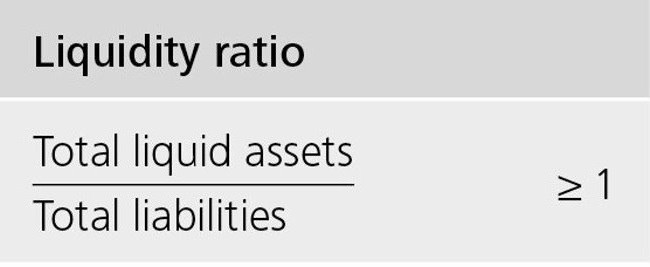

Liquidity is used if it is necessary to assess the ability of a legal entity to cover current liabilities from its own property. Liquidity is in conjunction with the speed with which a company can turn its property into finance. The quick ratio shows how much debt will be covered by the company's cash resources and their equivalents.

Company liquidity concept

Liquidity ratios apply to company assets. Based on the pace of implementation, they are:

- Highly liquid. This property does not require sale, or is sold almost instantly. This includes short-term financial investments and funds.

- Fast liquid. The sale of these assets does not last long. This includes debt receivables, and short-term.

- Medium liquid. It is sold either with the loss of part of the price, or long enough. Relate stocks of the enterprise.

Three kinds of odds

Based on the speed of sale of property, there are three types of indicators:

- Absolute liquidity ratio, calculated for assets with high solvency.

- Quick ratio (or fast). It is determined by the sum of property assets with high and quick liquidity.

- Current ratio. Applies to all current assets.

Any of these indicators provides a chance to assess the liquidity of the company, given the binding to the date.

What is urgent liquidity

Quick ratio shows the company's ability to cover its short-term debt through sales highly liquid assets. Liquid assets mean money, short-term financial investments, debt of debtors, the repayment of which is expected within a year.

Another version: the entire amount of current assets is taken, the amount of stocks is removed from it.

This ratio is widely used by Russian and foreign companies together with the current ratio. But, unlike the latter, when calculating urgent liquidity, stocks that are not highly liquid assets are removed from the general indicator of current assets.

The quick (urgent) liquidity ratio demonstrates the ratio of money and their equivalents. That is, this ratio more accurately shows the KPI of the company's liquidity than the KPI of current solvency.

There is an assumption in the work of companies that with the growth of liquidity ratios (urgent and current), the ability of an enterprise to cover its obligations also increases. But too high values may indicate the inefficiency of the use of working capital. We give an example: an enterprise has a large amount of cash that it does not use, but could invest in the assets of other companies and make a profit.

What quick liquidity demonstrates

The quick liquidity ratio provides an opportunity to calculate the share of the company's current debts, which may be covered by own resources over a short period of time. The calculation of the indicator is carried out on a specific number or numbers, if you need to know the dynamics of the coefficient.

Such a solvency calculation is most interesting for partners of the company who provide loans to it. But indicators are also used in the interests of the company itself. The literacy of the calculation, by and large, depends on the quality of the source information that is involved in the calculation of the indicator.

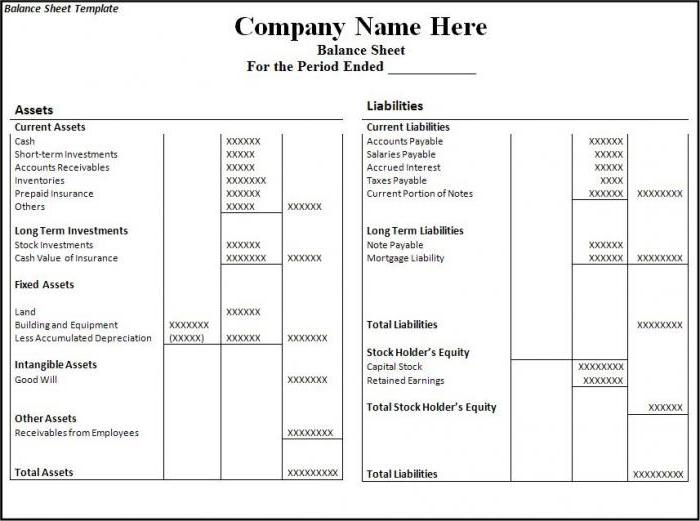

Information for calculations is taken from the financial statements of the enterprise.Rather, from the parts in which current assets and short-term loans are indicated. If you include information about assets whose real sales speed will be lower than expected (as an example: data on securities that are not credible or overdue receivables), the real picture will already be distorted. As a result of this, during calculations it is important at the same time to investigate the quality of the data that was taken for calculation. If there are doubts about the quality of the data, it is better to exclude them.

How to calculate the quick ratio

The formula of the indicator is as follows: the ratio of the number of assets that are highly liquid and quick liquid to the amount of debt that must be covered during the year.

The numerator is the sum of funds, short-term debt of debtors and the same financial investments. It can also be calculated as follows: the amount of current assets reduced by the size of stocks.

Short-term liabilities - the share of existing debts to creditors.

We calculate the quick ratio on the balance sheet:

Easy-to-sell assets (A1) / (Liabilities most urgent (P1) + Loans and borrowings short-term) = line 1250 form 1 + line 1240 form 1) / (line 1520 form 1 + line 1510 form 1).

Optimal value: above one. The indicator below demonstrates the need for regular work with receivables so that the company has the opportunity to transfer part of its current assets to funds for settlement with its counterparties.

We analyze the resulting indicators

The value of the quick ratio is interpreted differently.

The indicator is equal to one: the value of property that is quickly traded and highly liquid covers the debt.

The indicator is higher than one: it is possible to sell assets and cover Current responsibility. After that, there will still be part of the funds that will go at the disposal of the company.

Absolute (urgent) liquidity ratio below one: quick-selling assets are not enough to pay off all current debt over a short period of time. Here the optimal value is in the range from 0.7 to 1. Too low indicators are unfavorable, especially if there are a lot of figures in the calculation that relate to receivables.

Analysis of the dynamics of the coefficient

A study of dynamics can show the following:

- A growth indicator indicates an increase in the company's ability to cover its current liabilities in a short period of time. But too high growth rates indicate a decrease in the asset turnover rate and, as a result, a decrease in the company's profitability.

- A decrease in the indicator shows a decrease in solvency (liquidity) in relation to short-term debt.

What affects solvency

The dependence on some indicators can be determined by the calculation formula. An increase in the numerator will mean an increase in value. In other words, the increase in the number will be with an increase in articles:

- cash balance;

- short-term financial investments;

- accounts receivable with a maturity of one year.

Increasing the amounts that are in the denominator reduces the value of the coefficient. The decrease in the indicator will occur due to:

- increase the amount of loans issued for a short period of time;

- increase in short-term debt to those who issued loans;

- the remaining debt to creditors.

Conclusion

A demonstration of the optimal performance of the company is the fact that the amount owned should cover about twenty percent of current liabilities. But for some Russian organizations, taking into account the structure of short-term debt and its heterogeneity, the ratio may be at least 0.5.

- Ksl = (current assets - stocks) / short-term liabilities.

The quick liquidity ratio, the formula of which is indicated above, demonstrates the ability of an enterprise to meet its current obligations through the sale of highly liquid assets.