The tax legislation of the Russian Federation allows citizens who have bought an apartment to return part of the costs associated with the acquisition of real estate in the form of a deduction. Using this privilege has quite a few nuances. They are associated with the procedure for calculating the amount of deduction, as well as with the sequence of registration of this compensation. What should I look for when contacting the competent authorities to receive appropriate payments? What documents do you need to prepare for a citizen?

What is the essence of property deduction?

Property deduction is the possibility provided by the tax legislation of the Russian Federation to reimburse part of the costs associated with the acquisition or construction of a real estate object - an apartment, a house or a land plot, including the payment of interest on a loan issued for the purchase of housing. In some cases, appropriate compensation may also be charged for the costs of repairs in a residential building.

Who can get a deduction?

The property tax deduction for the purchase of an apartment or house can be drawn up by: the owner of the property, the spouse of the owner (if the apartment was bought in marriage), the parent of the property owner, who is a minor citizen. The consideration in question can only be received by a working person or one who pays the state PIT at a rate of 13%. For example, receiving a salary under a civil contract. It is through taxes paid to the state that the deduction is returned. It can be those payments that are transferred to the budget upon the fact that a citizen has carried out taxable transactions, for example, related to the sale of another apartment.

What expenses are deductions based on?

Let us consider in more detail on the basis of what specific expenses a person can receive a property deduction. Corresponding compensation is charged in the amount of 13% of:

- the amount of money transferred to the seller of real estate under the contract of sale;

- expenses for the purchase of materials used for repairs in the purchased apartment;

- compensation of services for the implementation of construction and repair work in a residential building;

- costs associated with connecting the property to communications, if it is a residential building;

- amounts reflecting the amount of interest paid on the mortgage loan.

It is worth noting that the costs associated with repair and decoration can only be included in the deduction structure if they are incurred as part of the acquisition of a new building.

What may be the amount of property deduction?

Consider how much property deduction can be presented. According to the legislation of the Russian Federation, the maximum amount of expenses for the purchase of housing from which a deduction can be calculated is 2 million rubles. As for the mortgage interest, their maximum value, which is taken into account when calculating compensation, is 3 million rubles if the person first applied for a deduction in 2014 and has no restrictions if the housing on which he draws up a deduction was purchased until 2014. Moreover, in the first case, 2 million rubles, which constitute the maximum amount of expenses for the purchase of an apartment, can be calculated from any number of real estate objects. If a person purchased property before 2014, then only one.

Thus, the actual deduction payments may amount to:

- 260 thousandrubles based on the cost of buying a home;

- 360 thousand rubles in mortgage interest, if a person purchased an apartment, the purchase costs of which are the basis for deduction, in 2014 and later.

If housing was purchased before 2014, then the size of the deduction on mortgage interest (if the corresponding loan, of course, was drawn up) is not limited.

Deduction Documents

We will study what documents need to be prepared in order to receive a property deduction, as well as in what order the corresponding compensation is drawn up. It is worth noting that the right to use the privilege in question arises for a person only after he becomes the actual owner of his home. That is, as soon as he receives a certificate of registration of ownership of real estate or signs an act of transfer and acceptance of the apartment - if he participated in its construction as an interest holder. Thus, the first document that a citizen needs to prepare is the one that certifies his ownership of real estate.

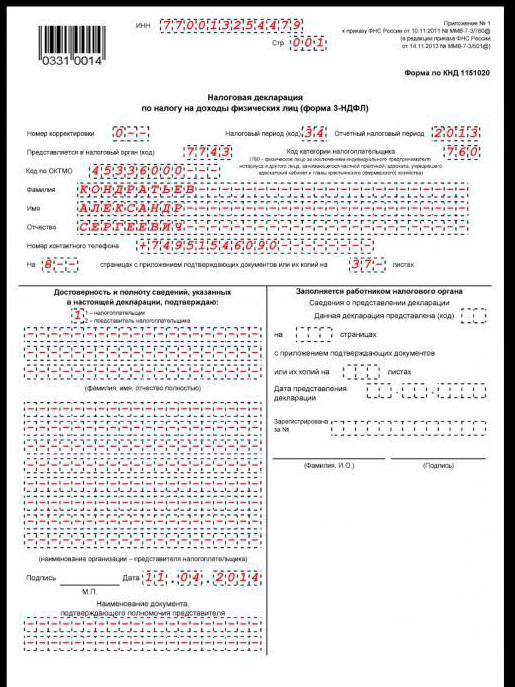

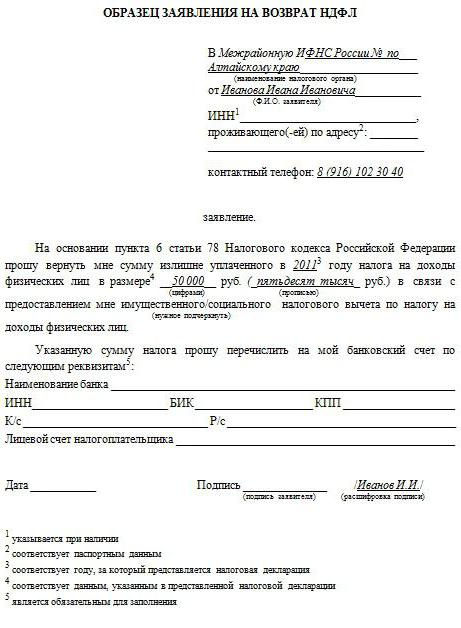

The next important source is a property deduction declaration. It is compiled in the form of 3-personal income tax. The citizen must fill out this document independently - by contacting, if necessary, a consultation with the Federal Tax Service or a specialized company.

Other sources that are generally required for processing compensation:

- certificate 2-personal income tax;

- application for property deduction in the prescribed form;

- passport;

- a contract of sale of housing or a contract with the developer;

- bank receipts confirming taxpayer expenses;

- statement from the mortgage account, in which the amount of interest transferred by the borrower for the loan is fixed.

Also, a person will need to open an account to which it will be convenient for him to receive a deduction in any bank.

Samples of deduction documents

The main difficulties characterizing the receipt of a property deduction are associated, as a rule, with the filling by the taxpayer of such documents as an application, form 3-NDFL. What are the nuances of working with them?

Visually familiar with them will help you drawn up for each of the marked documents sample. Property deduction - a procedure that requires compliance with the standards for filling various sources. Samples of these documents - applications for compensation, as well as forms of 3-personal income tax - are available in our review.

We will now study what are the ways to receive the payment in question. There are two of them:

- appeal to the Federal Tax Service according to the results of the past year - in person;

- appeal to the Federal Tax Service and the employer - during the year.

Methods of obtaining a deduction: through the Federal Tax Service

In the first case, the citizen will need those documents that we examined above. Having checked them within 3 months, the Federal Tax Service makes a positive decision regarding the provision of a deduction to a person or writes a justified refusal, usually meaning the need to provide any amended documents on the list or additional ones.

Receiving a deduction: appeal to the employer

If a person decides to receive a property tax deduction when buying a house by contacting the employer, the same sources will be required in general, with the exception of form 3-NDFL, as well as certificates 2-NDFL. It is not necessary to cook them in this case.

The second payment processing scheme involves the citizen's interaction with both the employer and the Federal Tax Service. First of all, a person must collect documents and submit them to the tax service. It should be noted that the application form for deduction in this case will be different - it must be issued to the Federal Tax Service upon appeal.

Having accepted the documents, the tax service will consider them within 30 days, and if everything is in order with them, it will issue a notification to the applicant that certifies the citizen's right to receive a deduction through the employer. This source will need to be attributed to accounting.

Based on the notice from the Federal Tax Service, the employer company will not be able to calculate 13% tax from the employee’s salary and thus pay it together with it. Personal income tax will not be withheld until the end of the year or until the deduction is exhausted. In order to continue to receive a deduction under this scheme, next year the employee will have to receive a new notification from the Federal Tax Service. Documents will need to be submitted to the tax office again.

Making a deduction: nuances

Consider the nuances that characterize the property tax deduction when buying an apartment.

First of all, it is worth paying attention to the fact that the compensation in question can be returned only to the extent that the citizen transferred to the state in the form of personal income tax. If a person has not paid taxes, then he will not be able to issue a deduction.

It is important that the tax rate in this case be 13%, that is, it should correspond to the one set for tax residents RF If a person has been outside Russia for more than six months, he receives non-resident status and will not have the right to process the payments in question until the period when he is in the Russian Federation will be longer than living abroad.

The next nuance that characterizes the property deduction when buying an apartment is the timing of the start of payment of this compensation to the employee by the company to which he applied for the desire not to legally pay the state salary taxes. In accordance with the clarifications of the Ministry of Finance of the Russian Federation, payments should begin from the month in which the person applied to the Federal Tax Service.

It can be noted that a citizen has the right to use both mechanisms for calculating the deduction at the same time. So, he can receive compensation through the employer, for example, from September to December, and next year - apply for it to the Federal Tax Service for the period from January to August.

The next caveat is the deduction when working for several companies. Until 2014, a person had the opportunity to receive compensation from only one employer. But since 2014, changes have come into force in the Tax Code of the Russian Federation. The property deduction has become possible to draw up with any number of employers at the same time. True, in this case, the citizen must indicate in a statement to the Federal Tax Service how he wants to distribute the deduction between different employers. The tax authorities, in turn, will have to give the applicant several separate notifications for each company.

Mutual offset of citizen and state obligations

The tax deduction for the purchase of housing can be set off against the payment of personal income tax for the sale of housing. In this case, its amount, determined on the basis of the value of the property, expenses, and in some cases based on mortgage interest, can be spent within 1 year. To implement this procedure - the offset of deductions and taxes, you need to contact the Federal Tax Service. Specialists of the department will provide the necessary advice.

For what period can a deduction be made?

A person can apply for compensation for expenses for an apartment for 3 years prior to applying to the Federal Tax Service if he is a working citizen, or for 4 if he receives a pension. In this case, several declarations are submitted to the tax service - for each year.

It can be noted that the right to property deduction does not have a limitation period. A person has the right to apply to the Federal Tax Service or to the employer for appropriate compensation at any time, even several years after the sale of the apartment, for which he is going to receive payments guaranteed by law.

Summary

So, the Russian Tax Code includes the rules according to which citizens of the Russian Federation have the right to make deductions based on the amounts spent on the purchase of a home, its repair or interest paid on mortgages. These compensations can be received in two ways - by contacting the employer or through direct interaction of a person with the Federal Tax Service.

The maximum amount on the basis of which the property deduction can be calculated depends on the year the citizen first appealed to the tax service. If he first made compensation before 2014, then he will be able to receive a payment of up to 2 million rubles from one property, but if it is possible to calculate the deduction from an unlimited amount of interest on the mortgage.

If a person first applied to the Federal Tax Service in 2014 and later, he is entitled to receive compensation in the amount of 2 million rubles spent on the purchase or repair of any number of real estate objects. However, with regard to the maximum amount of mortgage interest from which a deduction can be obtained, in this case it amounts to 3 million rubles.

Compensation can be filed with several employers. A combination of this deduction scheme and the mechanism for processing it through the Federal Tax Service is quite acceptable.