fill

Application form No. 26.2-1 has only one title page, therefore, when filling out it, no insoluble questions should arise. After submitting the correctly completed form, the tax authorities make a decision on whether to apply the special regime or refuse because of the mismatch of certain parameters.

Start filling out the form with the required details of the company. In the top lines the TIN / KPP are surely registered. Then a four-digit tax inspection code is entered in which the company is registered.

Depending on the time at which the application for the transition to the simplified tax system is filed, you must affix a certain attribute code. The unit is put during the initial registration of the company, the number two indicates that the application is submitted after registration, and 3 should be put down when switching from another tax regime.

The title page of the application spells out in detail the name of the company or surname, name, patronymic of an individual entrepreneur. In the column "Tax rate" is the selected percentage of deductions.

If the company is already conducting business, the next part of the document indicates the amount of income received for the first nine months of the year. Also in the corresponding lines the average number of employees and the residual value of depreciable property are prescribed. If the entrepreneur has just registered, then these lines do not need to be filled out.

A signed application for transfer to the simplified tax system, the form of which can always be obtained from the tax authorities, is certified by the seal and provided to the Federal Tax Service at the place of registration.