Liquidity as an economic term does not mean the destruction of anything, but, on the contrary, determines the ability of material resources belonging to a legal entity to transform into cash. AT financial analysis it is customary to use ratios that make it possible to assess the share of liabilities that can be settled at the expense of assets. Using the absolute liquidity ratio, you can determine the percentage of obligations that the company is ready to repay at the expense of available funds.

Types of liquidity

Assessment of the solvency of an economic entity consists of the calculation and analysis of liquidity ratios. The current indicator shows how many monetary units from existing assets correspond to one ruble of short-term debt. That is, the higher the absolute value of current assets, in comparison with short-term liabilities, the more stable the financial condition of the company. The quick liquidity ratio indicates the ability of the company to immediately repay its debts at the expense of cash, investment and debts owed to this company.

And the third absolute liquidity ratio shows the ability of an enterprise to cover current liabilities exclusively with cash available at a particular point in time at the disposal of an economic entity.

Calculation Data

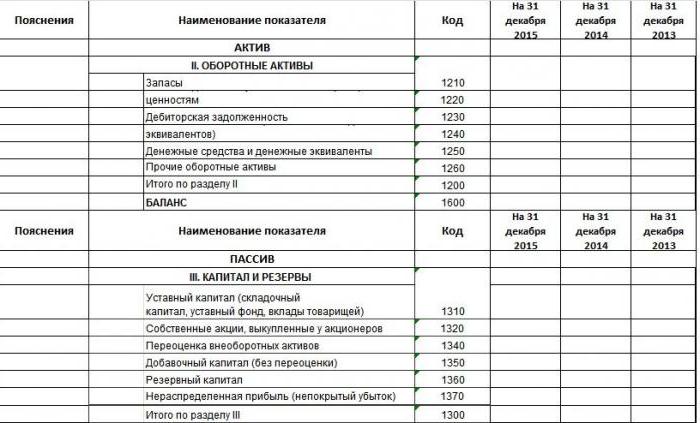

To calculate the quality indicators of doing business, analysts and financiers use financial statements as source information. For whom the form of the balance sheet is not new, they know that indicators (assets, liabilities) are assigned codes when filling out. An example of filling is shown in the photo.

This is an excerpt from the balance sheet. There are five sections in it, two chapters belong to current and non-current assets, that is, to the elements of wealth of a company that can be sold or converted into money. The remaining three sections: liabilities, capital and reserves. They relate to sources of assets.

Therefore, having available a completed balance sheet of the enterprise, you can calculate all the indicators, including the absolute liquidity ratio. Balance formula:

To abs. L = (code 1240 + code 1250) / (code 1520 + code 1510 + code 1550).

Data Interpretation

Now you need to figure out which specific liabilities and assets are included in the definition of the indicator. So, the numerator is assets, and the most liquid ones. Line 1240 displays the amount of financial investments up to a year excluding cash equivalents. These include: debt securities, authorized deposits in other organizations, loans to certain companies and other similar investments. The fact is that in the balance sheet of the enterprise in the first section there is line 1170, which also reflects financial investments, but they are long-term and do not participate in the calculation of this indicator. Code 1250 is cash and cash equivalents. These assets include cash on hand, on accounts, transfers in transit, deposits, and highly liquid securities.

Absolute liquidity ratio is the ratio highly liquid assets to urgent and short-term liabilities. The denominator of the formula consists of borrowed funds, debt to other entities and other obligations.

Absolute liquidity ratio: formula

If we structure the balance sheet for assets and liabilities, then the previously recorded expression of absolute liquidity can be represented by a more generalized formula. Assets help to make a profit for the enterprise, and liabilities form assets.They are interconnected and equal in total, therefore the form where these elements of economic activity are displayed is called the balance sheet.

A qualitative characteristic of assets is liquidity, that is, their ability to turn into money. It follows that cash is the most highly liquid. Liabilities are grouped by maturity. The ratio of groups of assets and liabilities determine the relevant indicators.

So, how to calculate the absolute liquidity ratio? The balance sheet formula is generalized:

To abs. L = A1 / (P1 + P2).

Group A1 as the most highly liquid includes cash and short-term investments. In total, there are 4 such groups, followed by quick-selling, slow-moving and difficult-to-sell assets.

P1 is a group with urgent liabilities, and P2 is a category short-term liabilities. There are also long-term (P3) and permanent liabilities (P4).

Balance sheet liquidity

Determining the degree of coverage of a company's liabilities with assets whose time interval for converting them into cash corresponds to the period of repayment of liabilities is called balance sheet liquidity.

- When A1 is greater than P1, it is believed that the solvency of the organization for the reporting period is sufficient.

- A2 more than P2 indicates the ability to cover the obligations of the enterprise in the near future.

- A3 over P3 is a condition confirming the solvency of an economic entity for a long-term period.

- A4 less than P4 follows as a consequence of the first three conditions and indicates the presence of an entity's own working capital.

The balance is not liquid provided that A4 => P4. However, such an analysis is approximate, more precisely, the conclusion about the solvency of the enterprise can be made using financial ratios. It is a comparison of liabilities and liquid assets that allows you to calculate the absolute liquidity ratio on the balance sheet, which is equal to the private funds from the first group of assets and the sum of term and short-term liabilities.

The economic meaning of absolute liquidity

According to the calculation and the formula, the value of the absolute liquidity ratio shows what percentage of current liabilities a company can pay out of the available funds in the account. This indicator is interesting to suppliers of raw materials, since absolute liquidity is taken into account to assess the present ability to pay obligations.

But what should be the indicator for solvency to be considered normal? In foreign practice, the norm of the absolute liquidity ratio of 20% or 0.2 is adopted. It would seem that the higher this indicator, the better. But a high value can be obtained in connection with the irrational structure of capital, when the share of assets is high and reflects money not invested in production. It is better to use for analysis this coefficient in dynamics for several reporting periods of time.

Absolute liquidity difference from current and urgent

If the absolute liquidity ratio shows instant solvency, then the critical and current liquidity data reflect the company's ability to cover liabilities in the medium and long term. Although financial analysis calculates all three coefficients, their values obtained are interesting for different groups of subjects. So, the quick liquidity ratio is important for creditors and banks to assess timely solvency.

The current liquidity indicator is used by investors to confirm the fulfillment of current obligations in due time. And the absolute liquidity ratio is attractive for suppliers with short loan periods, because its value expresses the ability to immediately repay current short-term liabilities.

The main difference between all three indicators is the composition of liquid assets participating in the repayment of the company's debt.

Value above / below normal

As mentioned earlier, the foreign absolute liquidity ratio is 0.2, but in Russian analytical practice, the upper limit of this value, which is 0.5, has been identified. When the value is below the norm of 20%, it is believed that the growth of short-term loans is not proportional to the increase in current assets. The situation may be related to the emergence of new sources of additional income for the company, as a result of which an increase in free cash accounts was caused.

The increase in absolute liquidity ratio may be associated with a decrease in receivables due to an agreement with counterparties on prepayment of supplies, as well as optimization of inventory management.

In general, in practice, consideration of liquidity ratios should be accompanied by their totality. The scatter in values can be all sorts of reasons that are theoretically impossible to cover.

Ways to increase the liquidity of the enterprise

- Decrease in receivables. An exit is an agreement with debtors to conclude a cession transferring a debtor's obligations to a third party.

- Profit increase. There are no specific recommendations for this item, since there is a dependence of this indicator on various factors that are individually inherent in each economic entity.

- The decrease in stocks with an increase in working capital.

- Optimization of capital structure, in which own funds must exceed borrowed.

Following these points, the company will become solvent, attractive to investors, and then the absolute liquidity ratio with similar indicators will be within normal limits.

Calculation Example

An excerpt is given of the completed balance sheet of the enterprise, it is necessary to calculate the absolute liquidity indicator.

| Explanations | Name of indicator | Code | As of December 31, 2014, thousand rubles | As of December 31, 2013, thousand rubles | As of December 31, 2012, thousand rubles |

| Assets | |||||

| 2. Current assets | |||||

| Stocks | 1210 | 460 | 390 | 260 | |

| Receivables | 1230 | 150 | 126 | 110 | |

| Financial investments (net of cash equivalents) | 1240 | ||||

| Cash | 1250 | 800 | 600 | 400 | |

| Total section 2 | 1200 | 1410 | 1116 | 770 | |

| Passive | |||||

| 5. Short-term liabilities | |||||

| Borrowed funds | 1510 | 300 | 150 | 400 | |

| Accounts payable | 1520 | 189 | 525 | 551 | |

| revenue of the future periods | 1530 | ||||

| Other liabilities | 1550 | 100 | 150 | 90 | |

| Total section 4 | 1500 | 589 | 825 | 1041 |

To find the absolute liquidity ratio, the formula of which was described earlier, it is necessary to substitute the values from the balance sheet corresponding to a specific code in the expression: quotient of assets by codes (1240 + 1250) to liabilities (1510 + 1520 + 1550), hence:

Abs. 2014 = 800/300 + 189 + 100 = 1.36

To abs. L 2013 = 600/150 + 525 + 150 = 0.73

To the abs. 2012 = 400/400 + 551 + 90 = 0.39

Short-term debt at the reporting moment can be repaid in 2014 immediately; in 2013 - in 1.4 days, and in 2012 obligations not exceeding the period of 12 months will be fulfilled in 2.5 days.